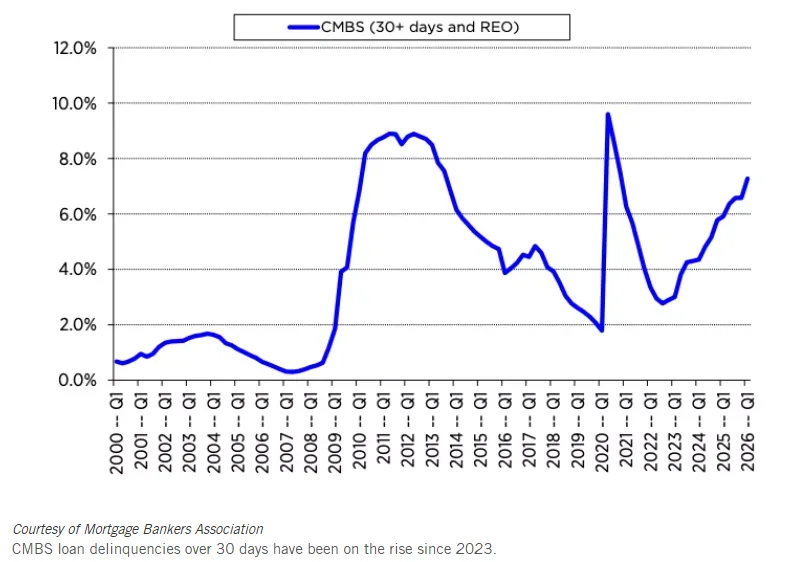

- Multifamily CMBS delinquencies rose to 7.28% in Q1 2026, extending a steady increase that has persisted since 2023, according to the Mortgage Bankers Association.

- Elevated interest rates, softer rent growth, and a more challenging refinancing environment are putting pressure on apartment borrowers, particularly those with loans originated in 2023 and 2024.

- The trend signals growing stress in portions of the multifamily market even as broader commercial mortgage performance remains relatively stable across several lending channels.

Multifamily loan distress is becoming harder to ignore as apartment owners contend with elevated borrowing costs and sluggish rent growth. New MBA data shows multifamily CMBS delinquencies continued rising during the first quarter of 2026. The increase highlights challenges for borrowers seeking to refinance maturing debt.

The pressure comes as the Federal Reserve maintains a higher-rate environment and investors reassess expectations for interest-rate cuts that many expected at the start of the year.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Growing Delinquency Trend

According to MBA’s Commercial Delinquency Report released June 2, multifamily CMBS delinquencies reached 7.28% in Q1 2026, up 70 basis points from the previous quarter. The rate measures loans that are at least 30 days delinquent or in real estate owned (REO) status.

