- Institutional investors remain bullish on self storage, even as occupancy ticks downward and new deliveries decline, per DXD Capital.

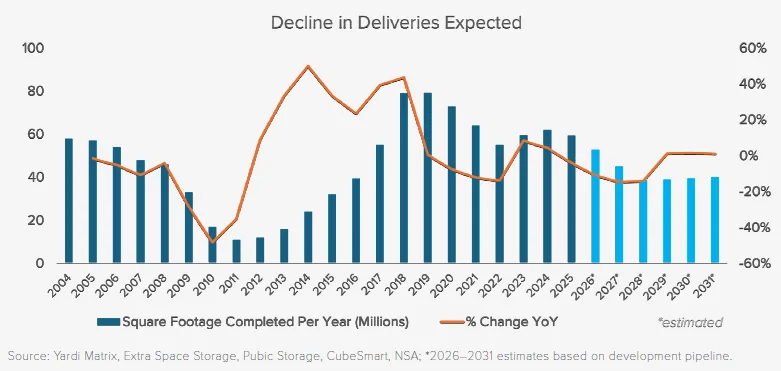

- Deliveries are set to fall from 59M to 38M net rentable SF by 2028, the lowest in a decade, helping limit occupancy erosion.

- High-profile deals like Public Storage’s $10.5B NSA acquisition signal confidence in the sector’s long-term fundamentals despite macro headwinds.

Pandemic Gains Reset as Market Normalizes

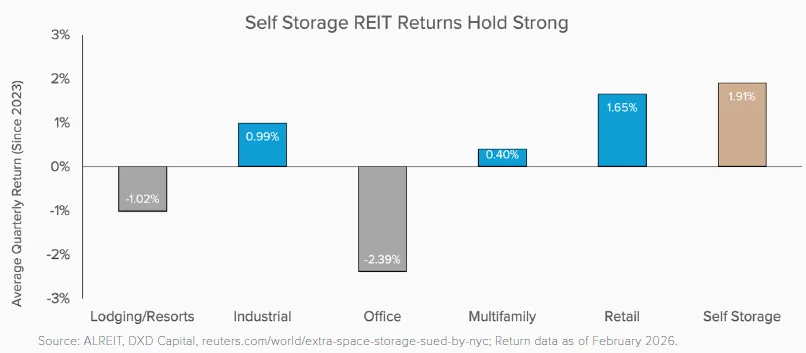

Institutional investors continue to pour into the self storage sector even as headwinds gather, according to DXD Capital’s latest Self Storage Quarterly Download, cited by Multi-Housing News. Headline returns remain sector-leading, with self storage posting an average quarterly return of 1.91% since 2023, compared to negative returns for office and lodging. But the sector is seeing a pronounced operational reset. Occupancy rates, which soared to all-time highs during the pandemic, are now below previous averages. Market observers are watching as the industry recalibrates expectations for the next several years.

Self storage’s resilience stands out against other commercial asset classes. DXD Capital’s report highlights that while office and hotel performance stays negative, self storage solidly outpaces both in risk-adjusted returns. Still, lower occupancy levels and a declining new-supply pipeline mark a shift away from the pandemic boom, forcing operators and investors to adjust strategies for a different interest rate and demand environment.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

US self-storage occupancy fell to 91.5% in Q1 2026, according to DXD Capital. That sits below the 92.8% pre-pandemic average and the 96.4% peak reached in Q3 2021. Slower home sales and weaker relocation activity reduced tenant demand.

Meanwhile, annual deliveries will drop from 59M net rentable SF to 51M this year. They should fall further to 38M by 2028. That would mark the lowest level since 2016. It also equals nearly half the 79.2M SF delivered in 2019.

Supply remains tight nationwide. However, performance depends heavily on local conditions. Markets often compete within a three-mile radius. Recent projects reflect that trend. DXD recently completed a 94,975-SF facility in Georgetown, Texas. It partnered with Mar-Gulf Management and MDI Capital. Extra Space operates the property.

Institutional Appetite and Ongoing Consolidation

Tighter supply has not reduced institutional demand. Public Storage announced a planned $10.5B acquisition of National Storage Affiliates in March. The deal would add more than 1,000 properties and 327M SF. It would also increase Public Storage’s REIT-managed market share from 35% to 44%.

That expansion would narrow the gap with Extra Space Storage. Together, the companies would strengthen their positions at the top of the sector. Private capital remains active as well. Heitman secured $475M for its latest funds. Blue Vista and UBS also formed a $600M joint venture with Extra Space.

DXD Capital’s Drew Dolan sees consolidation as a sign of sector maturity. He also points to more sophisticated and data-driven operations. In his view, both trends show self-storage has become an established institutional asset class.

Why It Matters

For CRE professionals tracking capital flows, self-storage remains a bright spot. Lower occupancy and weaker housing turnover may limit rent growth. However, the shrinking development pipeline helps prevent oversupply. Recent market reports suggest operators have already moved into a more balanced phase after supply growth and rent declines weighed on performance earlier this year. DXD Capital expects steady, though modest, rent and occupancy gains through 2028.

The pending $10.5B Public Storage-NSA merger highlights institutional confidence in scaled platforms. The companies expect to close the deal in Q3 2026. Public Storage could soon control nearly 45% of REIT-managed storage space. That would bring it closer to Extra Space and deepen industry consolidation.

Self-storage has also outperformed many CRE sectors. DXD reports positive quarterly returns since 2023. As a result, investors view the sector as a defensive option. Joint ventures, new funds, and major acquisitions show sustained interest from public and private capital.

For investors timing market cycles, Dolan points to 2029 and 2030. He expects peak maturities and new portfolio opportunities during that period. That outlook may encourage new entrants to invest sooner.

What’s Next

With deliveries forecast to contract through 2028 and no bounceback in sight, occupancy and rental rate growth should remain largely steady across most US markets—absent a major national demand shock. Institutional players are likely to continue consolidating, fueled by both capital inflows and a push for scale and operational efficiency. As consolidation continues, large operators are leveraging analytics and tech to squeeze more value from existing portfolios. For new entrants, the “window to position ahead” of the sector’s next peak, as Dolan notes, is now. Watch for further deal announcements as institutional conviction remains resilient despite operational resets.