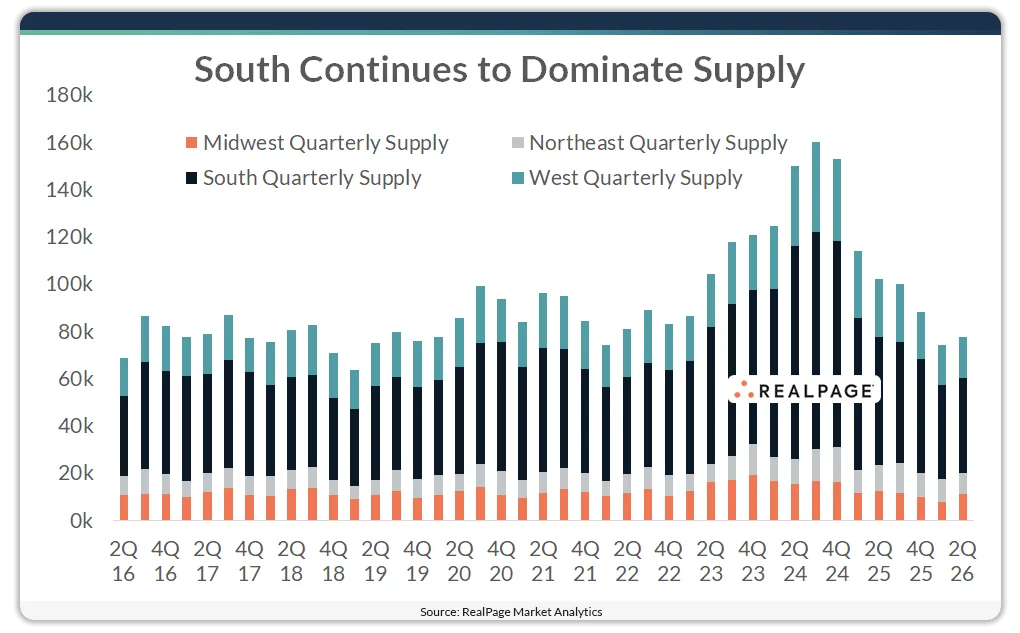

- US apartment completions rose modestly to 77,700 units in Q2 2026, per RealPage Analytics.

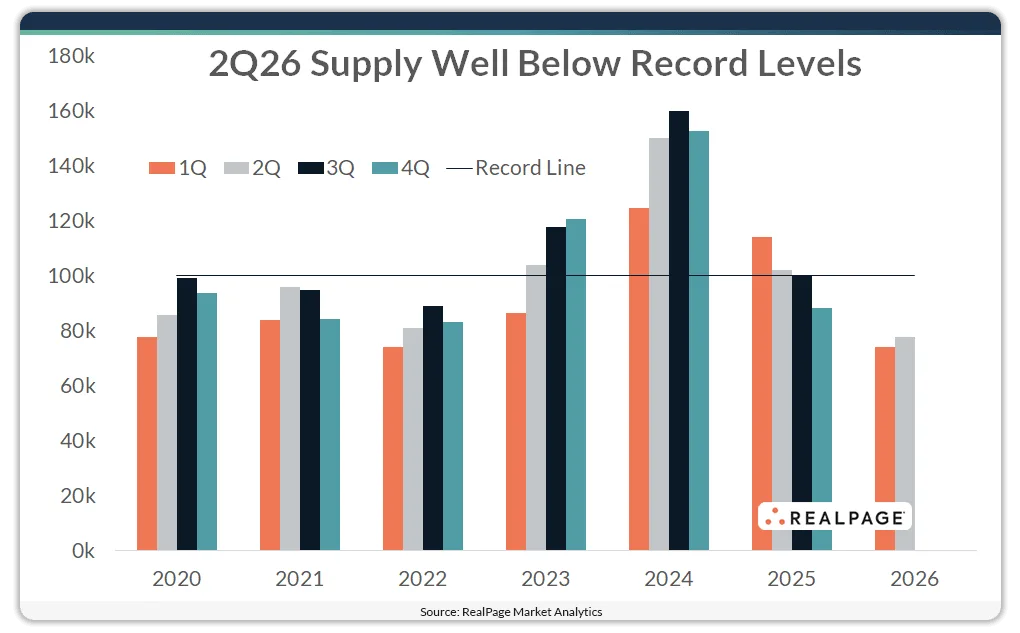

- Quarterly supply is still far below recent highs, with only the third sub-100,000 unit quarter in over three years.

