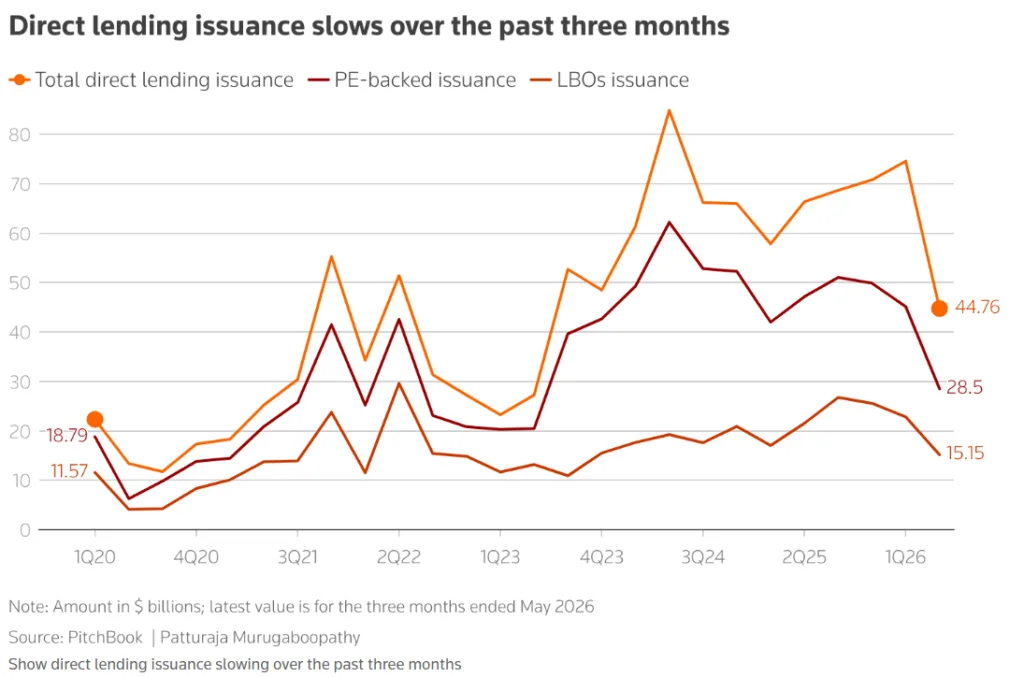

- Direct lending by US private credit lenders fell 40% to $44.8B in the three months ended May 2026, according to PitchBook.

- Funds including Blackstone and Cliffwater faced redemption requests exceeding 10%, triggering withdrawal caps and driving greater caution.

- Weaker issuance, tempered fundraising, and rising redemptions signal a new chapter for private credit, with heightened competition from syndicated loan markets.

Private Credit’s Surge Meets Resistance

The private credit boom that fueled US direct lending for much of the past five years is clearly on a downswing. Reuters reports that data from PitchBook shows new loan issuance by private credit lenders retreating sharply, dropping to $44.76B in the three months ended May 2026. That’s a steep 40% decline from the $74.56B seen in the prior quarter. After years of double-digit growth—and heavy demand from borrowers and investors—private credit lenders are wrestling with tougher market conditions and a marked shift in appetite, both from institutional and retail investors.

For context, June 2026 marks one of the lowest quarterly lending totals since the post-pandemic private credit surge. Despite growing assets under management at leading platforms like Blackstone, Ares, and Apollo, this pullback is sparking concern across the market. With direct lending to private equity-backed borrowers off nearly 37% and lending tied to leveraged buyouts down 34%, the industry is facing its most challenging test since the sector went mainstream.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

According to PitchBook, in the quarter ending May 2026, US direct lending issuance nearly halved. Loans to sponsor-backed borrowers tumbled to $28.5B, a near-37% drop, while leveraged buyout-related lending fell 34% to $15.15B. Redemptions surged: Blackstone and Cliffwater imposed 5% withdrawal caps on their private credit funds as investors sought to pull 10% of Blackstone Private Credit Fund shares and 17% from Cliffwater’s $31.3B vehicle. Fundraising levels also lagged recent highs: Preqin data puts total private credit commitments at $45B for the first four months of 2026—barely up from $44.5B for the same period last year, and well below 2023’s $52.2B tally for that window.

Elevated Scrutiny and Competitive Pressure

Competition from syndicated lenders is intensifying. Borrowers are shifting toward lower pricing and stronger liquidity. Meanwhile, investors are scrutinizing loan quality more closely. Software loans have become a key concern. The Morningstar LSTA US Leveraged Loan Index shows software loans fell 4.7% through May. The broader index gained 1.2% over the same period.

As a result, managers are tightening underwriting standards. They are becoming more selective and focusing on risk management. Investor demand is also weakening. Jefferies reported retail flows into alternatives fell 17% in May. Private credit flows dropped 35% and remained 70% below Q1 averages during Q2.

Why It Matters

Liquidity constraints, redemption demands, and tighter deal economics are reshaping private credit. As originations slow, large managers face pressure on fees, asset growth, and future earnings. Blackstone and Cliffwater imposed withdrawal limits after heavy redemption requests. Their actions signal growing stress, even among leading firms. Meanwhile, syndicated and traditional lenders are regaining market share. Borrowers also have more financing choices, forcing private lenders to compete harder on pricing and deal terms. As a result, private credit’s role as a one-stop capital source looks less certain.

Investor sentiment is also weakening. Preqin data shows fundraising remained subdued through early 2026. At the same time, retail flows, once a major growth driver, have slowed sharply. Jefferies reported steep declines in May allocations. Software credit adds another concern. Weak performance highlights growing asset quality risks that could widen spreads and reduce risk appetite.

The shift could affect commercial real estate finance. Private credit funds have become important liquidity providers across the sector. However, fewer loan deployments could raise borrowing costs and slow deal activity. Tighter capital availability may also force lenders to adjust underwriting standards through the rest of 2026.

What’s Next

Private credit managers appear to be bracing for continued outflows and softer origination pipelines through at least mid-year 2026. Market players will watch for stabilization in withdrawals and renewed fundraising momentum, particularly from institutional allocators. Managers are likely to focus on credit discipline and selective loan deployment, favoring sectors and deal structures that can weather increased scrutiny. As syndicated loans lure away more sponsor-driven deals, the risk/reward trade-off for private credit is evolving—and could reshape the capital stacks for CRE, LBOs, and middle market borrowers heading into Q3 and beyond.