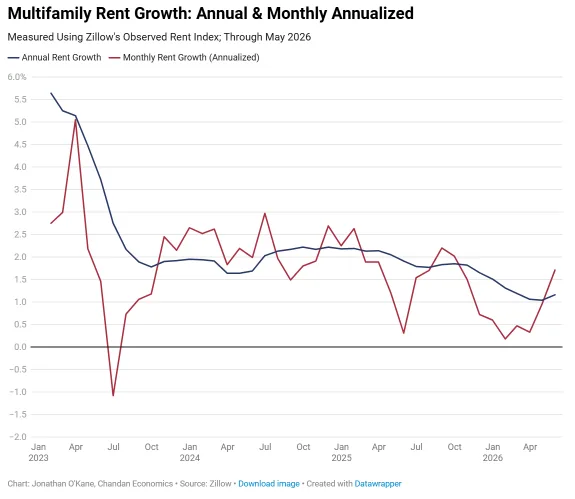

- US multifamily rents rose 1.2% year-over-year in May, marking the strongest acceleration since late 2024, based on Zillow’s index.

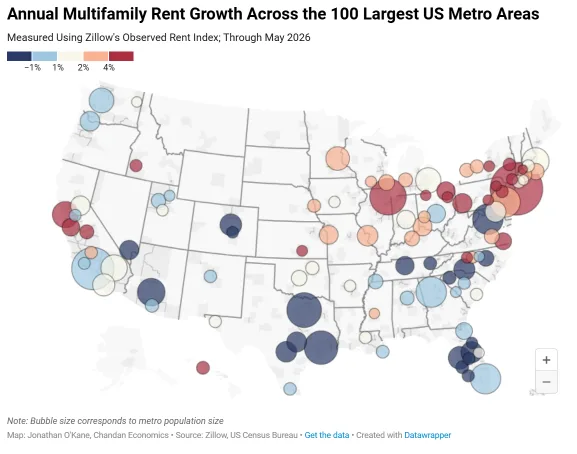

- Regional performance remains highly uneven, with the Midwest, Northeast, and coastal California seeing outsized gains and many Sun Belt metros still declining.

- The data suggest a gradual stabilization in national rent growth, signaling a potential end to the downward momentum seen throughout 2025.

Cooling Phase May Have Bottomed Out

After more than a year of deceleration, multifamily rent growth in the US may be turning a corner. According to an analysis of the Zillow Observed Rent Index (ZORI) cited by Chandan Economics, national apartment rents were up 1.2% year-over-year in May 2026, an uptick from 1.0% in April. While this level is muted compared to the highs of the pandemic boom, it’s the first clear signal of strengthening since late 2024. The data show gains picking up in a majority of metro areas, with 70% of surveyed metros posting monthly rent increases in May—the widest breadth of gains since September 2025.

This possible inflection comes as the market works through a wave of new supply in key cities and faces shifting demand fundamentals. With national rent growth running well below long-term averages, owners and investors are watching for stabilization as a potential floor after a protracted cooldown. The evidence from May suggests that, while far from robust, momentum has become more balanced and less negative than in past quarters.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

National multifamily rent growth reached 1.2% in May, up from 1.0% in April. Monthly momentum also improved. Annualized monthly growth rose to 1.7% from 1.0%. That marked the strongest reading since October 2025. Meanwhile, 70% of metros posted monthly rent gains. Another 86.4% recorded annual growth, nearly matching April.

Local markets remained divided. The Midwest, Northeast, and several coastal California metros led growth. San Francisco topped the list with a 6.7% annual gain. Urban Honolulu followed at 6.2%. Akron and Virginia Beach each grew 5.5%. Toledo posted a 5.4% increase. However, high-supply Sun Belt markets continued to struggle. North Port fell 5.7%. Cape Coral dropped 5.1%. Austin declined 3.9%, while San Antonio fell 3.5%. Denver rents slipped 2.9%.

Momentum Remains Market-Specific

While the national data show an uptick, momentum remains uneven across markets. Month-over-month, gains concentrated in many of the same metros leading annual performance. For example, Fresno and San Francisco each posted 1.0% growth in May, while Poughkeepsie, Syracuse, and Boise City also outperformed on a short-term basis. Conversely, Knoxville, Austin, and San Antonio recorded monthly declines of 0.4% or more.

This reinforces a broader trend seen in the last year: regional divergence is deepening. The Midwest and Northeast—along with select California coast markets—continue to benefit from modest supply growth and steady demand, supporting rent increases. Meanwhile, parts of Texas and Florida, along with Denver, still face supply-driven pressures that are weighing down rents. As such, national averages obscure a market increasingly shaped by local fundamentals.

Why It Matters

The latest figures from Zillow signal that nationwide rent growth is beginning to break out of its holding pattern. For owners, stabilized or gently rising rents suggest some relief after a challenging period marked by oversupply and decelerating fundamentals. Investment strategies—whether in core, value-add, or Sun Belt markets—must account for this new patchwork of winners and laggards. While the 1.2% year-over-year gain is a far cry from the double-digit increases seen in 2021 and 2022, it interrupts the downward trend that defined much of 2025.

CBRE’s Q1 2026 report also noted that national multifamily vacancies have plateaued, hinting that excess supply is beginning to be absorbed. New apartment deliveries have also started to slow, helping vacancy rates hold steady in several markets. Yet, as the data show, these trends are highly market-dependent. San Francisco’s 6.7% annual gain stands in sharp contrast to the –5.7% reading in North Port, FL, reflecting divergent supply pipelines and demand resilience. As such, underwriting, asset selection, and rent growth assumptions will remain a local game for the foreseeable future.

Looking forward, the improvements in both short-term momentum and metro-level breadth signal that the market is not headed for a sharp downturn. Instead, most indicators point to a slow, choppy climb for rents, especially as new deliveries are digested and economic growth remains steady. If supply pressures ease and job growth holds, the second half of 2026 could bring further market balance.

What’s Next

Looking ahead, industry analysts expect gradual improvement rather than a rapid upturn. The rent growth seen in May should provide a floor for national performance, but with construction completions still elevated in many metros, any rebound will likely be incremental. Investors should expect continued fragmentation, with market winners largely determined by local supply and demand conditions. As demand steadies and construction slows, especially in oversupplied Sun Belt metros, conditions may become more supportive of slow but steady rent growth through late 2026 and into 2027. The next two quarters will be telling for whether stabilization sticks nationwide or regional outliers continue to pull down the average.