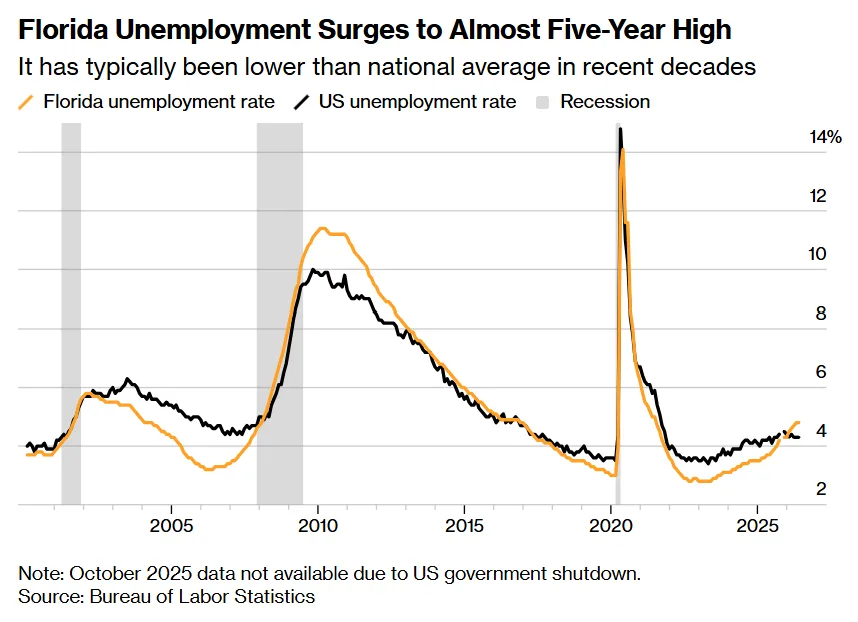

- Florida’s unemployment rate jumped to 4.8% as of May 2026, the highest in nearly five years, according to the Bureau of Labor Statistics.

- Key sectors like real estate, retail, and tourism are losing jobs as affordability issues and immigration enforcement weigh on demand.

- The state’s rapid post-pandemic growth has slowed sharply, raising questions about Florida’s economic model as domestic migration falters.

Florida’s Economic Cycle Turns

Florida has seen a dramatic swing in its job market fortunes since its pandemic-era population and economic boom, per Bloomberg. While the state once led the US in job creation, soaring living costs and cooling demand in major sectors are now taking a toll. The current surge in unemployment comes as high-profile companies like Citadel and Palantir relocate to the Sunshine State, yet these headlines mask a deeper slowdown in traditional engines of growth. Job seekers, including transplants lured by Florida’s zero state income tax and sunny climate, are discovering opportunities much tighter on the ground than in years past.

This reversal highlights Florida’s exposure to cyclical trends. The state’s economy is more sensitive to swings in consumer sentiment and interest rates, making it vulnerable as wage growth lags behind the rising cost of living. After nearly a million jobs were added since 2019, this sudden cooling is catching policymakers and newcomers off guard.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

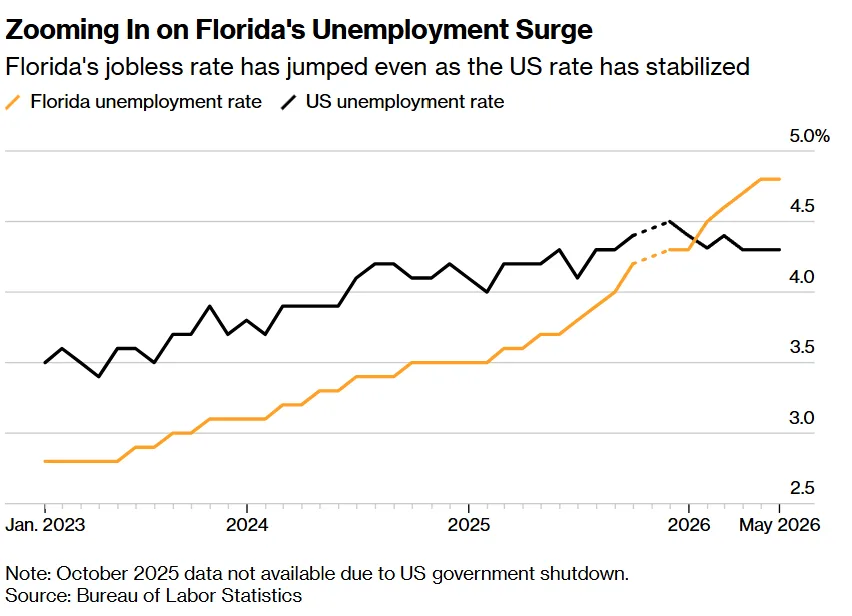

Florida’s unemployment rate climbed more than a full percentage point to 4.8% by May 2026, significantly outpacing the US average, per Bureau of Labor Statistics data. This rise marks one of the steepest state-level increases in the country over the past year. The slowdown has been led by contractions in heavily consumer-exposed industries: employment at furniture stores fell 3.7%, real estate jobs dropped 3.1%, and accommodations headcount shrank 3%, all as of May.

