- US retail sales jumped 5.2% YoY in May 2026, marking the fastest annual rise in over a year, largely fueled by inflation in select categories.

- Foot traffic outperformed for value brands and experiences, while core retail volume growth slowed to near-stagnant levels at 0.2%.

- Discretionary and experiential spending held up despite tighter budgets, but broad caution is evident in food, home, and furniture categories.

Inflation Drives Retail Headline Highs

Retail sales performance appeared robust in May 2026, as US stores logged a 5.2% annual gain—the fastest pace seen in over a year, according to new data from Placer.ai and GlobalData shared by Colliers. Core retail (excluding food and fuel) grew 4.5% year-over-year, continuing a 2026 streak of strong nominal gains. But sector leaders and CRE professionals are parsing the headline numbers closely, since much of the growth owes to sky-high inflation—gas station sales alone surged 25.4%, masking considerably weaker underlying demand. Without gasoline, retail growth in May moderates to 3.7%, and most of that is price, not volume.

The report also highlights consumer behavior shifts, as shoppers continue to spend but increasingly trade down or cherry-pick experiences and selective discretionary goods. This dynamic is reshaping physical retail traffic patterns and overall CRE demand, with the market recalibrating expectations for the rest of 2026.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

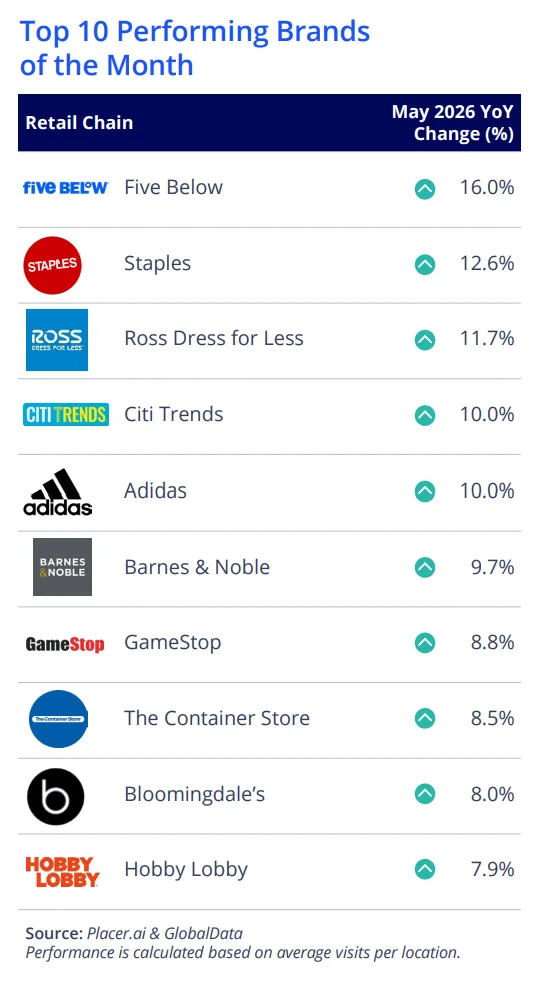

May’s lift in retail sales was uneven across channels. While top-performing retail brands like Five Below (up 16.0% in YoY foot traffic), Staples (12.6%), and Ross Dress for Less (11.7%) drew more shoppers, core retail volume growth dropped to just 0.2%—signaling consumer spending power is thin after adjusting for inflation. Discount and dollar store visits rose 7.79%, highlighting a pivot to value.

Experiential categories sustained strength: theater and music venues saw a 12.23% YoY visitor rise, and attractions were up 8.12%. Apparel sales climbed 3.6% and clothing visits grew 4.15%, reflecting continued indulgence in selective discretionary buys. Furniture (1.06% foot traffic growth) and home improvement retailers (0.56%) lagged, reaffirming caution around larger purchases. Grocery and food sales inched up 1.5%, but volume slipped 0.7% as consumers traded down.

Consumers Grow Selective as Value, Experiences Win Out

Patterns in the May 2026 data show consumers spending more carefully. Stubborn inflation continues to pressure household budgets. As a result, shoppers favor specific categories and cut back elsewhere. Discount retailers and affordable discretionary brands posted the strongest gains. Five Below, Ross, and Citi Trends led monthly traffic growth. Meanwhile, furniture stores, home improvement chains, and traditional grocers saw weaker results.

Food spending also reflected growing pressure. Visits to discount grocery stores jumped nearly 8%. However, grocery store traffic increased by less than 1%. At the same time, consumers continued spending on experiences. Fitness venues recorded a 2.47% traffic increase. Theaters and attractions posted double-digit gains. This selective spending pattern also reflects broader market caution, even as stronger headline indicators can hide underlying weakness across commercial real estate sectors.

Why It Matters

May’s data highlights a retail market operating in a high-price, low-growth environment. According to Placer.ai, shoppers increasingly favor value and experiences over broad discretionary spending. Meanwhile, core retail volume grew just 0.2% year over year, based on Colliers and GlobalData estimates. Most sales gains came from inflation rather than stronger demand.

Experience-focused tenants remain a bright spot for mixed-use and entertainment centers. Discount and off-price retailers also continue expanding. However, slower activity in furniture, home goods, and grocery stores limits broader retail recovery. Falling food sales volumes and uneven category performance point to ongoing consumer caution. CRE owners should track category-level demand and foot traffic instead of headline sales. These metrics offer a clearer view of tenant performance and leasing risk.

What’s Next

Inflation will likely continue masking retail weakness until prices stabilize or wages improve. Therefore, CRE investors will likely focus on value retailers, entertainment, and selective discretionary tenants. These categories continue attracting shoppers and supporting sales growth. Discounters, off-price apparel, and entertainment concepts should outperform through the rest of 2026. Monitoring category-level traffic and sales volume will remain essential as consumer spending patterns continue to shift.