- US apartment occupancy reached 95.5% in May 2026, extending a five-month recovery that has lifted occupancy 90 basis points since year-end 2025.

- Rent growth continued nationwide, but elevated apartment supply kept downward pressure on pricing in several Sun Belt metros, including San Antonio, Austin, and Phoenix.

- Coastal tech markets and supply-constrained Midwest cities are increasingly driving apartment rent growth as new deliveries moderate across parts of the country.

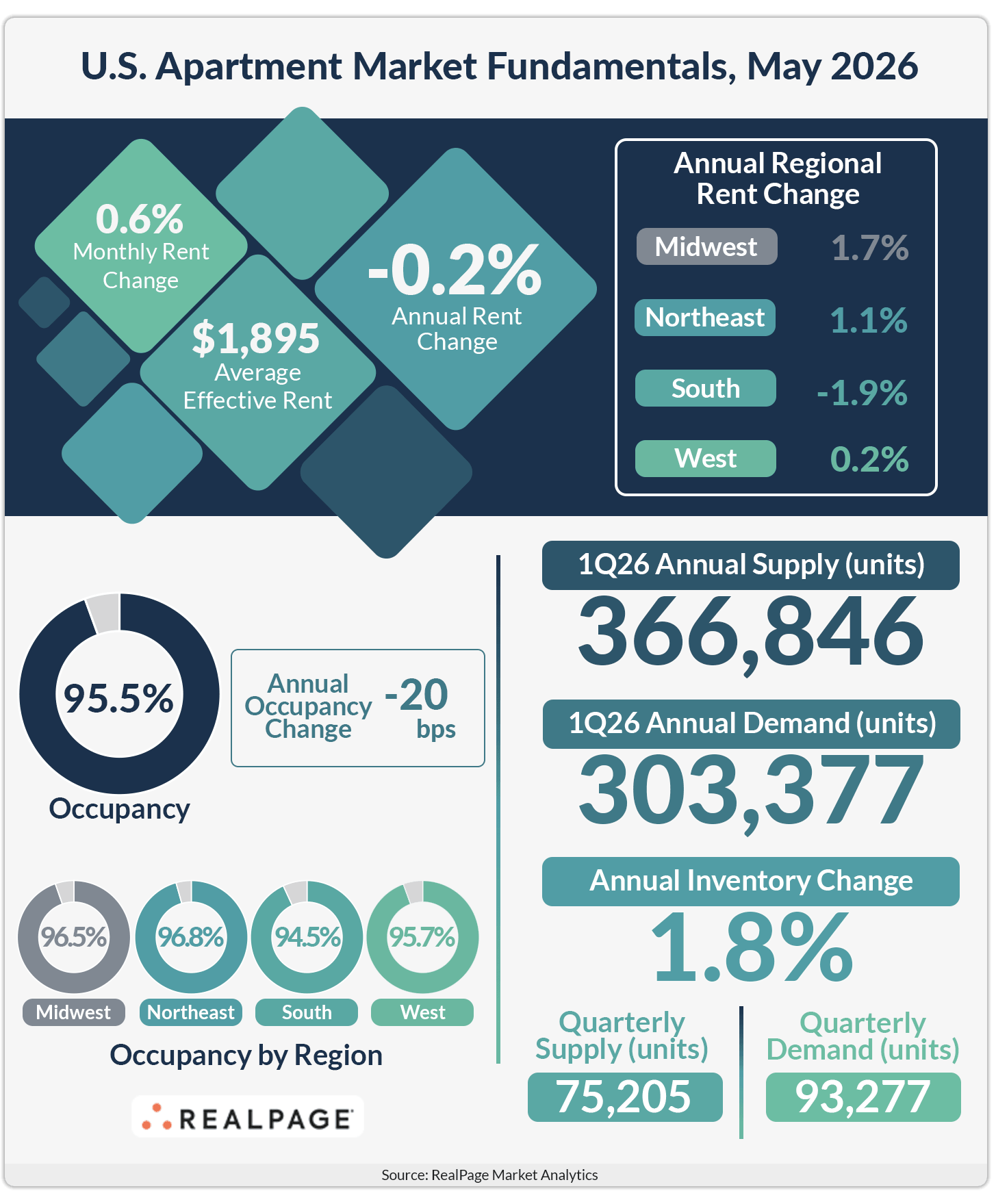

According to RealPage Market Analytics, the US apartment market continued its gradual recovery in May, posting a fifth consecutive month of gains in both occupancy and effective asking rents. Occupancy reached 95.5%, up 30 basis points from April and 90 basis points higher than at the end of 2025.

The improvement follows a challenging second half of 2025, when apartment fundamentals weakened amid elevated supply deliveries and softer leasing demand. While occupancy has rebounded steadily this year, the national rate remains 20 basis points below the 95.7% level recorded in May 2025, highlighting how far the market still has to climb.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Steady Turnaround

The apartment sector entered 2026 under pressure from one of the largest construction pipelines in decades. New deliveries across many Sun Belt markets outpaced demand growth throughout much of 2024 and 2025, forcing operators to lean on concessions and absorb lower occupancy levels.

That dynamic appears to be easing. Occupancy has now increased every month this year, suggesting renter demand is beginning to catch up with supply. The rebound has been broad enough to support modest rent gains as well. Effective asking rents rose 0.6% in May, extending a streak of monthly increases that began in January.

Still, the recovery remains measured rather than explosive. Despite five straight months of rent growth, national rents remained 0.2% below year-earlier levels, indicating that operators are still working through the impact of previous pricing declines.

The Details

All four US regions recorded monthly rent growth in May, according to RealPage data. The West delivered one of the more notable improvements, pulling itself out of annual rent contraction territory after months of weakness.

The South remains the lone region posting year-over-year rent declines and is also the only region where apartment occupancy remains below 95%. Occupancy across the Northeast, Midwest, and West hovered around 96% or higher during May.

