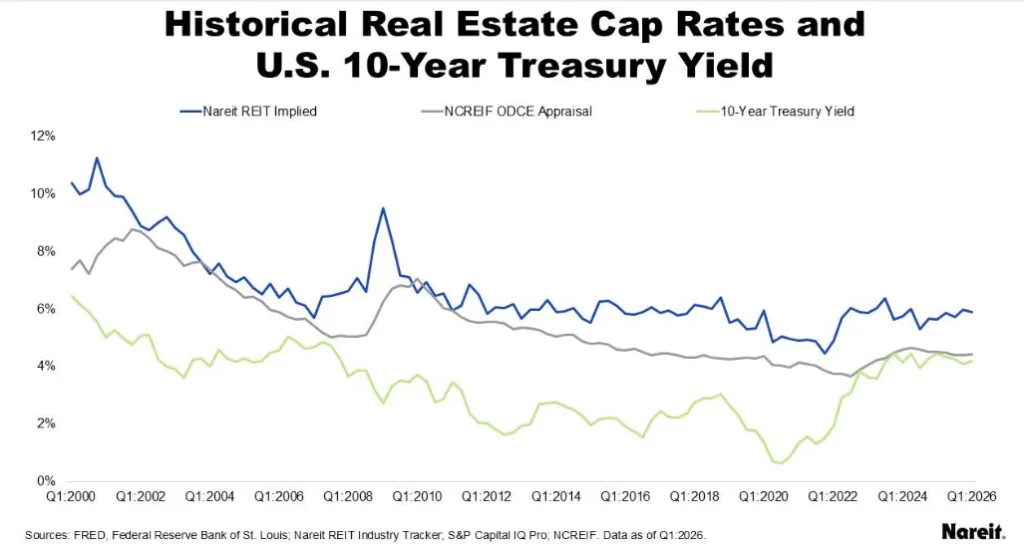

- Private real estate cap rates have stalled near 2021 levels, failing to reflect higher market yields since then.

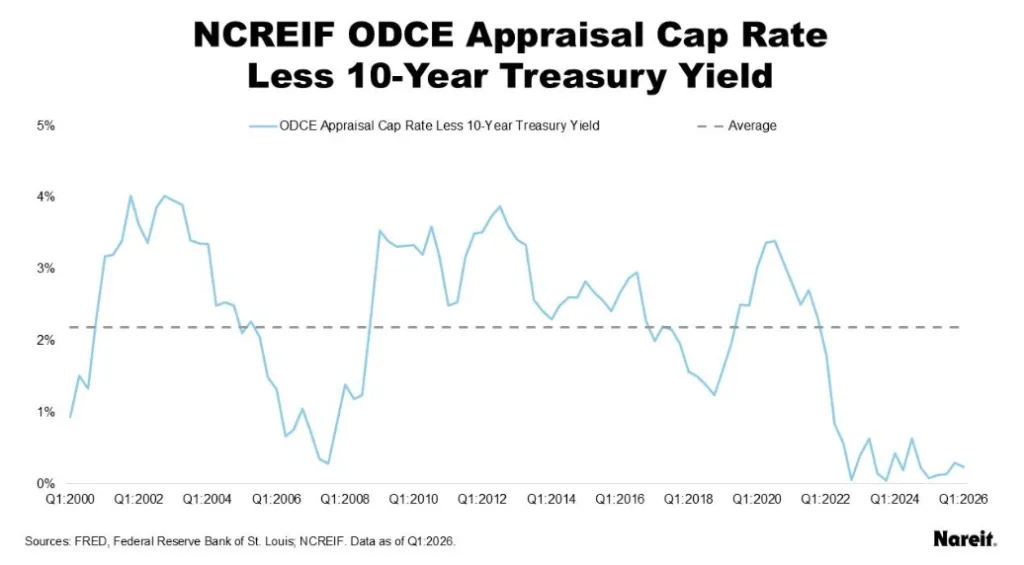

- The spread between appraisal cap rates and US 10-year Treasury yields averaged just 26 basis points across the last 14 quarters.

- This disconnect raises concerns for private valuations, while REITs may stand to outperform as appraisal marks eventually catch up to market reality.

Private Cap Rates Show Little Movement

Private real estate appraisal cap rates, based on NCREIF ODCE fund data, have barely budged since the end of 2021. Despite rising interest rates and market volatility, appraisers and portfolio managers have largely kept valuations static, diverging sharply from the more responsive REIT market. For the past three years, appraisal cap rates have hovered at levels that matched year-end 2021 REIT implied cap rates, according to Nareit commentary published June 3, 2026.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Persistent Spread Compression Defies History

Historically, the spread between private appraisal cap rates and the US 10-year Treasury yield has averaged 219 basis points since 2000. That spread shrank below 50 basis points only 14 times during this period—twice during the global financial crisis, and 12 times over the last 14 quarters amid today’s valuation dislocation. Over this most recent period, the spread averaged just 26 basis points, as interest rates climbed and appraisals failed to reprice. By comparison, REIT implied cap rate spreads averaged 171 basis points, while Moody’s seasoned Aaa corporate bonds averaged 94 basis points above Treasuries.

Prolonged Divergence Signals Market Adjustment Ahead

This stubborn disconnect highlights the challenges in private market valuation practices during a rising rate environment. For most of 2024 and through Q1 2026, appraised values have not adjusted to the higher cost of capital. Notably, recent US 10-year yields have exceeded NCREIF ODCE appraisal cap rates, an unusual and unsustainable dynamic. For institutional investors and managers, the message is clear. Current private valuations may soon need to align with broader market conditions as mark-to-market adjustments begin to materialize.

Why This Trend Matters for Investors

The persistence of modest spreads in private real estate cap rates creates risk for asset owners, as future valuation write-downs become increasingly likely. REITs, whose cap rates have reset more quickly, could benefit by comparison. According to Nareit, REITs are positioned for relative outperformance as private appraisals are forced to adjust. Investors should monitor ongoing cap rate movements alongside Treasury yields as a barometer for looming valuation changes in private portfolios.

Treasury yields represent the benchmark risk-free rate, while corporate bond spreads and REIT pricing offer additional signals about investor risk appetite. The fact that private appraisal cap rates have remained so close to Treasury yields suggests that valuations may not fully reflect today’s financing environment.

The disconnect also affects competition between public and private real estate. Public REITs have already absorbed much of the market’s repricing. That could leave them better positioned if private valuations move lower. Investors comparing public and private vehicles will likely focus on whether reported property values align with current market conditions.

What’s Next for Private Appraised Valuations

The next phase of the debate will depend on interest rates, transaction activity, and appraisal adjustments. If Treasury yields remain elevated, pressure could build on private valuations. The same could happen if property sales continue to close below appraised values.

Nareit believes private markets will eventually align with broader market signals. Appraised values tend to move toward observable transaction pricing over time. The key question is how quickly that adjustment occurs.

For now, the public-private valuation gap remains one of commercial real estate’s most closely watched stories. Investors are searching for pricing clarity in a higher-rate environment. As a result, cap rates, Treasury yields, and REIT valuations will remain critical indicators.