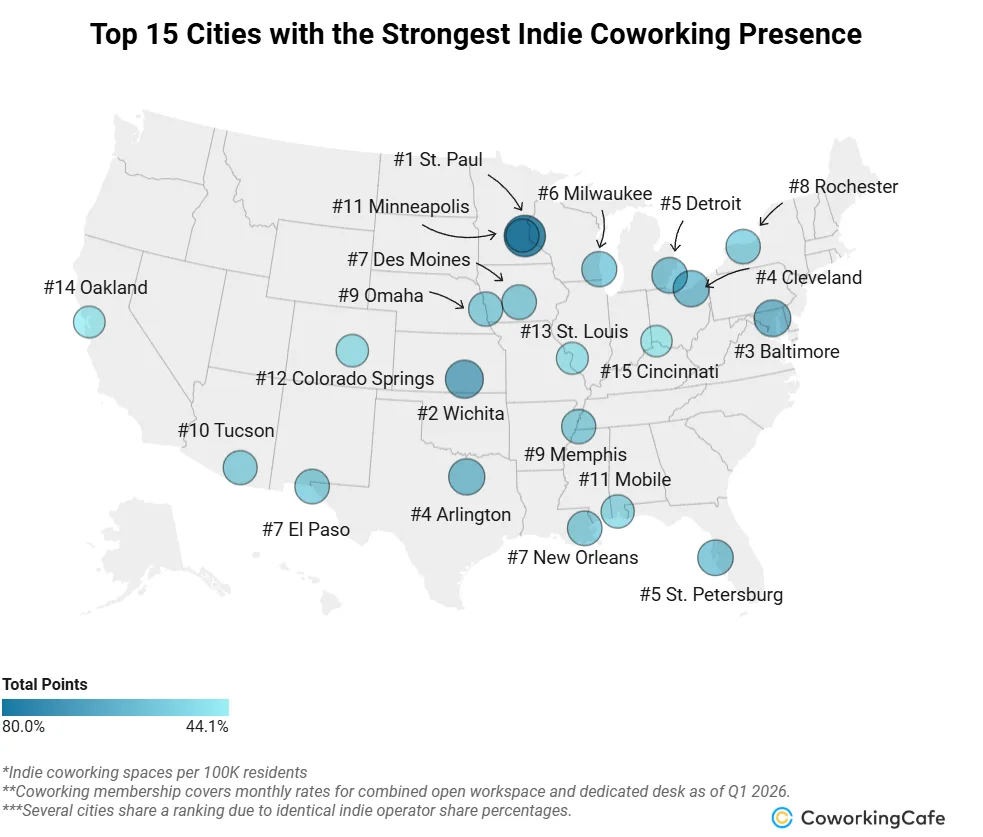

- St. Paul and Wichita tied for first among US cities for independent coworking presence, with independent operators accounting for 80% of each market.

- Midwest markets claimed eight of the top 15 cities, benefiting from startup growth, affordability, and rising remote work adoption.

- Smaller and midsized cities are becoming fertile ground for indie coworking brands as workers prioritize local identity and flexible workspace options.

Coworking’s next growth story isn’t coming from the largest national brands. Instead, smaller independent operators are gaining traction across midsized US cities, particularly in the Midwest, where remote work adoption, startup formation, and lower operating costs are creating favorable conditions for locally owned flex space providers.

A new study from CoworkingCafe analyzed 73 US cities with populations above 200,000 and found that independent coworking companies—defined as operators with fewer than four locations in a single city—are carving out significant market share in places where workers increasingly favor neighborhood-oriented workspace options over standardized national chains.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Midwest Takes Center Stage

Eight of the top 15 cities for indie coworking presence were located in the Midwest, led by St. Paul, Minnesota. According to CoworkingCafe’s 2026 analysis, 80% of St. Paul’s coworking operators are locally owned, with eight independent providers serving the market. The city also recorded 2.6 indie coworking spaces per 100,000 residents.