- The South led completions, but even top markets like Dallas and Phoenix showed reduced momentum from the 2024 surge.

Post-Surge Apartment Supply Moderates

After an exceptional construction run that peaked in 2024, US apartment deliveries have entered a cooling phase. According to RealPage Analytics, Q2 2026 saw 77,700 new multifamily units completed—up modestly from 74,200 in Q1, but still only the third time in 13 quarters that deliveries fell below 100,000 units completed in a quarter.

That marks a sharp shift from the post-pandemic boom, when quarterly completions repeatedly broke new records as the sector raced to meet pandemic-driven demand. With the supply wave ebbing, developers and investors now face a normalizing pace of new inventory.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Q2 2026 delivered 77,700 completed units, slightly above Q1 levels but far below recent peaks.

Quarterly completions first exceeded 100,000 units in Q2 2023. That milestone started a six-quarter streak. Deliveries peaked at roughly 160,000 units in Q3 2024. Since then, completions have slowed as developers reduced starts and finished projects already underway.

Regionally, the South remained the clear leader with more than 40,000 completed units. That total more than doubled the West’s 17,400 units. It also exceeded the Midwest’s 11,200 units and the Northeast’s 9,000 units.

Still, the South delivered less than half its mid-2024 peak of 92,200 units. Dallas and Phoenix led major metros, each completing more than 4,000 units this spring.

Construction Volumes Reset

The decline in completions reflects a broader shift in multifamily construction cycles.

Developers faced higher costs, tighter financing, and shorter delivery timelines after the overheated 2023 and 2024 pipeline. Dallas and Phoenix still led metro deliveries. However, both markets reflect a nationwide pullback from aggressive expansion.

Oversupply, especially across Sun Belt markets, continues to pressure rents and occupancy. Although the South remains the supply leader, volumes have dropped sharply from record levels.

Softening demand and fewer starts continue to slow deliveries. As a result, the national market continues to normalize.

Why It Matters

Q2 2026 signals a new phase in the apartment sector’s supply story.

For investors, slower completions should reduce the supply overhang that defined 2024. According to RealPage Analytics, the 160,000-unit peak in Q3 2024 strained lease-up activity across many growth markets.

The recent slowdown could help restore balance in those metros. Lower supply and slower rent growth may help operators stabilize portfolios and improve occupancy. That shift comes as stronger leasing activity has started to reduce vacancies across several major apartment markets.

The construction reset also points toward more typical development risks and returns. That shift reduces oversupply risks but could slow growth in fast-expanding submarkets.

Sector watchers will notice the South’s continued dominance in multifamily construction. However, the gap between regions has narrowed as deliveries moved past their peak.

The South still delivered more than twice as many units as the West. Even so, the region’s 40,000-unit pace remains well below 2024 levels.

As the cycle evolves, expect more nuanced supply and demand trends at the metro level. The market will also draw clearer lines between stable and volatile growth markets.

What’s Next

Market participants continue to track signs of the next development cycle.

Developers will likely keep starts low through the rest of 2026. Meanwhile, lenders and sponsors continue to absorb existing supply.

As markets lease up peak-year deliveries, construction volumes should moderate further. That trend could reduce near-term pressure on rents.

Current pipelines suggest the post-2024 supply wave has largely passed. As a result, the multifamily sector could enter a more stable period for deliveries.

Dallas and Phoenix remain key markets to watch. Their performance should reveal how quickly the sector resets.