- The Federal Reserve identified redemption pressure in private credit funds as a growing financial stability concern, despite broader resilience across the banking system.

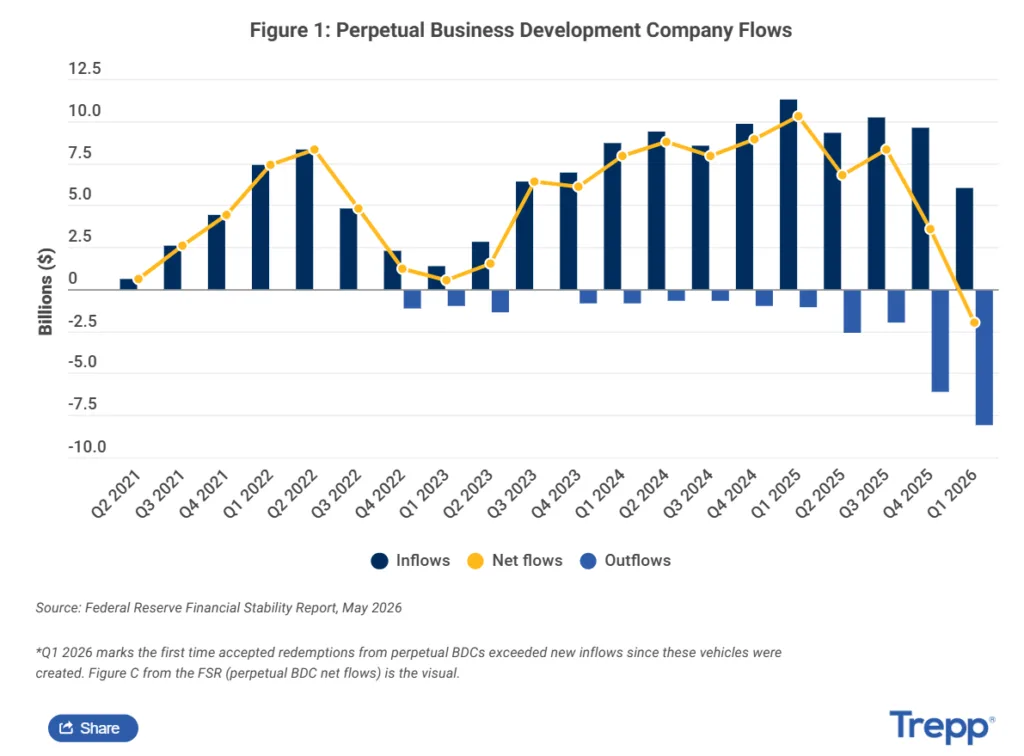

- Accepted redemptions at perpetual BDCs exceeded new inflows for the first time in Q1 2026, testing liquidity across a rapidly expanding lending segment.

- For CRE, the primary risks remain CMBS refinancing challenges and potential lending pullbacks from private credit providers serving transitional assets.

According to the Federal Reserve’s May 2026 Financial Stability Report, the US financial system remains resilient despite growing pressure in select markets, per Trepp. The report highlighted private credit after perpetual business development companies (BDCs) recorded net outflows for the first time since the vehicles were introduced.

The development comes as CRE fundamentals continue to stabilize after several years of valuation declines and higher interest rates. The Fed found limited evidence of broad CRE stress. However, it identified refinancing risk and private credit spillover effects as areas that deserve closer attention.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Private Credit Faces Its First Liquidity Test

Private credit has grown rapidly over the past several years, filling lending gaps left by banks that pulled back from certain sectors following higher capital requirements and rising rates. The sector became an increasingly important source of financing for middle-market companies and transitional commercial real estate projects.

That growth is now facing its first meaningful liquidity challenge. The Fed reported that accepted redemptions from perpetual BDCs exceeded new investor inflows during Q1 2026, marking the first quarterly net outflow since the products were launched. Investor concerns around interest rates, credit performance, and asset quality contributed to weaker demand. While most funds enforced standard quarterly redemption limits, the shift represents an important test for a market that has largely expanded under favorable fundraising conditions.

The Details

The Federal Reserve characterized current redemption pressure as manageable rather than systemic. According to the report, the 10 largest perpetual BDCs, which collectively control roughly 80% of sector assets, maintain sufficient liquidity through cash reserves and bank credit facilities to absorb at least three quarters of redemptions at currently capped levels.

The concern is less about today’s withdrawals and more about what happens if redemption requests accelerate. Should investor sentiment deteriorate further, private credit managers could face pressure to preserve liquidity by reducing new loan originations or selling assets into weaker markets. Either outcome could affect borrowers that have become increasingly dependent on private credit financing.

The report also noted that most funds continue to utilize redemption caps effectively, allowing managers to spread liquidity demands across multiple quarters rather than forcing immediate asset sales.

Banks Remain the Key Transmission Channel

The broader financial stability question centers on the connection between private credit and traditional banks. While private credit often operates outside the regulated banking system, it remains heavily linked to banks through revolving credit facilities and financing arrangements.

The Fed reported that bank credit commitments to nonbank financial institutions reached $2.6T during Q4 2025. Commitments tied to private equity firms, BDCs, and private credit platforms increased 17% year over year. As investor inflows slow, many private credit funds rely more heavily on these facilities to meet liquidity needs.

Bank executives have largely downplayed concerns so far. During Q1 2026 earnings calls, several super regional banks described their non-depository financial institution portfolios as investment-grade, highly collateralized, and among their lowest-loss lending categories. Still, the growing scale of these relationships means continued stress within private credit could eventually affect bank balance sheets and lending capacity.

Why It Matters

For CRE, the Fed’s findings suggest that market risk is shifting away from property fundamentals and toward financing channels.

The report found that CRE prices have largely stabilized after the declines seen between mid-2022 and early 2024. Capitalization rates have recovered from historic lows. Bank CRE loan delinquencies also remained relatively stable through the end of 2025. Many lenders have managed exposure through extensions, modifications, and additional collateral requirements.

The bigger concern is refinancing. The Fed identified maturing private-label CMBS loans as a key vulnerability. It noted that lenders may become less willing to extend loans as large volumes of debt come due.

Private credit adds another layer of risk. The sector has become an important funding source for transitional properties that often fall outside traditional bank lending. If redemption pressure causes funds to pull back, borrowers could face fewer refinancing options. That could create stress even when property performance remains stable. In that scenario, access to capital becomes more important than asset fundamentals.

What’s Next

The Federal Reserve’s overall assessment remains relatively constructive. Banking capital levels remain strong, household and business leverage continue trending lower, and aggregate funding risks are viewed as moderate.

The key question moving forward is whether private credit redemption pressure proves temporary or develops into a longer-term trend. Current liquidity buffers appear sufficient, but sustained outflows could force managers to reduce lending activity or rely more heavily on bank facilities.

For CRE investors and lenders, the focus will remain on two areas: refinancing activity within private-label CMBS and capital availability for transitional assets that depend on private credit funding. While neither poses an immediate systemic threat, both could influence deal flow and financing conditions throughout the remainder of 2026.