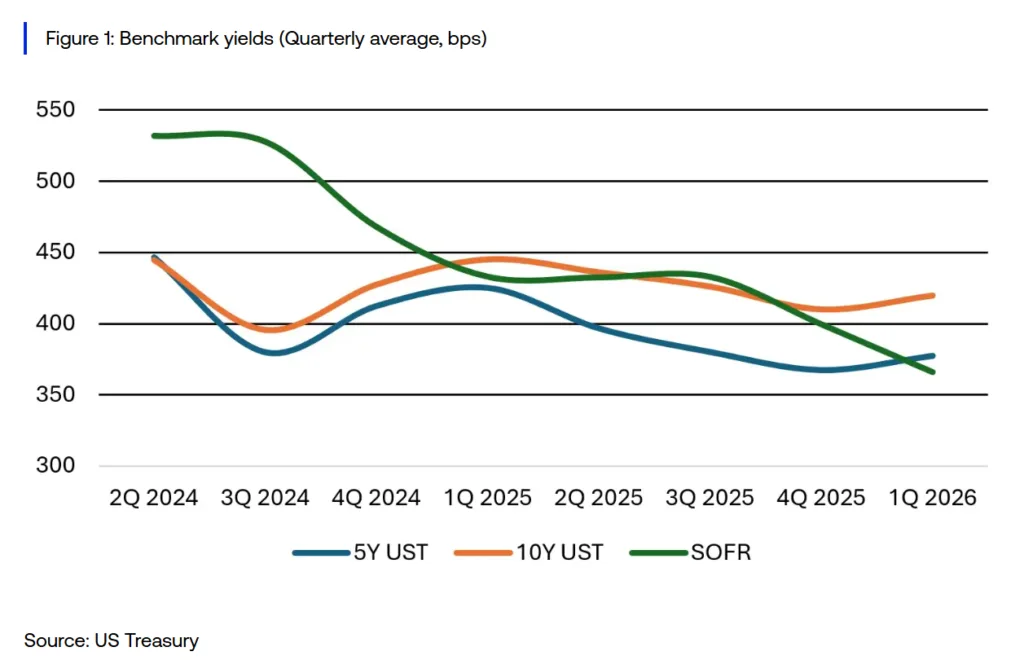

- CRE debt markets entered a more fragmented environment in Q1 2026, with falling SOFR lowering floating-rate borrowing costs while Treasury yields moved higher for fixed-rate loans.

- Altus Group reported a 24% quarterly rebound in quote activity to 1,866 quotes, with lenders remaining highly competitive across multifamily, industrial, and select office assets.

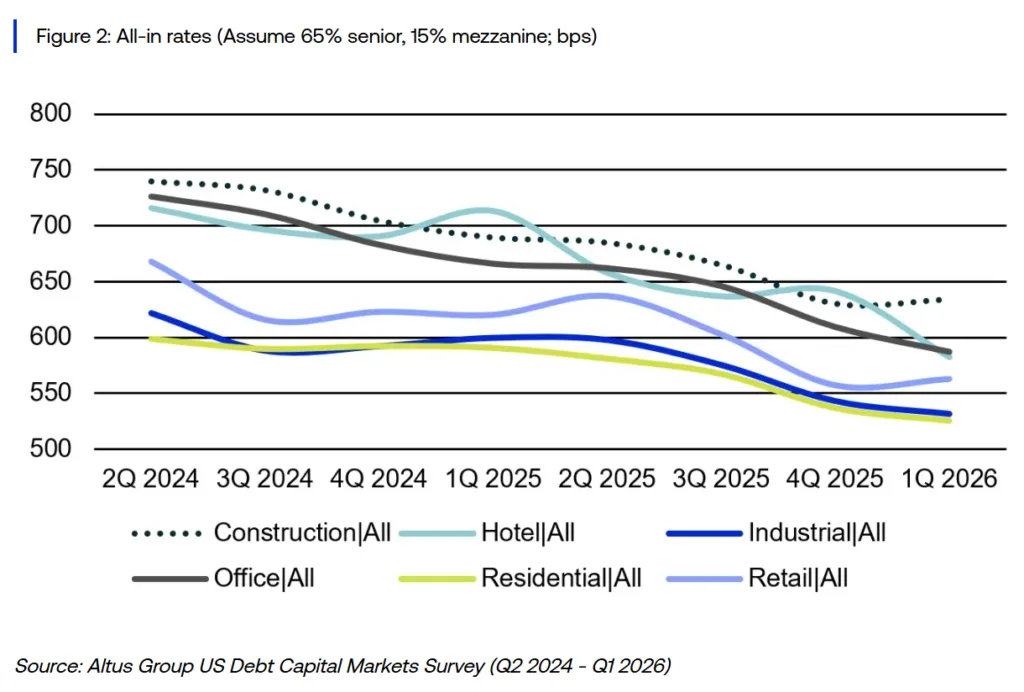

- Hospitality and office financing costs compressed sharply year over year, signaling improving lender sentiment toward sectors that faced elevated scrutiny over the past two years.