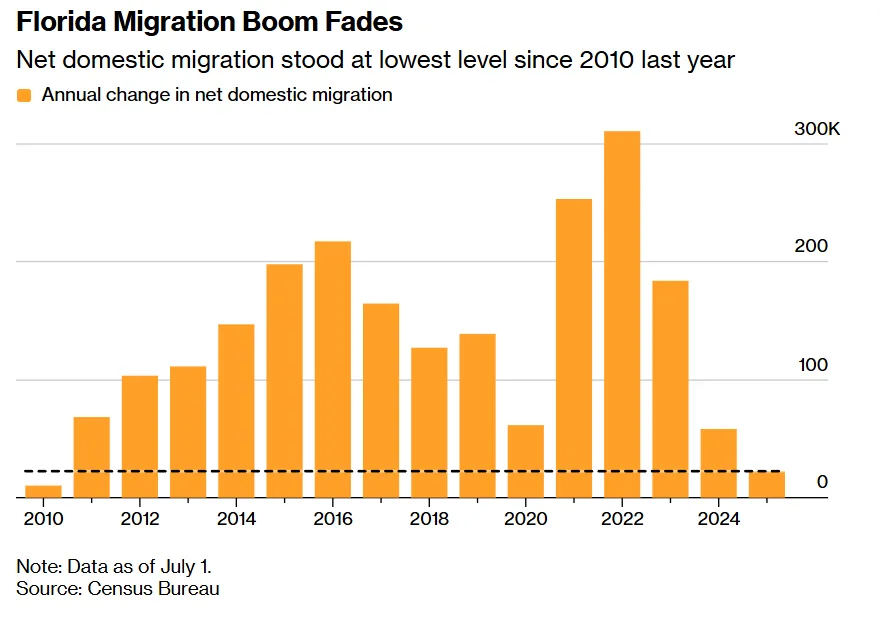

Domestic migration—a key driver of Florida’s past success—plummeted to just 22,517 people in the year through July 2025, per the Census Bureau, down from several hundred thousand at the pandemic peak. Meanwhile, the state’s tourism bureau, Visit Florida, reported a 1% drop in visitors for Q1 2026 compared to the previous year.

Florida Faces a Reversal in Migration and Growth

The latest numbers reflect a sharp pivot from Florida’s high-flying growth narrative post-2020, when it was second only to Texas in net new job creation. Affordability has now become a choke point: wage growth has failed to keep up with housing and insurance premiums, which soared following the state’s population surge. Net migration, which exceeded 200,000 annually during the peak, has returned to levels not seen since 2010.

The result is a state no longer leading in population and job growth, but instead seeing warning signs typically reserved for more mature Sun Belt markets. The weaker labor market is also reducing household formation, easing rental demand in several Florida metros. Compounding this, stricter immigration enforcement has reduced both the labor pool and the consumer base in local economies, particularly in immigrant-driven hubs like Miami.

Why It Matters

The shift in Florida’s job market has broad implications for CRE professionals and economic developers alike. For years, Florida has been a go-to Sun Belt story, drawing corporate expansions, inbound migration, and investor dollars on the promise of continuous growth. The state’s unemployment surge calls that thesis into question, especially as its core industries—hospitality, retail, and real estate—face secular headwinds and stiffer competition for domestic relocation. Property owners in hospitality and consumer-driven retail are feeling the impact as job losses in those sectors squeeze household budgets and reduce discretionary spending. According to BLS May 2026 data, payrolls in the state grew just 0.1% year-over-year, compared to a 0.3% gain nationally. Meanwhile, migration data from the Census Bureau signals fewer out-of-state arrivals to prop up housing demand and retail foot traffic.

While marquee office relocations like Citadel and Palantir provide political cover and some localized outperformance (e.g., Downtown Miami, which is still attracting global capital), the benefits have yet to broaden meaningfully statewide. Several Sun Belt metros face similar issues, but the speed of Florida’s reversal is sending a signal: labor market risks are rising just as the state’s cost advantages are diminishing. As political leaders debate responses—from tax incentives to business formation policies—market participants will be looking for evidence that Florida can diversify away from cyclical sectors or risk seeing the lure of business-friendly weather wear thin.

What’s Next

The coming months will put further pressure on Florida policymakers and business leaders to generate sustainable job opportunities outside of tourism and service industries. With elections looming—including the race to replace Governor Ron DeSantis and several open House seats—job growth and affordability are set to dominate the statewide conversation. Miami and the Space Coast may continue to draw growth sectors like finance and aerospace, but it will take years for these gains to affect the state’s overall economic profile, according to Homebase chief economist Guy Berger. For now, the market will be watching migration and job numbers closely for any sign the cycle is turning—because if Florida’s recent history is any guide, shifts can happen fast.