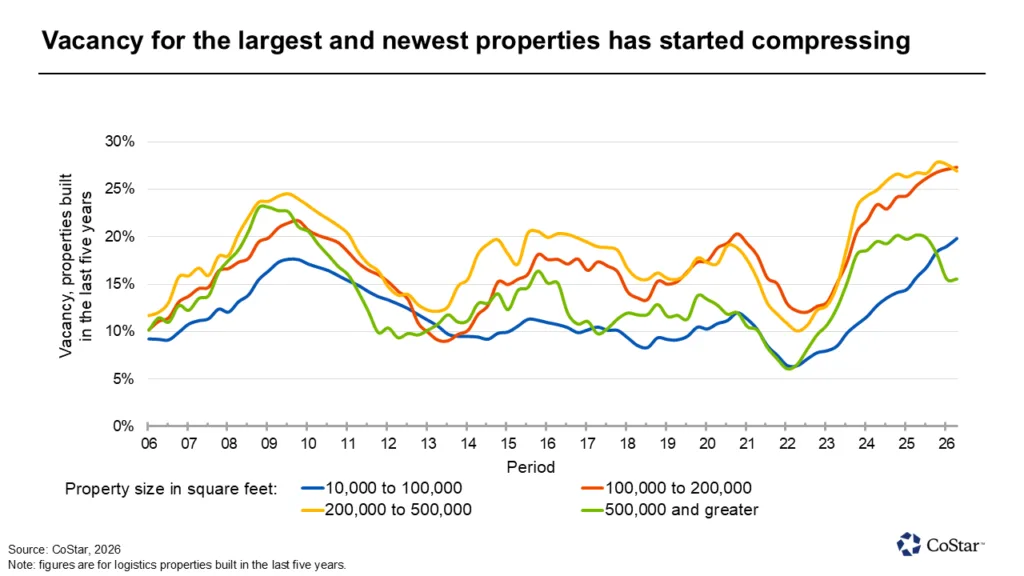

- Vacancy for US industrial properties over 500,000 SF is compressing as demand absorbs new supply, according to CoStar data.

- Mid-size and small-bay properties are facing higher vacancies due to increased supply, especially in markets like Phoenix and Austin.

- Shorter lease terms and uneven absorption highlight ongoing volatility across logistics and warehousing segments.

Newer Big-Box Space Drives Vacancy Compression

US industrial vacancy rates are tightening for properties over 500,000 SF, driven by robust demand for the largest and newest logistics assets. Business Wire reports that as of Q1 2026, build-to-suit deliveries and renewed appetite from large occupiers have helped push vacancy for this segment downward. Meanwhile, newer mid-size and small-bay industrial properties are experiencing a buildup in available space, reflecting uneven absorption trends across asset types.

Nationwide, large-scale logistics users have been active since late 2025, fueling absorption mostly through custom build-to-suit spaces. However, across the broader logistics market, vacancy rates tell a more nuanced story, as newer deliveries and regional supply gluts affect specific size categories differently.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Supply and Demand Diverge by Property Size

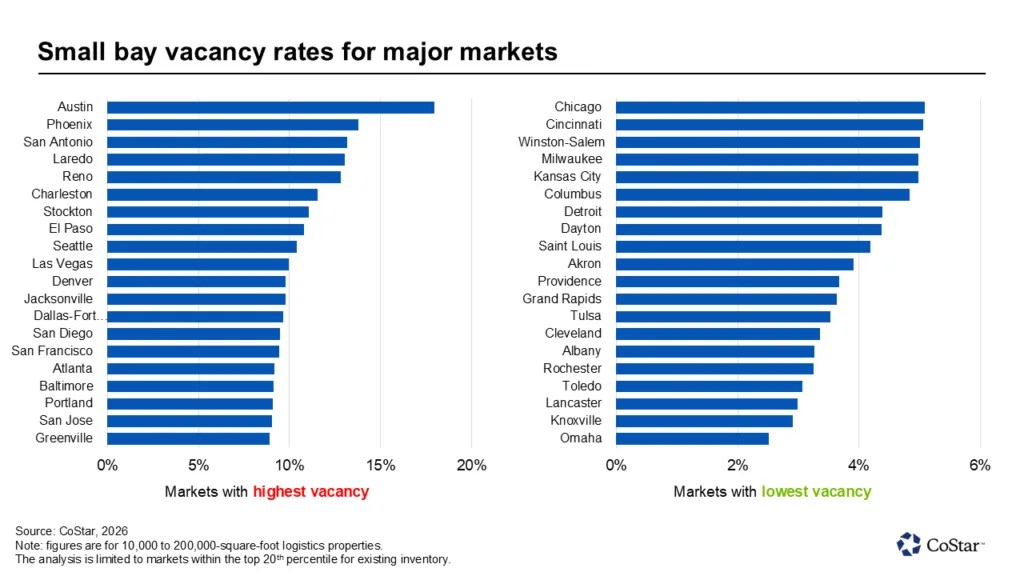

The US industrial landscape presents a tale of two markets: Large, new properties are seeing tightening availability, while vacancy climbs in mid-size and small-bay warehouses. According to CoStar, small-bay space (typically under 100,000 SF) maintains a vacancy rate of 6.4%, notably below the 10.9% average for the wider logistics sector—a sign of historically strong absorption and constrained construction. Yet, for new properties over 200,000 SF, especially at the mid-tier, supply is outpacing demand, leading to the highest vacancy levels in this cohort since 2006, except for the largest (over 500,000 SF) segment where absorption remains robust.

Leasing and Construction Volatility

Market dynamics illustrate a shift in tenant strategy. Juan Arias, national director of industrial analytics at CoStar Group, notes that average lease terms for the largest industrial spaces have declined from seven years in 2022 to five years in 2026. This trend reflects occupier concerns about supply chain disruptions and economic uncertainty, driving preferences for flexibility and shorter commitments.

Small businesses, contributors to small-bay demand, have pulled back on expansion amid macro volatility, moderating absorption for recent deliveries. Investors have also become more selective, as tenant-friendly conditions reshape leasing decisions across many industrial markets. Regionally, Phoenix and Austin have seen higher vacancy rates in the small-bay segment due to outsized new construction over the past few years, in contrast with tighter conditions in other markets.

Why It Matters

These trends highlight the risks and opportunities in industrial development. Large, new properties continue attracting tenants. Major retailers and e-commerce firms have resumed expansion plans. As a result, developers still support large build-to-suit projects.

However, shorter leases show that occupiers remain cautious. CoStar reports average lease terms fell from seven years to five. This shift makes cash flow less predictable. It also increases turnover risk for landlords.

Meanwhile, smaller and mid-size assets face rising competition. Deliveries exceed tenant demand in some markets. Small business confidence is also weakening. As a result, new projects may face longer lease-up periods. Investors should recognize this split. Well-located big-box space still draws steady demand. However, speculative projects in Phoenix and Austin face more uncertainty.

What’s Next

Demand for the largest logistics facilities will depend on retailers and e-commerce firms. If economic pressures persist, demand gaps may widen. Shorter leases could also become more common. That would increase risks for owners outside the big-box segment.

CoStar will keep tracking vacancies, leasing activity, and construction. For now, flexibility remains valuable. Tenants and owners must adapt to a more complex industrial market in 2026.