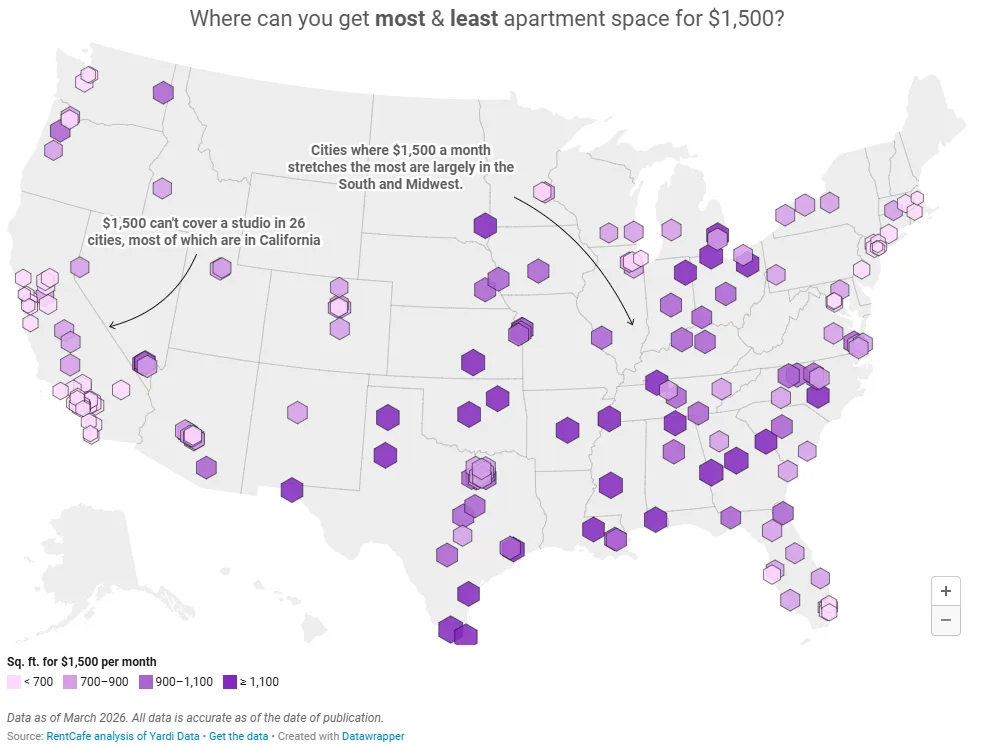

- Apartment size for $1,500 swings from 1,378 SF in McAllen, TX, to just 210 SF in Manhattan, NY, per RentCafe’s 2026 data.

- Two-thirds of the largest 200 US cities offer more space than the 703 SF national average for this rent budget.

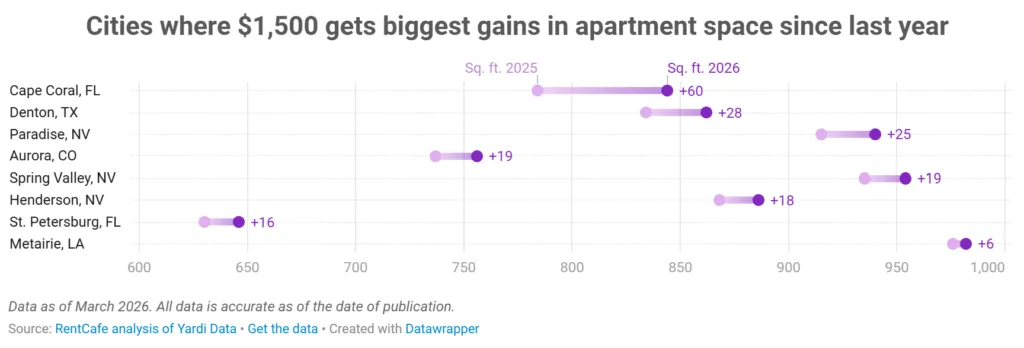

- In 26 cities—mostly across California—$1,500 won’t cover even a studio; only Metairie, LA, saw an increase in space for that rent since 2025.

Apartment Value Diverges Sharply by Market

According to RentCafe’s June 2026 analysis, the amount of space renters get for a $1,500 budget continues to diverge dramatically by location. McAllen, TX, remains the most affordable, delivering four times the apartment size possible in Manhattan—1,378 SF versus just 210 SF.

Across the 200 largest US cities studied, lower-cost Southern and Midwestern markets stretch a renter’s dollar the furthest, while coastal and high-density metros are out of reach for many households. As of March 2026, the national average apartment rent stood at $1,740 per month and the typical unit at 835 SF, meaning a $1,500 budget comes in below the median but still gets you a competitive footprint in many secondary markets.

