- Large industrial tenants are rapidly absorbing surplus big-box warehouses, sharply reversing pandemic-era oversupply.

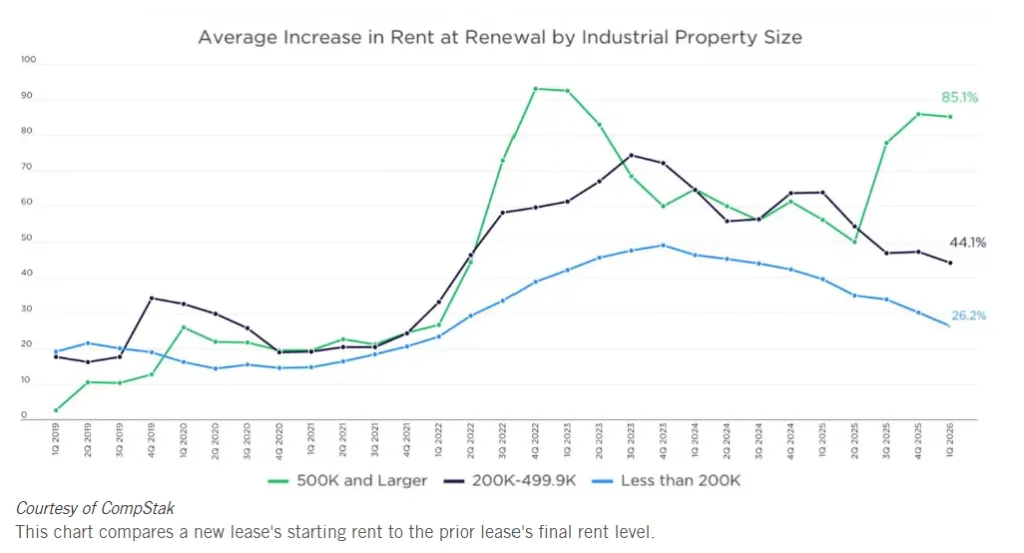

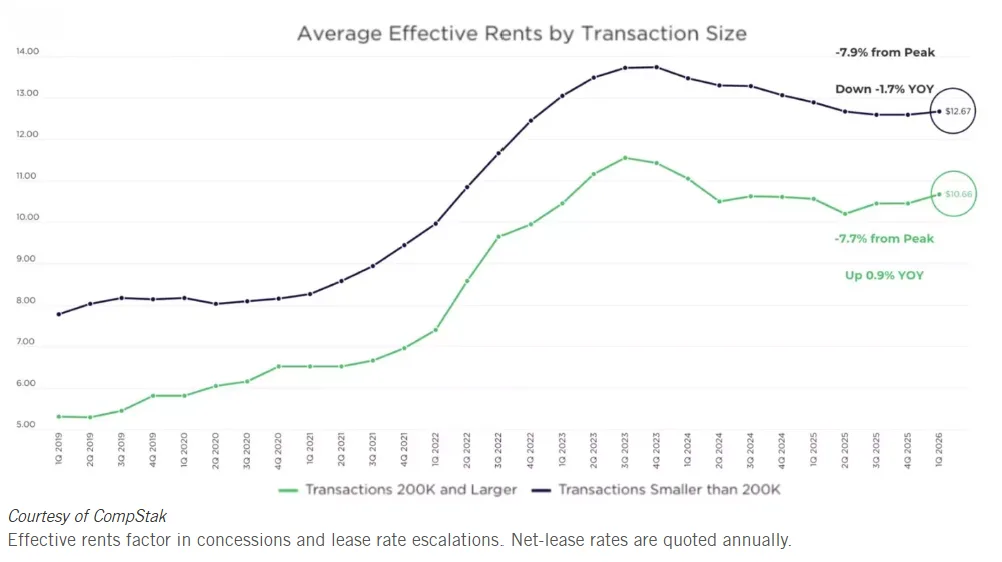

- Leasing activity for spaces over 500K SF is driving the sector, with effective rents for large renewals far outpacing smaller deals.

- Strong demand is restoring pricing power to landlords and supporting nationwide rent and absorption increases, tightening vacancy for big boxes.

America’s Pandemic-Era Warehouse Glut Shrinks Fast

After more than a year of sluggish activity in the US industrial market, big-box warehouse leasing has roared back. Bisnow reports that operators are signing deals over 500K SF at a pace reminiscent of the 2022 boom, drawn by the need for storage and supply chain certainty amid escalating global disruptions.

