- CRE maturity stress is better reflected in loan terms, refinance capacity, and post-maturity behavior than simple extension counts.

- Banks have tightened extension terms post-2022, requiring more credit support from riskier borrowers, while CMBS loans face resolution drag due to structural constraints.

- Market risk is concentrated in low-debt-yield, office, and retail assets, where refinance and payoff are harder; headline maturity counts can misstate real risk concentration.

Refinance Pressure Splinters Simple Narratives

According to Trepp, large volumes of US commercial real estate debt are maturing in 2026 in a market marked by higher borrowing costs, patchy transaction activity, and volatile asset values. The shorthand “extend and pretend” suggests lenders are papering over losses by rolling maturing loans forward. But this broad brush misses key differences in how extension plays out across bank and CMBS loans—and what that tells us about real stress points in the market.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Easy Extensions Do Not Explain the Data

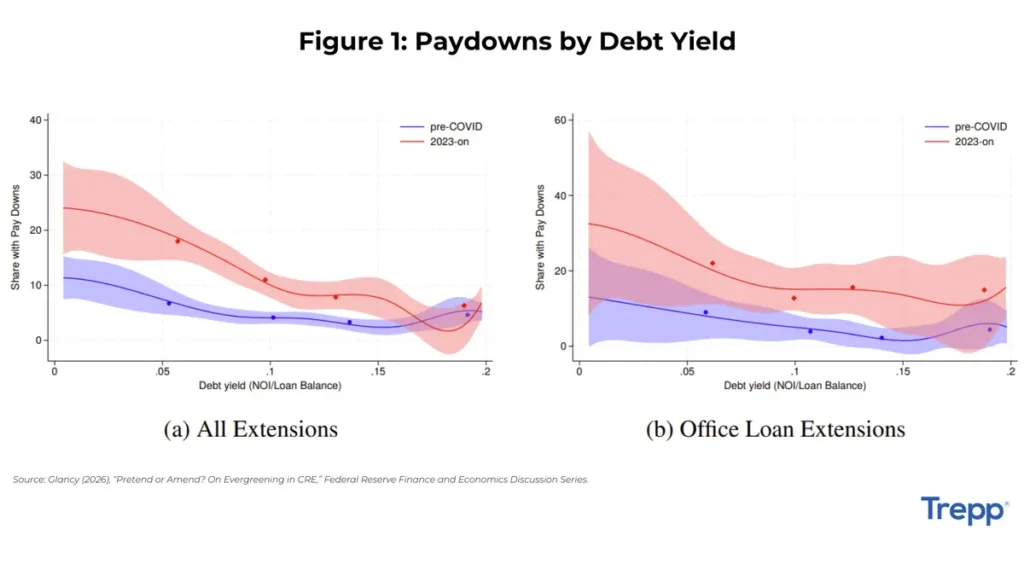

The “extend and pretend” view holds that lenders grant easy loan extensions to avoid recognizing losses, especially for weak loans. But Glancy’s 2026 research finds that after 2022, banks actually tightened extension standards. Low-debt-yield and nonrecourse borrowers were less likely to get extensions, and those approved had to provide paydowns, guarantees, or pay higher spreads. Extensions on riskier loans frequently involved more, not less, credit support, especially in the strained office sector. This shift aligns with broader trends in CRE lending, where loan modifications have increased as lenders work through refinancing challenges. Post-extension performance showed no wave of subsequent defaults, undermining claims that banks are broadly deferring loss recognition.

Maturity Drag Defines CMBS Stress

CMBS loans show stress differently. They often create “maturity drag,” where large balances remain unresolved after maturity. These loans do not always become delinquent. The CMBS trust and servicing structure slows modifications. At the same time, bondholder rules limit flexibility. Several factors increase maturity risk, including low occupancy, weak debt service coverage, and prior modifications. However, debt yield now stands out as the strongest warning sign. Lower property income relative to loan balance reduces refinancing options. It also lowers the chances of full repayment at current interest rates.