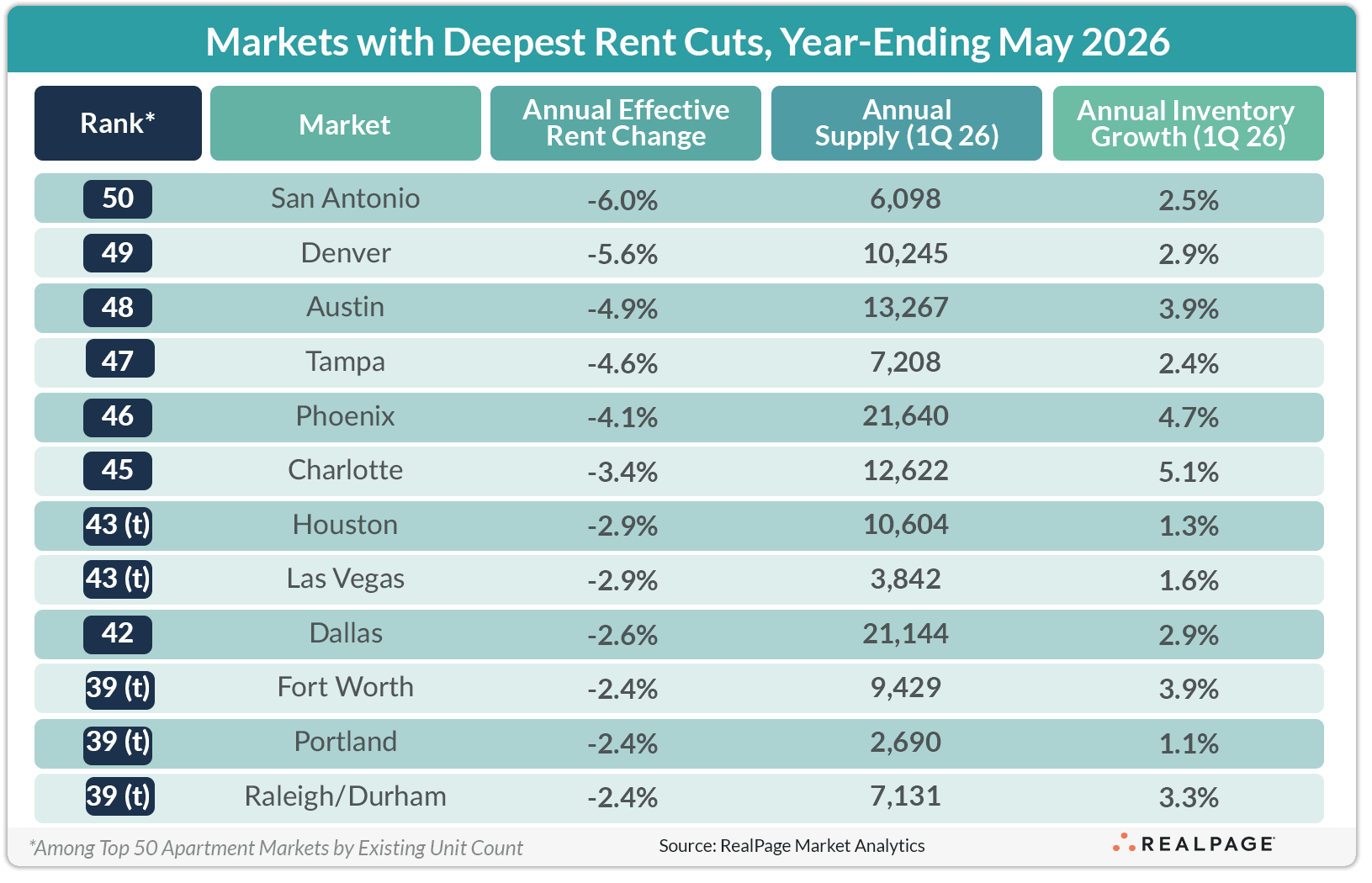

At the metro level, supply-heavy Sun Belt markets continued to struggle. San Antonio posted the largest annual rent decline among the nation’s 50 largest apartment markets at 6%. Denver followed with a 5.6% decline, while Austin recorded a 4.9% drop. Austin’s performance nevertheless represented an improvement, marking the first time annual rent declines have narrowed below 5% since July 2023.

Phoenix and Charlotte also remained under pressure, posting annual rent declines of 4.1% and 3.4%, respectively.

Diverging Regional Performance

The gap between high-supply and low-supply markets remains one of the defining themes of the apartment sector in 2026. Markets that experienced aggressive construction activity during the past several years continue to face pricing pressure as operators compete for residents.

That trend is especially evident across the Sun Belt, where inventory growth remains elevated relative to demand. Tourism-oriented markets have faced additional challenges. Tampa reported annual rent declines of 4.6%, while Las Vegas saw rents fall 2.9% year over year as softer consumer confidence weighed on discretionary travel activity.

Meanwhile, markets with more constrained development pipelines are seeing stronger pricing power. Several Midwest metros have quietly emerged as steady performers. Milwaukee posted annual rent growth of 3.5%, while Chicago recorded a 3.1% increase. St. Louis, Minneapolis, Detroit, and Kansas City each generated gains around the 2% range.

Why It Matters

The latest data suggests the apartment sector is moving beyond the worst effects of the supply wave that dominated industry conversations over the past two years. While new deliveries remain historically elevated in some markets, occupancy trends indicate demand is absorbing much of that inventory.

For investors and operators, the recovery offers evidence that fundamentals are stabilizing even if rent growth remains muted. Occupancy gains typically precede stronger pricing power, making the current trend an important signal for multifamily performance heading into the second half of 2026.

What’s Next

The next phase of the apartment recovery will largely depend on how quickly supply pressures ease in the nation’s most active development markets. As construction starts continue to slow, many industry observers expect inventory growth to moderate over the next year, potentially improving pricing conditions for landlords.