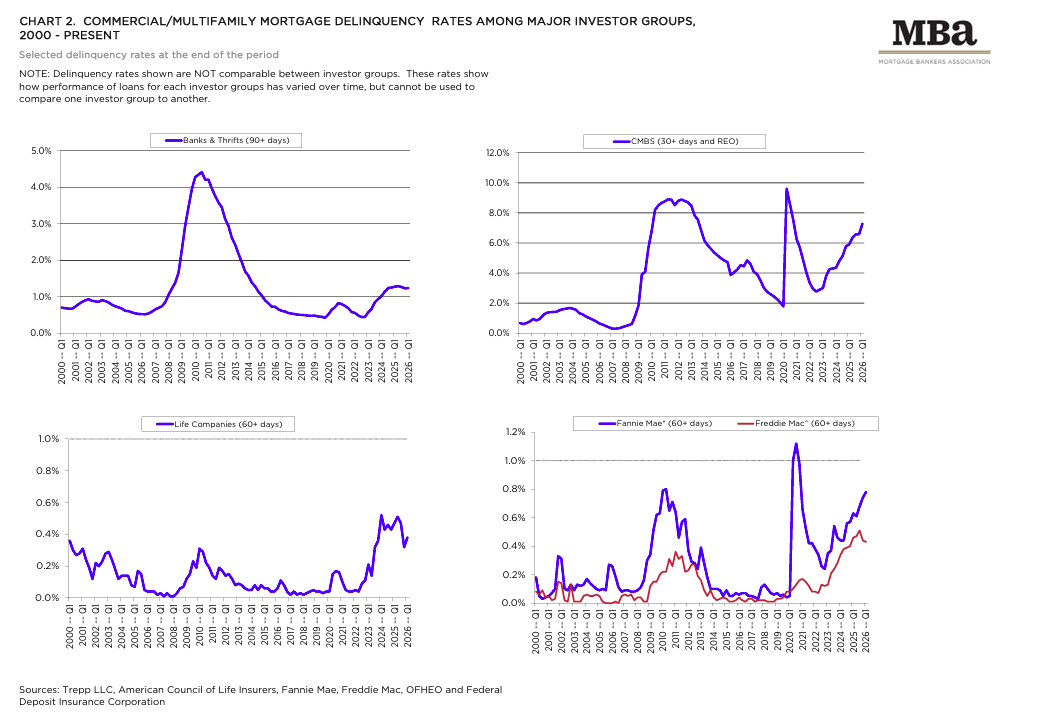

Fannie Mae multifamily delinquencies also increased, rising 4 basis points quarter-over-quarter to 0.78% for loans that are 60 or more days delinquent. By contrast, Freddie Mac’s delinquency rate declined slightly to 0.43%, while bank and life company portfolios remained relatively stable, according to MBA.

MBA Associate Vice President of Commercial Research Reggie Booker said loan performance remains generally healthy across much of the market. However, rising CMBS and Fannie Mae delinquencies point to ongoing pressure from refinancing challenges and higher borrowing costs.

The Refinancing Challenge

Industry observers point to the financing environment as a primary driver of multifamily loan distress. At the National Association of Real Estate Editors Conference in Miami, MBA Associate Vice President Judith Ricks discussed challenges facing multifamily borrowers. She said economic uncertainty and elevated interest rates have weakened refinancing options. As a result, borrowers with maturing debt are finding it more difficult to secure new financing.

Treasury yields have remained elevated throughout 2026, according to market data cited by Bisnow.

The 10-year Treasury reached 4.6% in May before settling just below 4.5% in early June. Meanwhile, the Federal Reserve has left benchmark rates unchanged through three consecutive meetings.

Ricks noted that refinancing conditions were more favorable in late 2025, when market fundamentals supported loan modifications and refinancings. That environment has since become more challenging, leading MBA to revise expectations for loan originations and interest-rate policy this year.

The association now expects multifamily loan origination volumes to decline in 2026 compared with 2025.

The forecast reflects growing refinancing challenges for borrowers with existing debt obligations.

Weak Rent Growth Adds Pressure

Financing challenges are arriving at the same time apartment fundamentals are cooling in many markets. National apartment rents increased just 0.7% year-over-year in May 2026, according to Apartments.com.

While rent growth remains positive, it has slowed considerably from the levels many owners underwrote during the post-pandemic apartment boom. For borrowers facing higher debt-service costs, limited revenue growth reduces flexibility when refinancing or restructuring loans.

Ricks also pointed to signs of weakness among multifamily loans originated in 2023 and 2024. While MBA is still gathering additional data, the organization is tracking reports of increasing short-term delinquencies among those vintages.

Multifamily CMBS Delinquencies in Market Context

The apartment sector remains one of the most closely watched property types in commercial real estate. A wave of new supply across Sun Belt markets has moderated rent growth, while elevated interest rates have compressed property values and refinancing proceeds.

Unlike office distress, which has dominated headlines over the past several years, multifamily challenges stem largely from capital markets conditions rather than structural demand issues. Occupancy levels remain relatively healthy in many markets, but borrowers with floating-rate debt or loans approaching maturity are facing a tougher path forward.

Why It Matters

Rising multifamily CMBS delinquencies offer one of the clearest indicators that higher-for-longer interest rates are beginning to affect apartment owners’ ability to service debt. With CMBS delinquency rates reaching 7.28% in Q1 2026, according to MBA, lenders, servicers, and investors are paying closer attention to refinancing risk across the sector.

The trend also underscores how modest rent growth can magnify financing pressures when debt costs remain elevated.

What’s Next

The key variable for multifamily borrowers remains the interest-rate outlook. MBA now expects rates to remain higher than anticipated earlier in the year, potentially limiting refinancing activity through the remainder of 2026.

Investors should watch delinquency trends among 2023 and 2024 loan vintages, along with apartment rent growth and Treasury yields. If refinancing conditions fail to improve, multifamily CMBS delinquencies could continue moving higher even as broader commercial mortgage performance remains relatively resilient.