Most CMBS loans maturing in June 2026 performed as expected. However, some office and retail loans faced elevated risk. The highest-risk loans were already in special servicing or carried DSCRs below 1.0x.

Refinancing Bottlenecks Are Concentrated, Not Systemic

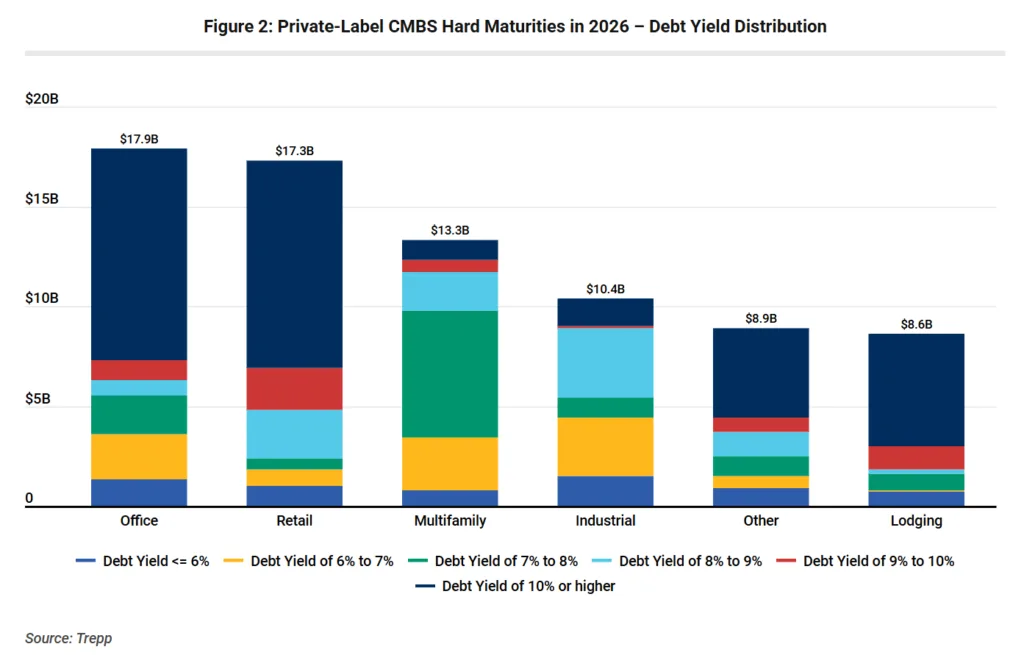

Refinancing stress remains concentrated within specific property groups. Older office buildings and regional malls face the greatest pressure. These assets often struggle with weaker cash flow, lower valuations, and limited market liquidity. Current data shows retail accounted for the largest share of June’s hard-maturing CMBS pool. However, office loans recorded the highest delinquency rate. This trend points to sector-specific challenges rather than broad market weakness. As refinancing options narrow, property fundamentals matter more. Credit quality and resolution terms increasingly determine outcomes. The volume of maturing loans alone tells only part of the story.

Why It Matters

For lenders and investors, reading CRE maturity stress solely through the lens of extensions can severely misjudge actual risk. Banks are negotiating tighter amendments rather than pushing weak credits forward on lenient terms. In CMBS, headline maturity balances overstate loss: actual risk is signaled by debt yield and the speed and structure of resolutions. Structural differences in how bank and CMBS loans are worked out shift where and how market stress appears, with asset type and income fundamentals now driving outcomes.

What’s Next

Markets should monitor whether debt yield continues to drive outcomes for maturing loans, particularly in office and retail. If banks ease on extension terms for weak borrowers, or if CMBS delinquency rates jump as unresolved loans transition to non-performance, that would point to a broader renewal of true extension-driven loss deferral. For now, watch for more targeted amendments, new equity injections, and NOI improvement as lenders attempt to navigate the refinancing gap without large-scale defaults—especially in assets at the intersection of valuation and leasing uncertainty.