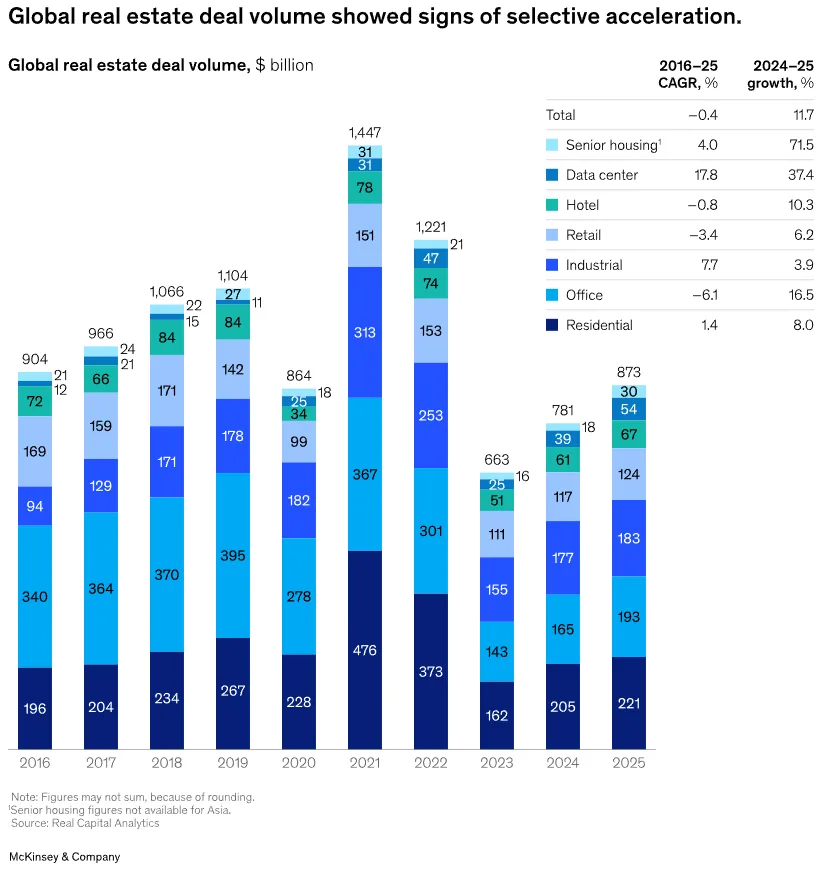

- Global real estate deal value climbed 12% in 2025, but total transaction count stayed flat as investors targeted select sectors and higher quality assets.

- Specialty property, including data centers and senior housing, now comprises 14% of total volume, while AI is rapidly transforming operations and workflows industry-wide.

- Operational execution, capital structure creativity, and platform scale have replaced cycle-driven momentum, reshaping strategies for both GPs and LPs.

Selective Acceleration Defines 2025

Global real estate capital deployed in 2025 signaled a shift in strategy: deal value hit $873B, up 12% year over year, but transaction count remained broadly flat, reports McKinsey. The uptick reflects not broad market normalization, but concentrated bets in sectors like data centers, senior and student housing, and flex industrial. Data center deal volumes surged 37% globally, while US Class A office transactions rose 34%. Investors are sharpening focus on asset and operator quality as structural shifts—including hybrid work and obsolescence of lower-tier assets—intensify pressure on lagging segments.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Cycle Tailwinds Fade, Execution Takes Center Stage

Capital flows are recovering, but the easy alpha from falling cap rates is over. According to McKinsey, public REITs now trade at cap rates 130 bps above private appraisals, with the gap halved from 2023 as valuations adjust. Investors emphasize asset selection and operational value add: in 2025, asset selection explained 70% of performance variation, up from under 50% three years prior. The result is a market where strong underwriting, discipline on capital structure, and platform scale matter more than broad market exposure or cycle timing.

AI Reshapes Operating Models

AI is moving from back-office efficiency play to core strategy, catalyzing what McKinsey describes as agentic adoption: embedding AI into end-to-end workflows across maintenance, leasing, asset management, and construction. The estimated annual value from agentic AI across global real estate tops $430B. Platforms integrating AI directly—not just layering on tools—are speeding up decision-making, surfacing actionable insights, and cutting leakage, especially where human judgment interplays with automated processes. Large, vertically integrated owners and managers hold a structural advantage at scale.