The broader Midwest trend reflects more than just coworking demand. Cities like Milwaukee, Cleveland, Detroit, and Omaha are seeing growth in tech startups, freelance work, and hybrid employment models that support flexible office use without requiring long-term leases.

Wichita, Kansas, tied for first nationally alongside St. Paul, with independent operators accounting for 80% of the local coworking market. Jacksonville came in third, with independent operators accounting for 75% of the local coworking market.

The Details

The report tied indie coworking growth directly to shifts in workforce behavior. In roughly 75% of analyzed cities, remote work participation exceeded the national average of 13.3%, creating a deeper customer base for flex office providers.

Several top-ranked cities also reported elevated self-employment levels. New Orleans posted the highest self-employment rate among leading markets at 7.1%, reflecting strong demand from freelancers and small business owners.

Pricing remains another competitive advantage for secondary markets. Monthly coworking memberships averaged $164 in Wichita, $182 in St. Paul, $199 in Cleveland and Des Moines, $205 in New Orleans, and $235 in Baltimore.

The study also highlighted how many independent operators intentionally position themselves around neighborhood identity and specialized communities. In New Orleans, for example, operators cater to niche audiences ranging from women executives to nonprofit organizations and creative professionals.

Smaller Markets, Stronger Local Brands

The findings reinforce a broader trend within commercial real estate: Secondary and tertiary markets are increasingly driving flex space innovation.

Nine of the top 15 cities identified in the report had populations below 500,000. Unlike gateway metros such as New York, Los Angeles, or Chicago—where large coworking brands dominate inventory—smaller cities still offer room for local operators to establish footholds before institutional consolidation takes hold.

Western representation was more limited than other regions, but Tucson, Las Vegas, and Colorado Springs all made the top 15. Tucson ranked particularly well, with independent operators accounting for roughly 73% of the local coworking market.

The South also posted a strong showing, placing five cities in the top 15, led by Jacksonville, Memphis, and New Orleans.

Why It Matters

The rise of indie coworking signals a shift in flexible office demand outside gateway markets. Instead of competing on scale alone, local operators now differentiate through affordability and neighborhood ties. That trend mirrors broader flex office expansion across major US markets, where coworking operators continue increasing their office footprint despite slower leasing activity.

That matters for landlords and investors evaluating office repositioning opportunities. As hybrid work stabilizes rather than disappears, smaller coworking operators could become increasingly important tenants for underutilized office assets in secondary downtowns and mixed-use districts.

The trend also suggests that flex office demand is becoming more decentralized. Workers are prioritizing proximity, convenience, and localized experiences over commuting into centralized corporate hubs.

According to CoworkingCafe, indie coworking growth tends to flourish in cities “large enough to sustain demand but not yet saturated by national brands,” creating opportunities for local entrepreneurs and smaller operators to establish durable market positions.

What’s Next

Independent coworking operators will likely stay concentrated in secondary markets with lower rents and fewer barriers. However, larger flex office firms may target successful regional brands as those companies mature.

Institutional investors could also pursue partnerships, acquisitions, or management agreements with established indie operators. As a result, competition may increase across high-growth secondary markets.

At the same time, hybrid work, freelancing, and startup growth should support long-term demand for flexible office space. Markets with growing tech sectors and strong remote-work adoption could lead the next expansion wave.

Midwest and Sun Belt cities appear especially well positioned for future indie coworking growth. These markets continue attracting startups, remote workers, and small businesses seeking flexible workspace options.

Office landlords also face pressure from elevated vacancies across many downtown markets. In response, locally rooted coworking operators may help landlords activate underused office space.

These operators also align with shifting workplace preferences centered on flexibility, convenience, and community-driven experiences.

Editor’s Note (June 2026): This article has been updated to reflect revised data provided by CoworkingCafe after the original report was corrected and republished. Several city rankings changed following updates to the underlying coworking operator dataset.