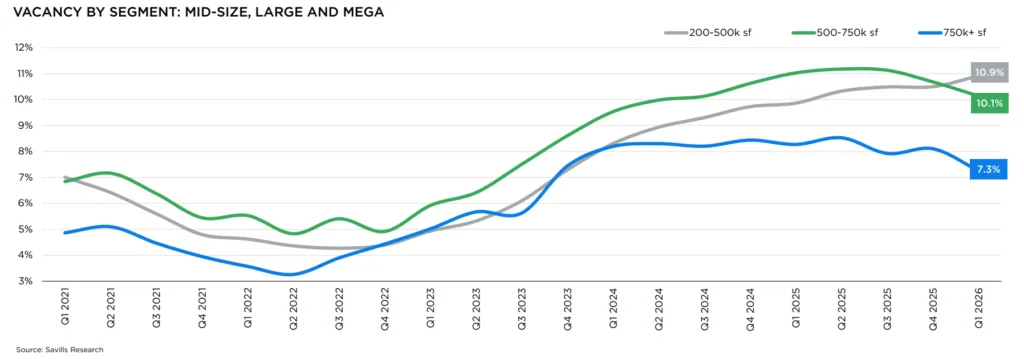

- Mega warehouse vacancies fell to 7.3% in Q1 2026, while mid-size vacancies climbed to 10.9%, per Savills and CompStak.

- Leasing momentum and rent escalation are concentrated in larger segments, with landlords capturing outsized value on mega deals.

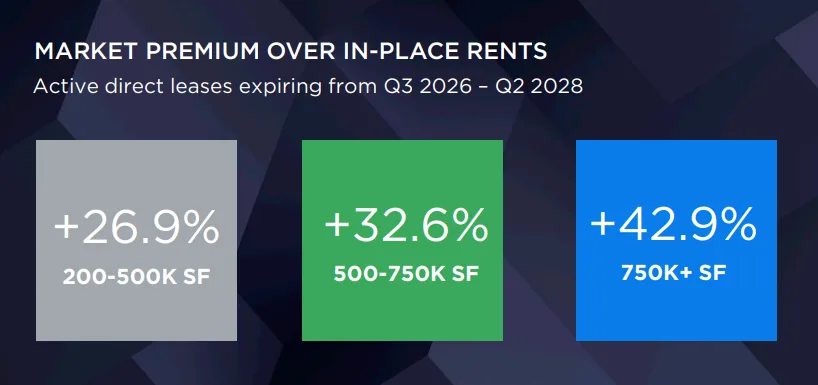

- Rent growth is poised to accelerate for mega facilities as expiring leases reveal market rents up to 42.9% higher than current in-place deals.

Mega Warehouses Buck the Industrial Supply Trend

According to a joint report by Savills and CompStak, the US industrial market’s bright spot is large-format warehouses, but the performance gap between mega and mid-size buildings is widening. In Q1 2026, vacancy for warehouses over 750,000 SF dropped to 7.3%, down 100 basis points year over year. Meanwhile, mid-size buildings (200,000–500,000 SF) reached a vacancy rate of 10.9%, and the trend remains negative. This divergence follows a pronounced shift in occupier strategy—larger facilities are attracting more tenants chasing supply chain resilience, while smaller ones face a glut.

Leasing data for the past six months shows mega facilities accounted for 30.6% of all big-box activity, rising sharply from 21.5% only six months earlier. The footprint of demand has shifted as logistics and retail operators look to consolidate operations into fewer, larger nodes, reflecting both new supply chain normal and competitive pressures on speed and costs. Population growth across several Sun Belt markets is reinforcing this trend, as expanding consumer bases require larger distribution networks and fulfillment hubs.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Barriers to Mega Development Keep Supply Tight

The mega warehouse segment is tightening for reasons beyond demand. Zoning rules, site constraints, and local opposition limit new supply. These challenges hit high-barrier markets hardest. In California, AB-98 creates additional hurdles for projects above 250,000 SF.

Savills found that from 2023 to 2025, developers delivered eight mid-size buildings for every new mega facility. That imbalance has created scarcity across major logistics markets. Dallas-Fort Worth offers more than 130 mid-size options but fewer than 10 mega listings. Similar supply gaps exist across many US logistics hubs. Over the past two years, available mega spaces fell 14%. Meanwhile, mid-size availability increased 15%. As a result, tenants face fewer choices in the largest warehouse segment.

Lease Economics Favor the Biggest Spaces

Savills and CompStak found clear differences in lease economics by building size. Mega leases signed between Q2 2025 and Q1 2026 averaged $8.45 PSF in starting rent. That trailed mid-size and large facilities. However, effective rents exceeded starting rents by 8.2%. Lower concessions and lease terms exceeding eight years drove the gap.

Meanwhile, mid-size leases averaged $9.62 PSF in starting rent. Yet they generated only a 1.3% effective rent premium. Concessions also remained high, reaching 9% of lease value. As a result, landlords increasingly prioritize lease duration and rent escalations over headline rents. This strategy helps them secure long-term value from mega facilities and lock in stronger cash flows.

Source: Savills Research and CompStak, The Bigger the Better Report, Q1 2026.

Lease Rollover Will Accelerate Mega Rent Growth

What sets the stage for rent acceleration in the mega segment is the large gap between in-place and market rents. CompStak’s analysis of leases expiring from Q3 2026 to Q2 2028 shows mega warehouse tenants will face average increases of 42.9% at renewal—compared with 32.6% for large and 26.9% for mid-size. Many of these expiring mega leases were signed before 2020, locking in pre-surge rates. As these roll, landlords will be able to mark rents to current and rising market levels, reinforcing the outperformance of the segment. The mid-size tier, by contrast, is still battling elevated supply, and landlords will need to keep offering concessions to secure tenants.

Collectively, these trends mean there is no one-size-fits-all recovery for industrial real estate. For investors, operators, and users, understanding the nuances between mega, large, and mid-size segments has never been more critical.

What’s Next

With supply chain dynamics still evolving, logistics and retail giants are likely to continue consolidating their footprints into mega facilities, further tightening an already limited pool. New supply remains uncertain, given higher barriers to construction in key US logistics nodes. Expect escalating rent growth in the mega segment as more pre-pandemic leases expire and rollover to market—Savills projects the largest mark-to-market jumps to hit from 2026 through 2028. Meanwhile, the mid-size segment is set for continued softness until supply overhangs resolve. Investors and developers should anticipate a bifurcated market landscape in the years ahead.