- Distressed office transactions in US CBDs have surged, with nearly 35% of total square footage sold since 2024 considered distressed.

- National office vacancy dipped to 17.7% in May 2026, but office utilization remains notably below pre-pandemic norms with hybrid work entrenched.

- Urban core towers face sharper discounts, while cities like San Francisco and Austin see vacancies falling as new supply dries up and employment stabilizes.

Flight to Quality Deepens CBD Distress

Yardi Matrix’s June 2026 report finds distress rising sharply for US office assets, especially in commercial business districts (CBDs). While national office vacancy dropped to 17.7%—down 230 basis points from its March 2025 high—utilization lags pre-pandemic patterns. Kastle Systems reports national office attendance has flatlined at around 55%. Demand is fragmenting, with weaker properties and urban core towers suffering greater distress while trophy assets capture outsized demand. This gap is expected to widen as AI adoption accelerates and occupier requirements evolve.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

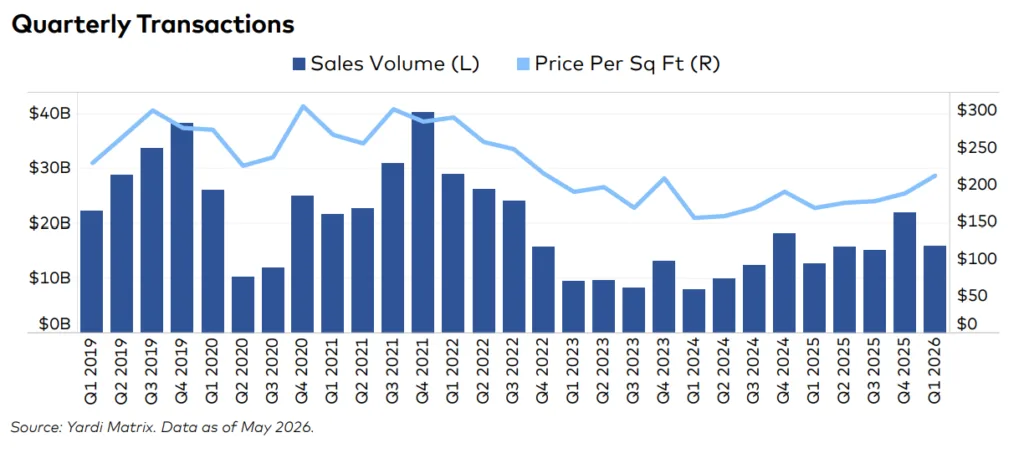

Of the 800M SF in office transactions tracked since 2024, 19.4% were distressed, up from just 6.2% in the prior three years. In CBDs, distressed sales accounted for 34.6% of activity by square footage, compared to 24.5% in broader urban areas and only 12.1% in the suburbs. Average size for these transactions has ballooned post-Covid—now roughly 200,000 SF, double pre-pandemic norms.

Notably, a 44-story Seattle CBD tower, currently 47% vacant, is under contract to sell for $280M—a 54% discount from its 2019 price, per Bloomberg. If the deal closes, Blackstone (through Perform Properties) will offload the U.S. Bank Center to Spear Capital amid ongoing tech layoffs and demand contraction downtown.

Hybrid Work Reshapes Urban Dynamics

The office recovery remains a story of contrasts. National vacancy rates are trending down and some markets stand out. San Francisco’s vacancy fell to 23.3% in May 2026—a 520 basis point decline from the prior year, the steepest drop among major metros. This reversal followed severe pandemic-era job losses in the tech-heavy Bay Area. However, as office employment stabilizes and AI-driven demand perks up, especially in finance and tech, leasing activity is firming.