Debt, Returns, and Fundraising Trends

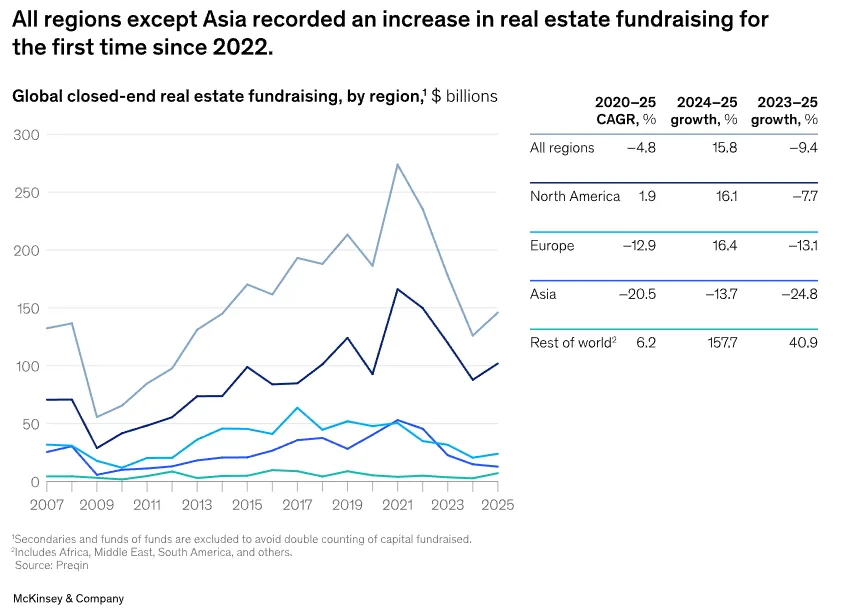

2025 saw a rebound in private-market fundraising to $146B, up 16%, but still roughly 50% below prepandemic highs. Opportunistic funds were up 65% as LPs searched for dislocation plays, while value-add strategies slumped to just $27B, down 71% from 2022.

Return profiles improved, with debt and core-plus strategies leading (4.8% and 1.5% annual returns), but performance is still well below the 2021 peak. Refinancing pressure persists: $2.1T of US CRE loans are slated to mature over the next three years, with the ‘wall of maturities’ simply pushed forward by extensions and restructurings.

Vertical Integration and Market Consolidation

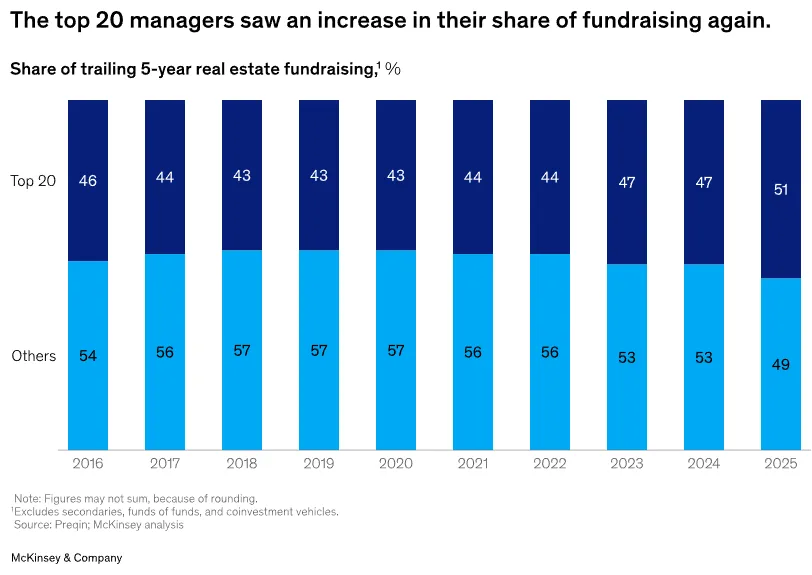

Larger real estate platforms are actively acquiring operating capabilities, blurring the lines between investment management and day-to-day execution. Mega deals—like Apollo’s acquisition of Bridge Investment Group and Brookfield’s pending purchase of Peakstone Realty Trust—underline a bet on platform scale for capital deployment and integration of asset management. For LPs, the top 20 managers captured 51% of fundraising in 2025, up from 46% a decade ago, as institutional investors cut relationships with smaller GPs in favor of larger, diversified operators. Minority GP stake sales now account for 57% of real estate manager M&A, according to McKinsey data.

Real Estate, Infrastructure, and the Blurring Boundary

Data centers, logistics, and life sciences assets are drawing both real estate and infrastructure capital, with hybrid players (KKR, Blackstone, Stonepeak) creating ‘real asset’ platforms. Institutional investors are also increasing allocations to specialty sectors that offer stronger demographic and operational tailwinds. Infrastructure funds—which delivered 5% IRR for bottom-quartile vintages between 2013–22, compared to losses in real estate—now target real estate-like segments, intensifying competition. Infrastructure’s portfolio share rose from 32% in 2023 to 36% in 2025. The implication: future outperformance hinges on subasset-level execution and capital flexibility, regardless of traditional segment labels.

Why It Matters

These shifts underscore a new reality: the CRE cycle is not ‘returning to normal.’ Instead, capital is more concentrated, operational execution separates winners from laggards, and large-scale platforms hold structural advantages. For dealmakers and operators, evidence-backed niche strategies matter more than market beta. For institutional capital, scale and execution quality increasingly define partner selection. AI, capital structure agility, and integrated workflows are emerging as necessary—not optional—for value creation in the new cycle.

What’s Next

Look for continued market bifurcation and further LP consolidation around the biggest platforms, especially those with in-house operational capabilities. Data center, senior housing, and Class A office segments should remain hotbeds for deal activity in 2026, powered by both real estate and infrastructure capital. AI adoption will move from pilot to enterprise scale, raising both execution stakes and competitive barriers. CRE professionals should expect a market where outperformance requires clear specialization, capital and operating agility, and strong technology integration at the asset level.