Demand is now outpacing the supply created in the wake of the pandemic, with tenants backfilling the record 1.5B SF of speculative space delivered in recent years. This reversal marks a significant departure from early 2025, when macroeconomic turbulence, trade wars, and energy shocks dampened appetite for major industrial facilities.

Vacancy for warehouses 750K SF and larger dropped to 7.3% in Q1 2026, compared to 8.3% a year earlier, according to Savills. Meanwhile, smaller big-box spaces (200K–500K SF) saw vacancy rise to 10.9%.

This divide highlights the outsized pressure—and opportunity—in the largest segment, as tenants increasingly favor modern Class-A properties that facilitate consolidation and operational efficiency.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Pandemic Supply Hangover Resolves

Between 2021 and 2024, developers bet heavily on future demand. They delivered a wave of new supply as market conditions weakened.

Post-pandemic optimism soon collided with tariffs, inflation, and geopolitical turmoil. As a result, the warehouse sector faced oversupply, and landlords lost pricing power.

The market shifted in the second half of 2025. By H1 2026, mega-leases fueled a sharp recovery.

Large deals lowered vacancy rates and lifted leasing activity to 490M SF. That marked a 27% year-over-year increase, according to Savills.

National industrial leasing volumes reached their highest levels since early 2022.

The Details

Several headline deals highlight the big-box recovery.

Tesla leased 682K SF in Austin and removed the market’s largest speculative warehouse. Meanwhile, Invesco completed a 522K SF lease worth $42M in the Inland Empire.

Third-party logistics firms continue to drive demand. JLL reports that 3PL companies leased more than 30M SF in Q1.

That total represented 20% of leasing activity and rose 65% from 2025 levels.

Many occupiers now consolidate older facilities into modern Class A buildings. Average lease sizes reached 210K SF in Q1 2026.

That figure sits 16.5% above 2019 levels.

CompStak reports that renewal escalations above 500K SF exceeded 84%. Those increases more than doubled rent growth for smaller spaces.

Large-Block Demand Squeezes Vacancy

Big-box absorption continues to outpace smaller-unit activity.

Smaller tenants returned more slowly after uncertainty disrupted decision-making. Global events also weighed on expansion plans.

Lease negotiations now take longer to complete. Prologis reported an average timeline of 59 days in Q1.

That figure exceeded the company’s seven-year average.

Occupiers appear more deliberate with major commitments. Large leases now carry greater strategic importance. This caution follows a broader industrial reset, as vacancy rates for newly delivered large facilities began tightening after several quarters of oversupply.

Industrial users also face record energy prices and trade uncertainty. Ongoing geopolitical tensions add more pressure.

Many firms now secure larger footprints in premium facilities. They want to reduce future supply chain risks.

The conflict between the US and Iran disrupted key transit routes. As a result, companies moved inventory closer to customers.

That strategy increased demand for well-located facilities with higher clear heights.

Why It Matters

The big-box recovery restored leverage that landlords lost after the supply surge.

CompStak reported 84% renewal escalations for leases above 500K SF in Q1 2026.

That figure exceeded the rate for smaller renewals by more than two times.

The data shows that logistics owners regained pricing power.

3PL firms now account for more than 20% of leasing activity. Their footprint continues to grow at a record pace.

Occupiers increasingly value scale and speed. They also seek cost certainty and inventory flexibility.

Class A buildings continue to absorb space quickly. Meanwhile, lower-tier properties remain stable.

JLL reports that average lease sizes for smaller properties held near 60K SF.

Industrial vacancy stayed near 8.2% nationwide. Large-block warehouses moved in the opposite direction.

Those properties tightened faster and attracted stronger tenants. They also supported higher pricing.

The market looks very different from 2025 conditions. Smaller users had largely remained on the sidelines.

Today, confidence has improved across tenant sizes. Still, large deals remain the sector’s primary growth engine.

What’s Next

Occupiers continue to reevaluate their distribution strategies. Older leases will also roll over in coming quarters.

As a result, negotiations will likely remain lengthy. Strategic reviews continue to extend decision timelines.

Developers will probably slow new construction activity. Many firms have already absorbed pandemic-era excess supply.

However, demand for premium facilities remains strong.

Cushman & Wakefield and Colliers expect continued strength in the 500K SF-plus segment through late 2026.

Effective rents should continue rising during that period. Vacancy for large blocks should continue falling.

Landlords will likely retain leverage on renewals and escalations. Tenants continue to compete for top-tier logistics space.