- Low- and middle-income renters are seeing a growing share of their incomes go toward rent, while high-income renters face less pressure.

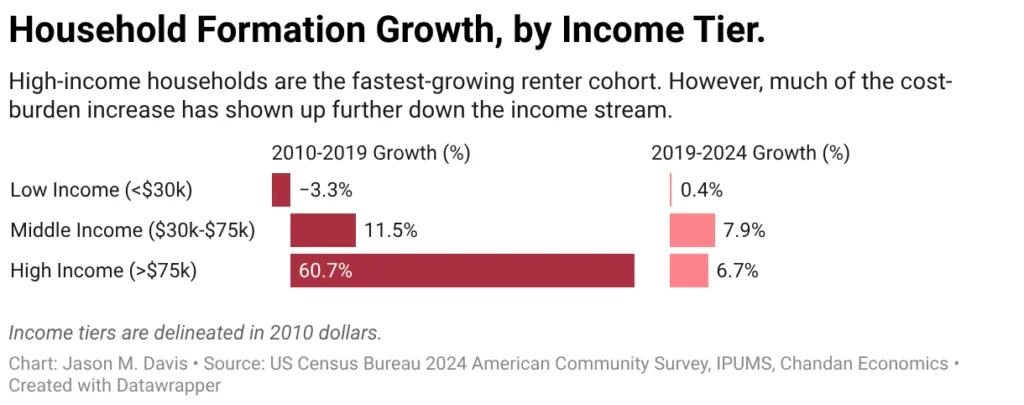

- The number of high-income renter households has expanded fastest since 2010, but affordability strains have hit lower incomes hardest as supply stays tight.

- A shrinking pool of low-rent units and robust demand have fueled stratification in the US rental market, widening the affordability gap.

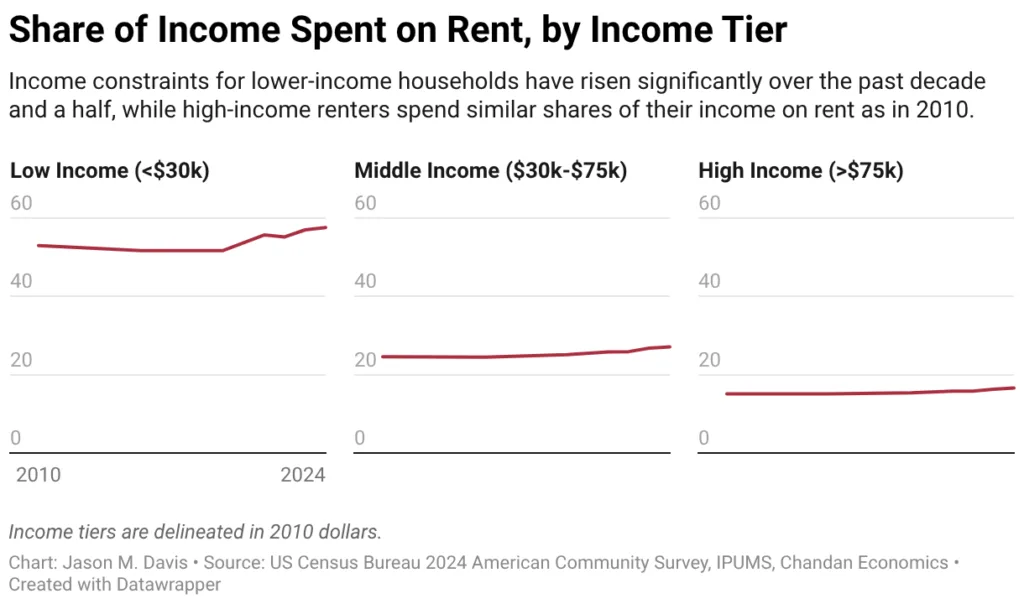

US rental affordability pressures have taken a sharply divergent path across income brackets. Barriers to homeownership have spurred a surge in high-income renter households since 2010, but the cost burden has grown fastest for low- and middle-income renters. In 2024, nearly 58% of low-income renters’ paychecks go to rent compared to roughly 53% in 2010. The affordability gap isn’t closing — it is widening.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Worsening Affordability Traps Lower-Income Households

Low- and middle-income households have shouldered the brunt of tightening affordability, while high earners have largely avoided significant cost increases. According to the latest data, just over 84% of low-income renters now spend more than 30% of their income on rent, a jump from 82.9% in 2010. The share of cost-burdened middle-income renters grew from 31.6% to 40.5% between 2010 and 2024.

High-Income Renters Reshape the Landscape

High-income renters have become the fastest-growing segment since the GFC, increasing 60.7% from 2010 to 2019. Despite greater demand from this cohort, high earners saw their rent-to-income ratio rise only modestly (from 15.1% in 2010 to 16.6% in 2024), signaling that upwards rental pressure was disproportionately absorbed by households lower on the income ladder.

Supply Constraints and the Filtering Effect

The trend coincides with a shrinking pool of affordable units. Harvard’s Joint Center for Housing Studies found the US lost 2.1M rentals with inflation-adjusted rents below $600 between 2012 and 2022 — units critical to those earning under $30,000 per year. While high-end apartment construction has ramped up post-pandemic, most new supply is priced above traditional affordable thresholds. The filtering down of older, more affordable inventory is lagging behind the influx of higher-earning renters, compounding cost pressures at the bottom.

Why It Matters

The findings challenge the assumption that rising demand from lower-income households alone drives affordability pressures. Instead, the data suggests supply constraints have played a major role in determining who bears the cost of higher rents.

Despite substantial growth in higher-income renter demand, lower- and middle-income households experienced the sharpest increases in housing stress. The share of middle-income renters spending at least 30% of income on rent rose from 31.6% in 2010 to 40.5% in 2024, highlighting how affordability pressures spread through the market.

The shortage of affordable housing appears central to that story. According to a 2024 report from Harvard University’s Joint Center for Housing Studies, the US lost 2.1M rental units with inflation-adjusted rents below $600 between 2012 and 2022. Those units historically served households at the lower end of the income spectrum.

What’s Next

The rental market has seen a surge in apartment construction since the pandemic, but much of that new supply has targeted higher price points and amenity-rich projects.

Over time, newly delivered apartments can create a filtering effect as older units become relatively more affordable. However, Davis argues that new renter demand is moving through the system faster than affordable inventory is being created.

Unless the pace of affordable housing production accelerates, affordability pressures may remain concentrated among lower- and middle-income renters. That could leave the rental market increasingly segmented, with higher-income households continuing to drive demand while cost burdens deepen for renters further down the income distribution.

For owners, developers, and policymakers, the data underscores a growing challenge: increasing supply alone may not be enough if new inventory fails to reach the households experiencing the greatest affordability strain.