- Manufacturing PMI climbed to its highest level since May 2022, signaling stronger output and improving demand expectations across the sector.

- Capacity utilization remains below historical norms, while capital spending plans and industrial absorption suggest firms are relying on existing facilities rather than expanding.

- Rising input costs are flowing through supply chains, creating new cost pressures for industrial occupiers, developers, and property owners.

According to Trepp, US factory activity gained momentum in May as output increased, forward-looking demand indicators strengthened, and manufacturers showed greater confidence about the months ahead.

The improving outlook comes at a notable point for industrial real estate. While production is rising and leasing activity has recovered, several indicators suggest manufacturers still have enough existing capacity to accommodate growth without triggering a broad wave of new industrial development.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Demand Improves but Expansion Remains Cautious

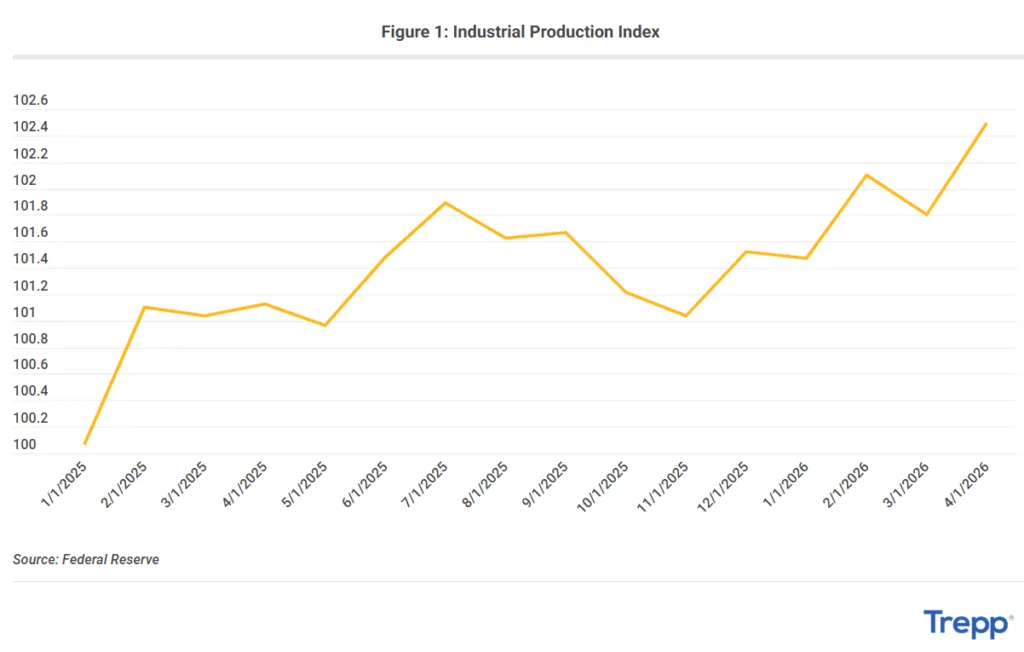

Manufacturing entered the second quarter with stronger momentum than many expected. The Federal Reserve’s April industrial production data showed manufacturing output rebounding after a March decline, supported by gains in durable goods production, business equipment, consumer goods, and motor vehicle manufacturing.

The May S&P Global Flash Manufacturing PMI reinforced that trend. The index reached its highest reading since May 2022, while manufacturing output expanded at its fastest pace in more than four years.

However, some of that activity appears tied to inventory building rather than end-user demand. Manufacturers reported stockpiling goods amid ongoing supply concerns and expectations for higher costs. While that behavior supports near-term production volumes, it does not necessarily indicate sustained long-term growth. For industrial landlords and developers, the distinction matters because temporary inventory accumulation often boosts warehouse utilization without creating permanent space requirements.

