- Retail landlords nationwide are at or near full occupancy, but new retail construction is stalled by high costs and uncertain economics.

- The tightest markets, like Texas, are driven by population growth and major grocery-anchored developments, while many regions see few new projects breaking ground.

- Landlords are buying leases out of bankruptcy to regain control of quality space as tenant churn and limited new supply influence retail real estate strategy nationwide.

Retail Availability Plummets as New Projects Pause

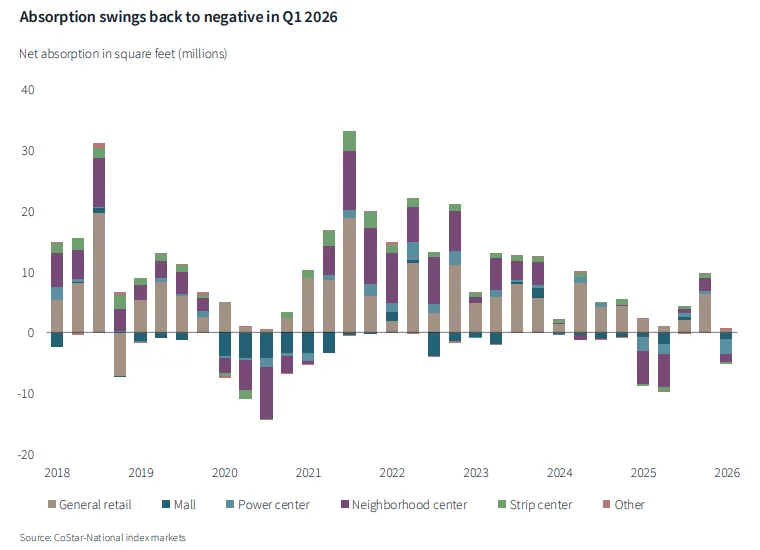

The US retail sector is tighter than it has been in years, with landlords across major markets reporting portfolio occupancy levels near historic peaks well into 2026, per Bisnow. High interest rates and tariffs, however, keep the pipeline for new retail product at a standstill. This squeeze follows a mixed Q1, as 4.4M SF of negative absorption marked a sharp reversal after two quarters of increasing occupancy, according to JLL’s 2026 market report.

Development Barriers Persist

Elevated borrowing costs and rising construction expenses make new ground-up retail even less feasible than comparable multifamily or industrial projects, JLL’s Danny Finkle noted at the 2026 NAREE Conference. Developers face reluctant lenders and higher cost thresholds, with many unwilling to break ground without a high percentage of pre-leasing from national brands. For today’s tenants—ranging from big-box chains to specialty grocers—preferences around format, size, and layout limit speculative projects even further.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Texas Remains a Notable Exception

Texas continues to outperform, led by population growth and a surge in grocery-anchored mixed-use projects, particularly from chains like H-E-B, said Weitzman’s Ian Pierce. The firm reported 44M SF in Texas retail leases, with Dallas-Fort Worth logging a fourth consecutive year of record occupancy—much of it driven by the strength of supermarket-anchored assets. Other anchor retailers, including Walmart, Costco, and Home Depot, remain active acquirers and tenants in the state, a notable contrast to most US metros.

Disrupted Tenancy Drives Landlord Action

With tight supply and little prospect of relief, vacancy doesn’t linger: landlords are responding to retail bankruptcies by buying leases and repositioning assets to drive stronger rents. Some property owners have moved quickly to replace failing chains—like Big Lots and Party City—with competitors or completely new concepts, captured at higher PSF rates. Finkle underscored how this power shift favors landlords, citing the rise in landlords purchasing vacated leases out of bankruptcy to control release strategies directly—a trend evident following the spate of filings by Saks Global and West Marine in 2026.

Why It Matters

The tightening supply caps some retailers’ expansion potential despite healthy consumer demand. According to JLL, a lack of new development will keep occupancy rates elevated, but rent growth could slow if tenants balk at unattractive renewal terms. Industry observers see continued pressure on margins for developers and retailers, with only well-capitalized, pre-leased projects making the cut in most markets. The pivot to experiential and service-focused retail further complicates the calculus, as centers seek tenants who offer defensibility against e-commerce and cyclical shocks.

What’s Next

Until interest rates ease or cost structures shift, large-scale retail development looks likely to remain on pause nationwide. Adaptive reuse, repositioning, and bankruptcy-linked dealmaking will headline activity for the remainder of 2026. CRE professionals should pay close attention to how much rent growth landlords can extract in a full-occupancy world and whether the Texas expansion model can materialize elsewhere. The timeline for a new supply cycle appears tethered to both broader capital markets and tenant willingness to precommit in a highly selective expansion environment.