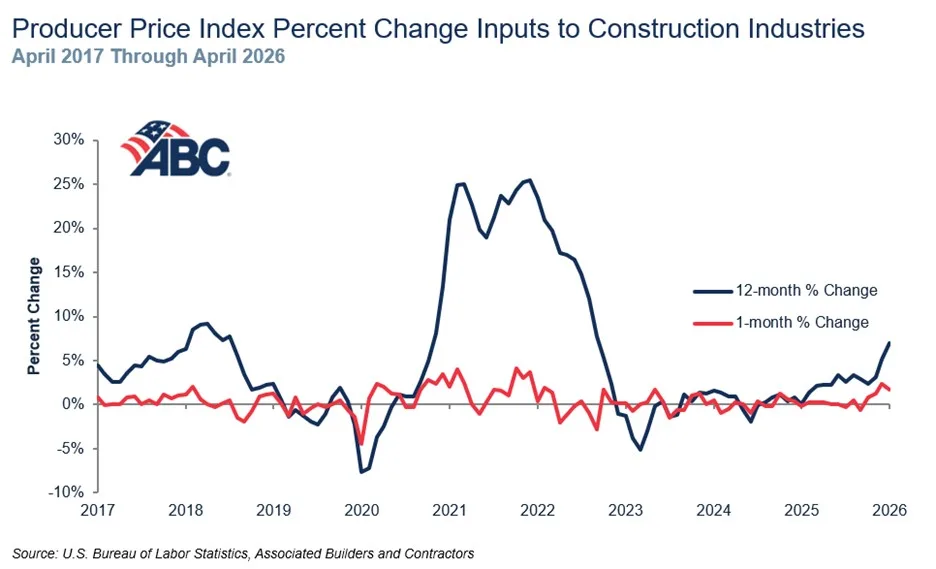

- Construction input prices increased 6.2% between January and April 2026, according to Associated Builders and Contractors analysis of BLS data.

- Energy commodities posted the sharpest gains in April, while steel and lumber prices also climbed as tariffs and inflation pressured supply chains.

- Rising material costs and stubborn inflation could delay expected Federal Reserve rate cuts, adding another headwind for commercial construction activity.

Bisnow reports that construction material costs continued climbing in April, extending a sharp escalation that contractors and developers have tracked since the start of 2026. Associated Builders and Contractors reported Wednesday that construction input prices rose 1.7% month over month and 6.2% year to date, based on US Bureau of Labor Statistics Producer Price Index data.

The pace of escalation has accelerated quickly. ABC Chief Economist Anirban Basu noted that construction input prices increased more during the first four months of 2026 than they did during the prior three years combined, when prices rose 4.8%.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Energy Prices Drive Construction Inflation

Energy commodities accounted for much of April’s increase, reflecting broader geopolitical and inflationary pressures. Crude petroleum prices jumped 11.3% between March and April, the steepest increase among tracked commodities. Unprocessed energy materials climbed 9.2%, while natural gas prices rose 4.9%.

Year over year, the increases were even steeper. Crude petroleum prices surged 61.8% compared to April 2025, according to ABC’s analysis, while natural gas prices rose 27.3% and unprocessed energy materials increased 48.9%.

The conflict involving Iran, combined with broader inflationary pressures, has contributed to higher fuel and transportation costs that ripple across construction supply chains.

The Details

Beyond energy, several core construction materials also posted meaningful gains in April. Softwood lumber prices rose 5.5% month over month, while hot rolled steel bars increased 4.1%. Steel mill products and industrial controls equipment each climbed 3.8%.

Overall construction materials prices were 7% higher than a year ago, while nonresidential construction input costs rose 7.4% annually. Nonresidential prices also increased 1.8% between March and April.

ABC attributed part of the increase to tariff-sensitive materials, particularly steel and iron products. Basu said inflationary pressure was “widespread” across the construction economy, not isolated to energy inputs alone.

Inflation Pressures Persist

The construction pricing surge comes as broader inflation data continues surprising economists. Wholesale inflation rose 1.4% in April compared to March, according to reporting from The Wall Street Journal, nearly triple economists’ expectations of a 0.5% increase.

That combination of elevated materials pricing and resilient labor market conditions could complicate expectations for lower borrowing costs later this year. Markets had anticipated potential Federal Reserve rate cuts in 2026, but persistent inflation data may keep policymakers cautious.

For commercial real estate projects, that creates a difficult equation: financing costs remain elevated while hard construction costs continue moving higher.

Why It Matters

Material cost inflation directly impacts project feasibility, especially for large-scale industrial, multifamily, and infrastructure developments already facing tighter lending conditions. Escalating steel, lumber, and fuel costs can quickly alter underwriting assumptions and squeeze contractor margins.

According to ABC’s Construction Backlog Indicator, contractors remain busy despite pricing volatility, with data center projects continuing to support demand for specialty contractors and large-scale construction activity nationwide. But sustained input cost increases could eventually slow starts, delay bids, or force developers to revisit project scopes.

The renewed rise in commodity pricing also revives concerns from the post-pandemic construction cycle, when rapid materials inflation disrupted budgets and timelines across the industry.

What’s Next

Developers and contractors will be watching energy markets closely through the summer as geopolitical tensions and tariff policies continue influencing commodity prices. Additional increases in oil and steel costs could place even more upward pressure on construction budgets heading into the second half of 2026.

Attention will also shift toward upcoming inflation and labor market reports as the industry gauges whether the Federal Reserve can realistically ease rates this year. If borrowing costs remain elevated alongside rising materials prices, project pipelines could begin softening later in 2026 despite today’s still-healthy backlog levels.