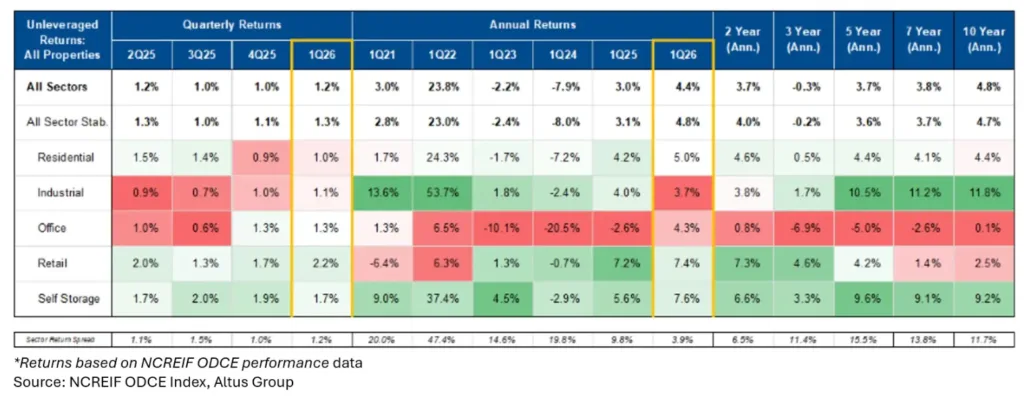

- The NCREIF ODCE Index returned 1.2% in Q1 2026, extending a streak of stable, income-driven performance across institutional real estate.

- Retail led all major sectors, while industrial, residential, and office results reflected growing differences between markets and asset quality.

- Investors are increasingly focused on long-term entry points as supply pressures ease and select sectors begin showing signs of recovery.

Private Market Stability Persists

According to Altus Group’s analysis of Q1 2026 NCREIF ODCE Index results, institutional-quality commercial real estate continued to deliver steady performance despite ongoing economic uncertainty. The ODCE Index posted a 1.2% unlevered total return during the quarter, driven primarily by property income rather than appreciation.

The results reinforce a trend that has emerged over the past year. While transaction activity remains below historical norms and interest rate uncertainty continues to weigh on capital markets, operating fundamentals across much of the private CRE market have remained resilient. Altus Group’s findings were echoed by public REIT earnings commentary, suggesting stability is extending across both private and public real estate markets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Retail Leads the Pack

Retail emerged as the strongest-performing major property sector in Q1, generating a 2.2% total return. Malls, neighborhood centers, and street retail assets all recorded positive appreciation, supported by strong leasing activity and healthy operating performance.

According to Altus Group, cash leasing spreads reached double-digit gains across both new and renewal leases, while same-store net operating income growth remained robust. The sector’s continued strength has surprised many investors given broader concerns around consumer spending and economic growth. However, retail landlords have benefited from years of limited new construction and a supply-demand balance that remains favorable compared to many other property types. Consumer spending trends remain the primary variable investors are watching as the year progresses.

Industrial and Residential Markets Split

Industrial performance continued to reflect significant regional differences. Southern California remained the sector’s biggest laggard, with warehouse rents in the Inland Empire falling another 2% during the quarter. The correction in one of the nation’s largest logistics markets has now stretched into its third year.

Elsewhere, conditions improved. Markets including Atlanta, Chicago, Dallas, Houston, and Phoenix posted positive appreciation as new supply deliveries slowed. Altus Group noted that the national industrial construction pipeline now equals roughly 1.7% of existing inventory, below the 10-year average of 2.6%.

Residential real estate displayed a similar divide. Gateway markets such as San Francisco, New York, and Chicago led performance as rent growth strengthened. Meanwhile, Sunbelt markets including Dallas, Raleigh, Orlando, Denver, and San Diego continued to face pressure from elevated apartment deliveries. San Francisco stood out in particular as AI-related job growth boosted rental demand while new housing supply remained limited.

Office Recovery Remains Selective

Office generated a 1.3% total return during the quarter, though property values across the sector remained negative overall. The results highlight how increasingly asset-specific office performance has become.

Positive appreciation appeared in select markets, including San Francisco, New York, Dallas, Houston, and Los Angeles. However, performance varied significantly even within the same submarkets. Higher-quality buildings with strong amenities and desirable locations continued attracting tenants, while less competitive assets struggled to maintain occupancy and rental rates.

That growing divide is influencing investment strategies. Many institutional investors are reassessing portfolio allocations and acquisition opportunities based on building quality, location, and leasing momentum rather than broader market averages. The trend mirrors what public office REITs have reported throughout the past year, with top-tier properties consistently outperforming weaker assets.

Why It Matters

The latest ODCE results suggest that US CRE fundamentals remain considerably stronger than many investors anticipated entering 2026. While capital markets remain constrained by higher borrowing costs and economic uncertainty, property-level performance continues to provide a measure of stability.

The quarter also reinforced an increasingly important theme across commercial real estate: sector and market selection matter more than broad asset-class exposure. Retail continues to benefit from limited supply growth. Gateway apartment markets are recovering as supply pressures ease. Industrial fundamentals are stabilizing in many regions despite ongoing challenges in Southern California. Even office is showing pockets of improvement where leasing activity remains healthy.

For investors, these trends create a more nuanced landscape than the broad-based downturn many feared. According to Altus Group, lower capital expenditure levels may indicate that landlords are beginning to see returns on investments made over the past several years, potentially supporting future leasing performance. At the same time, easing development pipelines across multiple sectors could improve fundamentals further if demand remains intact.

What’s Next

Attention is increasingly shifting toward investment timing. Industry participants continue to monitor interest rates, trade policy developments, and broader economic conditions, but many believe the market is approaching a more attractive point in the cycle for long-term capital deployment.

Supply conditions appear particularly supportive. Industrial development has slowed materially, apartment construction is expected to moderate after record deliveries in several Sunbelt markets, and retail remains one of the most supply-constrained sectors in commercial real estate. Those factors could provide a tailwind for operating performance over the next several years.

While uncertainty remains, Altus Group’s assessment points to a market transitioning from correction to opportunity. For investors with a three- to seven-year investment horizon, 2026 and 2027 may offer some of the most compelling entry points seen since interest rates began rising earlier in the decade.