- Disruption in the Strait of Hormuz is raising energy and shipping costs, pressuring logistics networks and industrial location strategy.

- US industrial rents grew 5.3% year-over-year in April while vacancies plateaued at 9.1%; Dallas keeps building despite elevated supply.

- Higher costs, regionalizing supply chains, and tenant-favored lease negotiations signal shifting fundamentals for operators and investors.

Energy Shock Upends Global Shipping and Industrial Strategy

The ongoing conflict in Iran and the resulting closure of the Strait of Hormuz have caused a swift energy shock, sending ripples through global supply chains. According to Yardi Matrix’s May 2026 National Industrial Report, about 20% of the world’s oil previously moved through the Strait, and its effective shutdown has sparked one of the largest oil market disruptions in decades. Shipping costs are up across all segments—gasoline, jet fuel, maritime bunker—leading to significantly higher logistics expenses for US industrial occupiers and pushing site selection back to the top of the strategic agenda.

While the world watched global supply chains adapt during the pandemic, this latest shock is testing the resiliency improvements many firms have implemented since then. The demand for infill facilities and assets near ports, rail, and highways is set to intensify as companies attempt to minimize cost exposure from lengthier and more expensive delivery routes.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

US industrial in-place rents hit $9.08 PSF in April, up 5.3% over the past 12 months. Atlanta led yearly in-place rent growth at 8.1%. Inland Empire followed at 7.1%, with Miami at 6.9%, Tampa at 6.7%, and Boston at 6.6%. The national vacancy rate reached 9.1%, up 30 basis points from last year. It has stayed largely flat since mid-2025.

Newly signed leases now average $9.99 PSF, or 91 cents above the in-place average. However, that margin has narrowed. In Southern California, new lease pricing now trails market averages in key markets. Los Angeles leases signed this year averaged $1.51 PSF below in-place rents. Orange County’s spread came in $0.61 lower. Even so, tight coastal supply should limit deeper rent declines, despite current tenant leverage.

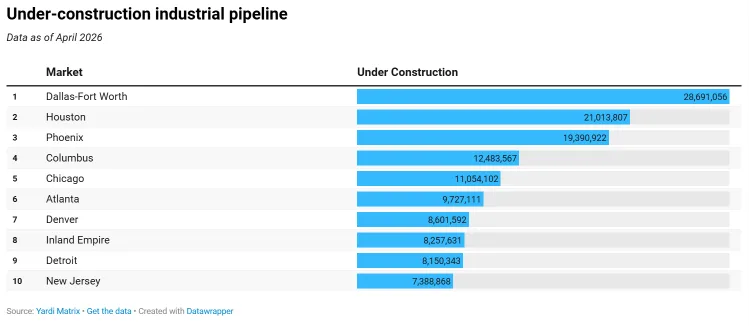

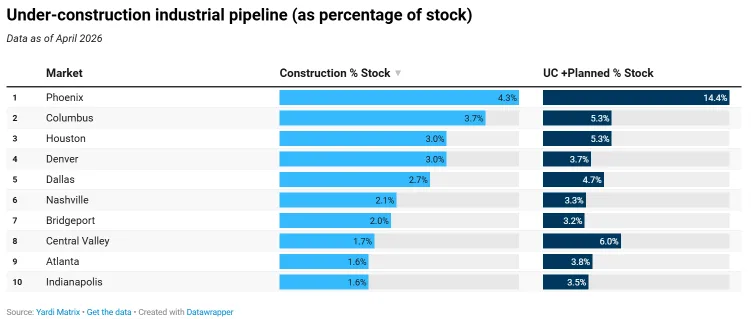

Nationwide, developers have 360.8M SF of industrial space underway, equal to 1.7% of inventory. Dallas leads the pipeline with 28.7M SF underway, or 2.7% of local stock. Recent supply pushed Dallas vacancy to 9.7%. Still, developers remain bullish on the market’s long-term growth. Population gains and its logistics hub status continue to support demand.

Regionalizing Supply Chains and Rents Diverge

The Iran conflict is driving up energy and shipping costs. It is also squeezing global supplies of petrochemicals, fertilizers, and helium. These shortages are raising costs for finished goods and advanced manufacturing inputs. The same pressure is already reshaping broader CRE demand, especially across logistics-heavy industrial markets. As producers and occupiers adjust, supply chain regionalization may accelerate again. Companies may keep more inventory near end users and seek regional hub properties.

The market is splitting. Fast-growth markets like Atlanta and the Inland Empire still post above-average rent gains. Meanwhile, rent growth softened in Memphis at 2.3%, Denver at 3.0%, and Detroit at 3.0%. The upper Midwest and Heartland metros face slower absorption. Still, high-demand coastal and Sun Belt markets remain competitive for infill and port-adjacent logistics space.

New construction also remains concentrated. Dallas, Houston, Phoenix, and Columbus are building above the national average as logistics providers recalibrate their networks.

Why It Matters

With producer price inflation surging—US Bureau of Labor Statistics data show a 1.4% PPI gain in April, the highest monthly jump since 2022, and a 6.0% year-over-year increase—the industrial sector is at a crossroads. Over 75% of the monthly price hike was attributed to energy. As operators weigh whether to pass costs downstream, some may be forced to absorb margin compression, especially with consumer spending potentially dampened by higher transportation costs and inflation.

Leasing fundamentals are still robust for the highest-quality space, but the shift in negotiating power (noted by Yardi Matrix in Southern California) is worth watching elsewhere. In markets where oversupply is still unwinding, owners could see further concessions. Still, there are bright spots: Dallas’s construction boom continues atop extraordinary absorption, and select secondary ports—like Philadelphia—are drawing major institutional investors. Philadelphia, for instance, saw its average industrial sale price climb over 150% since 2019, and EQT Real Estate’s recent $308.7M purchase of the Forest Park Corporate Center demonstrates institutional appetite for well-located distribution nodes.

Investors, developers, and operators now face a more fragmented national landscape where regional rent growth, vacancy, and development pipelines can diverge rapidly. CBRE and JLL’s recent outlooks both note that while national vacancy may stay elevated in the short term, quality, flexibility, and proximity will be at a premium as US supply chains go local in the face of ongoing global instability.

What’s Next

If the Iran conflict persists into summer or beyond, the impact on global energy and materials supply will likely anchor higher costs and longer lead times into industrial contract negotiations. This could drive further polarization between tenant-favored and landlord-favored markets, extending the current lull in rent growth for some metros while sharpening the focus on location-critical facilities.

Dallas and other supply-heavy Sun Belt markets will need sustained demand to absorb record new space—especially if consumer spending wanes. Watch for infill development in core logistics hubs, consolidation by top institutional investors in port markets, and an acceleration of reshoring or nearshoring strategies as US firms look for new ways to insulate themselves from geopolitical shocks. Higher developer costs and construction delays may also restrict future pipeline growth, tightening fundamentals in select markets as supply finally tapers off in 2026 and beyond.