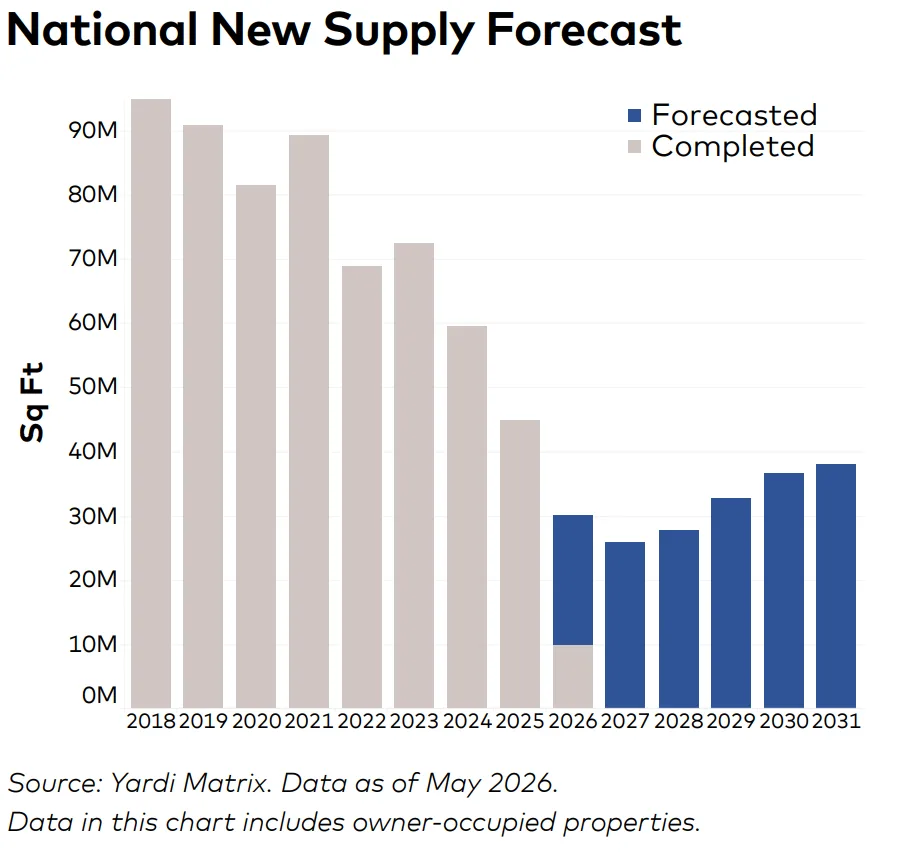

In contrast, Austin—despite corporate relocations and a drop in vacancy of 440 basis points over 12 months—still faces an elevated 24% vacancy, the highest among top metros. Its supply pipeline, once among the nation’s most robust, has been cut in half, reflecting hesitancy to add space while current vacancies remain high. Nationally, just 29M SF (0.4% of inventory) is under construction, a historic low likley to temper future pressure.

Why It Matters

For office lenders and owners, rising CBD distress is reshaping risk and asset values. Since 2024, 73% of CBD office properties with prior sale data traded at discounts. That far exceeds the 48% rate for urban non-CBD assets and 42% for suburban properties. Larger buildings in dense markets have struggled to match changing tenant needs and hybrid work patterns. As a result, they posted steeper value losses. Cities like Seattle highlight the impact of tech layoffs and weaker occupancy. Similar pressures have emerged across downtown markets as investors reassess aging office stock and shifting demand patterns.

Meanwhile, the national average listing rate reached $33.61 PSF in May, according to Yardi Matrix. That was $0.70 higher than April but 1.4% below last year. Trophy assets still command premiums, with Manhattan at $69.29 PSF and Miami at $58.41. That reflects the ongoing flight to quality. Still, only properties with strong demand or top amenities are preserving value. Uncertainty continues to weigh on the market. Office-using sectors lost 170,000 jobs between May 2025 and May 2026, adding pressure on leasing and absorption.

What’s Next

With the supply pipeline near historic lows and distressed deals making up almost a fifth of office sales, the sector faces a lengthy sorting period. Older buildings will likely see more pricing pressure. In contrast, newer and renovated properties should benefit from demand for flexibility, amenities, and prime locations. Over time, occupiers will likely place greater emphasis on adaptable space as AI adoption and hybrid work expand. Expect more coworking demand and a wider gap between top- and lower-tier assets through 2027 and beyond.