RentCafe notes that 64.5% of cities surveyed offer more space than the 703 SF national average accessible at the $1,500 level, further highlighting stark regional disparities. The analysis reveals that rent inflation and tightened supply are compressing apartment footprints in nearly every market, with only a handful of exceptions.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Where the Space Stretches—and Shrinks

Large disparities persist. Renters in McAllen, TX, get more than 1,370 SF for $1,500. Meanwhile, Manhattan offers barely enough space for a studio.

At the other end, 26 cities provide less than studio-sized apartments for $1,500. Most of those cities are in California.

Metairie, LA, was one of the few markets to gain space. Apartment size increased from 976 SF in 2025 to 982 SF in 2026. That shift moved renters from a one- to two-bedroom into a compact three-bedroom.

Nearly one-third of the 200 cities studied gained some square footage since last year. However, most increases were modest. Outside Metairie, they rarely unlocked larger apartment types.

By contrast, renters lost ground in three cities. They include Kansas City, KS, Lincoln, NE, and Omaha, NE. Renters there now get one fewer bedroom for $1,500. Rising rents, supply limits, and slower income growth drove the decline.

The Details

McAllen, TX, offers the most space nationwide. A $1,500 budget rents an average apartment of 1,378 SF. That is enough for a large three- or four-bedroom.

Other top markets include Macon, GA, at 1,346 SF, and Columbus, GA, at 1,335 SF. Wichita, KS, and Jackson, MS, each offer 1,287 SF. Their average rents remain well below the national average.

Manhattan ranks as the least affordable market. A $1,500 budget rents only 210 SF. Brooklyn follows with 292 SF, while Queens offers 314 SF.

California dominates the least affordable markets. Fifteen of the 26 cities in this group fail to provide even a studio. Los Angeles offers 429 SF and averages $2,774 in rent. San Francisco provides 307 SF and averages $3,577.

In about half of the 200 cities studied, $1,500 rents a one- to two-bedroom. In 31 markets, it covers a two- to three-bedroom. Most are in the Southeast and smaller Midwest metros, including Oklahoma City and Memphis.

Squeezed by Rent Growth and Geography

Rent inflation continued to squeeze renters in 2026. Fewer cities now offer more space for the same budget. At the same time, top metros demand more rent for less space.

The national average apartment rent reached $1,740. Only eight of the top 200 cities remain below $1,200. As a result, affordability has shifted toward secondary and tertiary markets. This divide mirrors recent rental trends, as Midwestern markets gained momentum while several coastal hubs lost ground.

Midwest and Southern cities still offer better value. They benefit from slower rent growth and larger housing supplies. By comparison, coastal markets remain far more expensive.

The findings match broader 2026 trends from Yardi Matrix. Multifamily deliveries continue to rise, while absorption remains healthy. One-bedroom units now dominate new development.

However, construction activity lags in much of California and New York. That shortage tightens supply in the smallest and priciest segments. Consequently, fewer renters can afford two- or three-bedroom apartments in major urban cores.

RentCafe’s Alexandra Both said half the cities still offer a one- or two-bedroom for $1,500. That remains a sweet spot for many households. Still, market conditions continue to shift.

Rent increases in midsized metros have pushed some renters into smaller units. Square footage declined most in Queens, down 8.9%. San Francisco fell 5.5%, while Bridgeport, CT, dropped 4.5%.

Why It Matters

Apartment affordability continues to shift across the country. Lower-cost metros still keep average rents below $1,500. Meanwhile, gateway cities have become difficult for middle-income households to afford.

The data shows that space matters as much as rent. It influences where graduates, remote workers, and families choose to live.

Thirteen percent of the cities studied offer only a studio or less for $1,500. That trend reflects construction delays and long-standing policy barriers along the coasts.

Markets such as McAllen, Macon, and Wichita may attract more residents. Value-conscious households increasingly seek more space for their money.

The effects extend beyond renters. Developers, owners, and investors are adjusting underwriting and product strategies.

Cities where $1,500 unlocks a larger apartment may see stronger absorption and faster lease-ups. Markets moving in the opposite direction could face higher turnover and longer vacancies.

The apartment construction pipeline slowed in late 2025. CoStar reported a 14% annual decline in starts. Tight supply will likely keep raising rent-to-space ratios, especially in costly metros.

This imbalance continues to support Sun Belt markets. RentCafe’s city-level analysis also gives multifamily professionals better tools for underwriting and portfolio decisions.

What’s Next

Rent growth, supply limits, and changing demand will likely widen differences in apartment values. Yardi Matrix expects California and New York to remain undersupplied. As a result, renters there may see little improvement in available space for $1,500.

Mid-sized Southern and Midwest cities could attract more budget-conscious renters. Institutional and private investors may also keep shifting portfolios toward these markets.

RentCafe’s local data offers useful benchmarks. That is especially true as projects face longer timelines and higher operating costs. Multifamily stakeholders should expect continued volatility in rents and apartment sizes over the coming quarters.