The CRE debt market lost its one-way momentum in Q1 2026. While floating-rate borrowers benefited from another sharp decline in SOFR, fixed-rate borrowers faced higher Treasury benchmarks that partially erased gains from tighter spreads. The result was a bifurcated lending environment where financing costs increasingly depended on loan structure rather than broad market conditions.

According to Altus Group’s Q1 2026 US Debt Capital Markets Survey, market activity rebounded after a slower holiday quarter, with lenders issuing 1,866 quotes across all products, up 24% quarter over quarter. Borrowers continued to receive roughly 5.1 competitive quotes per financing request, underscoring that lender appetite remains intact despite volatility in benchmark rates.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Market Driven by Diverging Benchmarks

SOFR averaged 3.66% in Q1 2026, down 34 basis points from Q4 2025 and 67 basis points year over year. That decline continued to lower borrowing costs for floating-rate debt, especially bridge and short-term financing products tied directly to the benchmark.

Treasury yields moved in the opposite direction. The 5-Year Treasury climbed 10 basis points quarter over quarter to 3.77%, while the 10-Year Treasury rose to 4.20%, also up 10 basis points, according to Altus Group. The increases marked the first quarterly reversal after several periods of declining fixed-rate benchmarks.

That divergence created a split market. Floating-rate borrowers captured immediate savings, while fixed-rate borrowers saw tighter spreads offset only part of the Treasury increase. The gap is becoming more consequential as borrowers weigh whether to lock rates or stay exposed to additional Fed easing later in 2026.

The Details

Floating-rate senior short-term loans remained the dominant financing product, accounting for 39% of all quotes in the quarter, or 720 transactions surveyed. Fixed-rate senior short-term debt followed at 21%, while fixed-rate senior long-term loans represented 19%.

Overall lender engagement strengthened. Survey participants averaged 17 quotes each during the quarter, the highest level since Q2 2025. Altus Group surveyed 110 market participants across lending platforms and debt intermediaries.

Multifamily remained the most financed collateral type at 23% of all quotes, followed by industrial at 18%. Office and retail each captured 17% of quote volume, suggesting lenders continue reopening selectively to office deals after several years of retrenchment.

Office’s stability stands out given the sector’s ongoing valuation pressure. Rather than avoiding office entirely, lenders appear increasingly willing to finance trophy and stabilized properties with durable tenancy and strong sponsorship.

Spread Compression Continues

Credit spreads tightened across most major loan categories in Q1. Lower-leverage floating-rate senior loans averaged spreads of 267 basis points over SOFR, while higher-leverage floating loans tightened to 348 basis points.

On the fixed-rate side, lower-leverage senior short-term loans averaged 218 basis points over the 5-Year Treasury, down 15% year over year. Fixed-rate mezzanine debt averaged 774 basis points over the 10-Year Treasury, while preferred equity coupons averaged 12.37%.

Hotel financing posted the most dramatic improvement. According to Altus Group, hotel all-in borrowing costs fell 59 basis points quarter over quarter to 5.82%. Limited-service hotels saw costs decline 150 basis points year over year, signaling that lenders have become materially more comfortable underwriting hospitality risk after years of post-pandemic caution.

Office financing costs also continued to improve. Average office all-in rates fell 79 basis points year over year to 5.87%, with trophy office assets seeing declines of roughly 100 basis points over the same period.

A Borrower-Friendly Market, for Now

The broader all-in borrowing picture still favors borrowers. Across all property sectors, average financing costs declined 68 basis points year over year, even though quarter-over-quarter improvements slowed materially compared to late 2025.

Residential and industrial properties remain the cheapest conventional sectors to finance, with all-in rates averaging 5.25% and 5.32%, respectively. That trend persists even as Sunbelt multifamily markets face rising supply pressure and slower rent growth. Construction loans, however, remain elevated. Construction office financing jumped 133 basis points quarter over quarter to 7.97%, reflecting continued lender caution around speculative office development.

Retail also showed some renewed pricing pressure, with all-in borrowing costs rising modestly to 5.63% during the quarter.

Why It Matters

The Q1 data shows a CRE financing market shifting toward asset-specific and structure-specific pricing. Falling short-term rates continue helping floating-rate borrowers refinance and extend loans. However, rising Treasury yields may limit relief for fixed-rate borrowers.

The shift also complicates capital stack decisions for owners and developers. Borrowers expecting additional Fed cuts may favor floating-rate loans. Meanwhile, borrowers worried about Treasury volatility may lock rates sooner.

Hotel and office pricing also improved meaningfully. Lenders pulled back sharply from both sectors between 2022 and 2024. Now, tighter spreads suggest institutional capital is returning selectively.

What’s Next

The next phase of the CRE lending cycle will likely hinge on whether Treasury yields continue climbing while SOFR declines further. If that split persists, the market could see a wider divide between bridge lending and permanent financing activity.

Lender competition remains healthy, but the easy repricing gains may be fading. Borrowers will be watching upcoming Fed decisions, inflation data, and Treasury market volatility closely as they evaluate refinancing strategies for the second half of 2026.