The Details

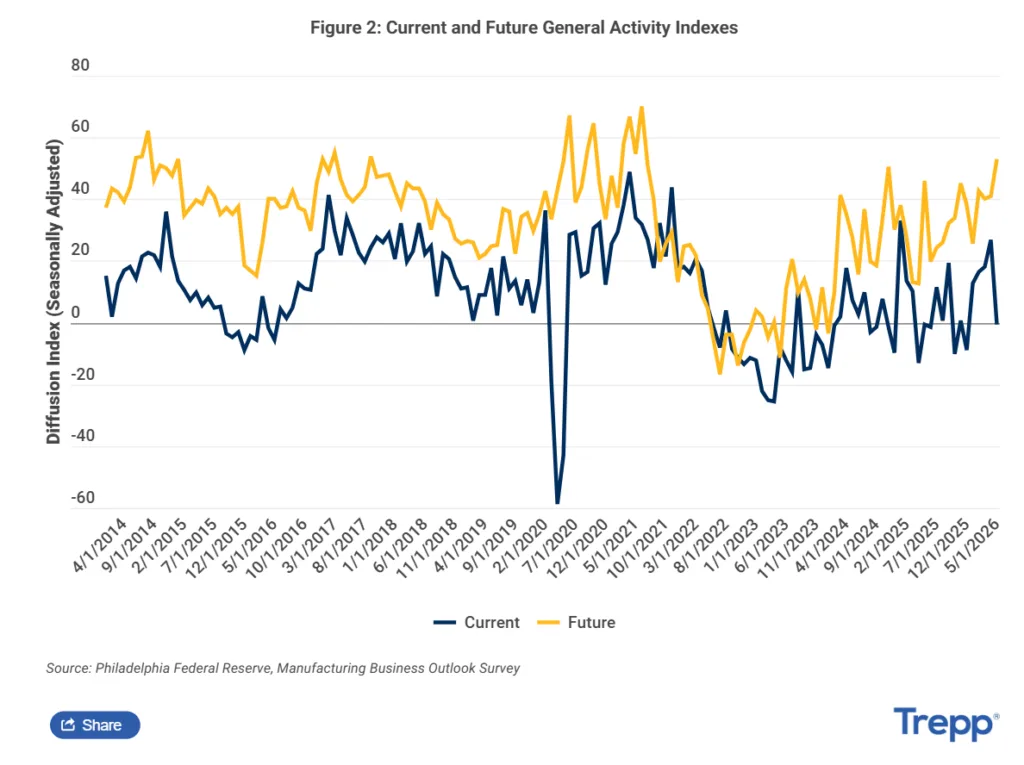

Regional Federal Reserve surveys painted a mixed picture of current manufacturing conditions but a much more consistent outlook for future demand.

The New York Fed’s Empire State Manufacturing Survey showed business conditions reaching their strongest level since April 2022. Meanwhile, the Philadelphia Fed’s current activity index declined after four consecutive months of improvement.

Despite those differences, manufacturers in both regions expressed growing confidence about the next six months. More than half of respondents in New York expect business conditions to improve, while nearly two-thirds of Philadelphia manufacturers anticipate increased activity. The Philadelphia Fed’s future activity index climbed to its highest level since June 2021.

That gap between current conditions and future expectations highlights an important dynamic. Manufacturers appear optimistic about future demand, but many have yet to translate that confidence into significant investment or expansion decisions.

Industrial Capacity Still Has Room to Run

The stronger demand outlook has not yet translated into meaningful capacity expansion. Federal Reserve data showed capacity utilization improving in April, but the metric remains below its long-run average.

Regional surveys point to similar caution. New York manufacturers reported only modest capital spending plans, while Philadelphia’s future capital expenditures index declined, though it remained in positive territory.

Industrial real estate fundamentals tell a comparable story. According to CBRE Econometric Advisors’ Q1 2026 industrial market report, leasing activity increased year over year and net absorption rebounded from early 2025 levels. Yet absorption remained below historical averages, while construction completions continued to exceed demand growth.

As a result, vacancy and availability rates remain elevated compared with a year ago. The combination suggests industrial demand is improving, but supply conditions remain loose enough that many occupiers can expand within existing facilities before requiring significant new construction.

Why It Matters

For developers hoping for a new wave of manufacturing-driven construction, the data offer a more measured outlook. Manufacturers are producing more goods and expressing greater confidence about future demand, but they are largely doing so within their existing footprints. Below-average capacity utilization and restrained capital spending indicate many facilities still have room to absorb additional production.

That dynamic aligns with broader industrial market conditions. According to CBRE’s Q1 2026 data, supply growth continues to outpace absorption despite improving leasing activity. As long as occupiers have available space and manufacturers retain unused production capacity, demand is more likely to support existing buildings than large-scale development pipelines.

What’s Next

The next several quarters will reveal whether manufacturers’ optimism translates into sustained production growth and new investment.

Current indicators suggest demand is moving in the right direction. Manufacturing output is rising, forward-looking activity measures remain strong, and industrial leasing has improved from 2025 levels. However, excess capacity and cautious spending plans continue to limit the case for major expansion.

The key variable to watch is the relationship between demand and costs. If stronger activity persists and manufacturers begin exhausting existing capacity, capital spending and industrial space demand could accelerate. If rising input costs compress margins instead, expansion plans may remain restrained despite improving business conditions.

For industrial real estate, the near-term signal remains clear: stronger utilization of existing facilities appears more likely than a broad new development cycle.