- CLO issuance surged in May 2026, marking the strongest US activity this year and second best month for Europe.

- AAA spreads tightened despite remaining above February lows, while refinancing and reset volumes hit multi-year highs.

- This resurgence reflects increased lender confidence amid lingering geopolitical uncertainty, with a positive outlook for year-end issuance.

CLO Market Bounces Back in May

Trepp reports that US and European collateralized loan obligation (CLO) markets regained momentum in May 2026 after a subdued March and volatile April. Both primary issuance and refinancing activity ramped up significantly, marking a notable improvement in credit market sentiment. Spreads on senior tranches tightened from April’s highs, signaling resilience in the face of ongoing geopolitical uncertainty. Managers and investors adjusted quickly to a slightly improved risk environment, pushing May’s volumes well above prior months.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

US and European CLO Issuance Surges After March Lull

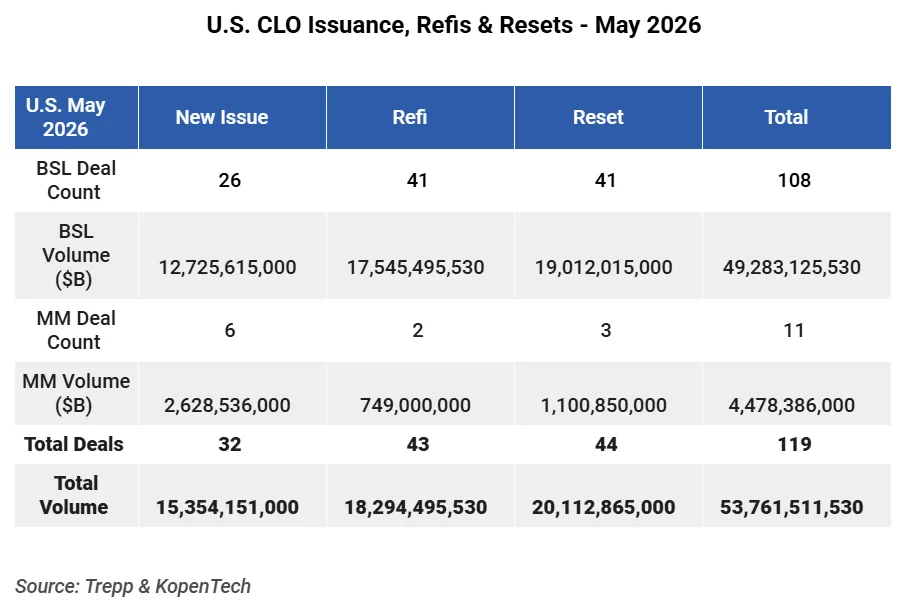

After March’s slowdown, May CLO issuance in the US reached $53.7B across 119 deals, according to Trepp and KopenTech. Broadly syndicated loan (BSL) CLOs drove US activity, with $49.2B from 108 deals, while middle market transactions contributed $4.5B across 11 deals. New issuance hit $15.3B, more than double April’s levels. Refi and reset activity accelerated to $38.4B across 87 deals—up nearly 94% month-over-month. In Europe, total May issuance reached €9.8B across 24 deals, up from earlier in the year, all concentrated in BSL structures. New issuance there jumped to €5.7B, while refinancings and resets modestly increased to €4.2B.

Spreads Narrow and Deal Terms Hold Stable

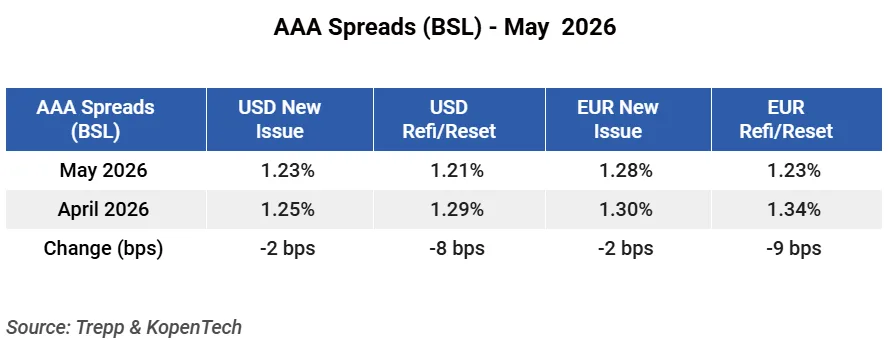

AAA spreads, a key measure of CLO risk appetite, narrowed in May. New US BSL deals priced at 1.23%, down two basis points from April. European new issue spreads also tightened, averaging 1.28%. Refi and reset spreads fell even further. US spreads tightened by eight basis points. European spreads narrowed by 11 basis points. Meanwhile, managers and investors maintained discipline. Reinvestment periods and non-call durations stayed largely unchanged. Only minor structural adjustments appeared across new deals.

Refi/Reset Boom as Managers Lock In Cheaper Funding

The sharp uptick in refi and reset activity in both regions underscores managers’ desire to seize more favorable funding conditions. US refi/reset issuance nearly doubled in May to $38.4B, a stark contrast to April’s $19.8B. European managers also grew more active, with €4.2B in refi/resets exceeding March’s €3.1B. The tightening of AAA and other tranches provided the window to refinance older, higher-cost deals, suggesting widespread belief in continued market stability for at least the near term.

Why It Matters

CLOs remain a vital conduit for leveraged finance liquidity. The May rebound highlights how quickly issuance and refinancing markets can reopen when risk premiums normalize. That improvement contrasts with recent stress in commercial real estate CLOs, where rising maturities have pressured loan performance and credit metrics. Even so, macro uncertainty persists. According to Trepp and KopenTech, the return of tighter spreads and heavier deal flow not only unlocks capital for lenders and issuers but helps reprice broader credit risk across the leveraged loan and private credit landscape.

What’s Next

With the CLO market displaying renewed flexibility and risk tolerance, syndicators and managers are likely to test the limits of demand heading into the second half of 2026. Watch for further tightening in spreads if risk sentiment continues to improve. The focus now turns to new manager entrants and evolving deal structures as the market absorbs any further geopolitical shocks. Europe’s continued stabilization and potential reactivation of the middle market segment could also add to volumes in the months ahead.