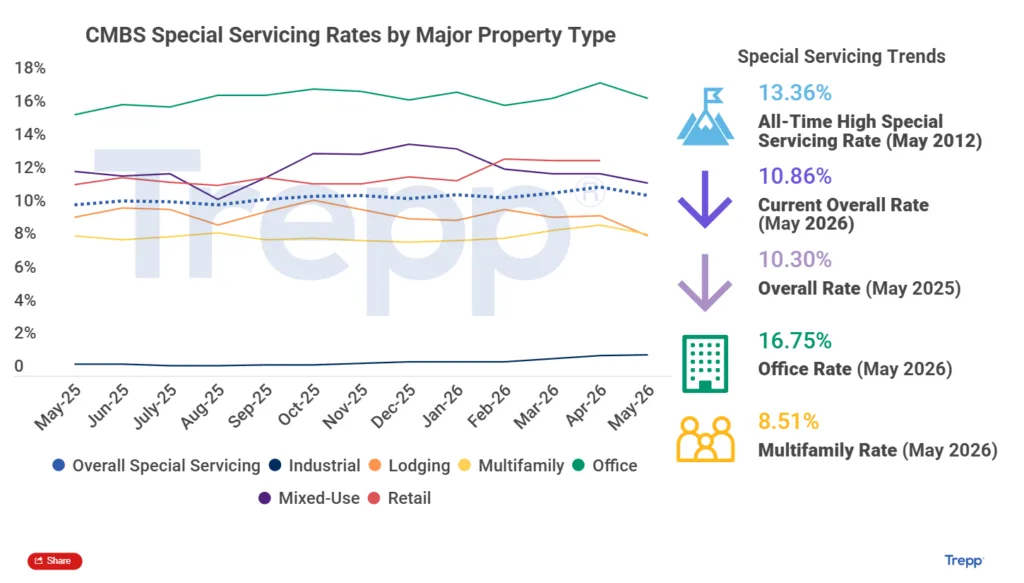

- The US CMBS special servicing rate declined to 10.86% in May 2026, per Trepp, as resolutions outnumbered new loan transfers.

- Office segment led improvements with a 91-basis-point drop, but distress remains broad, with new trouble across office, retail, and mixed-use loans.

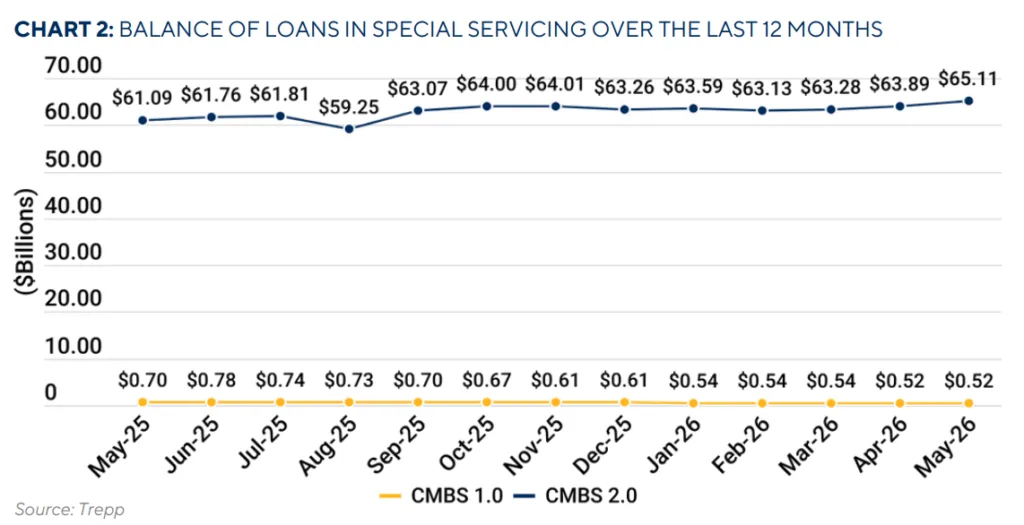

- The gap between legacy CMBS 1.0 and post-crisis CMBS 2.0+ special servicing rates highlights persistent risk in older vintages.

Pace of Resolutions Leads Decline

According to Trepp’s May 2026 Special Servicing Report, the US CMBS special servicing rate fell 51 basis points month-over-month to 10.86%. This retreat comes even as $2.9B in new loans, mostly in office and retail, transferred to special servicing. The reduction stemmed from a combination of several large office loans curing and the denominator effect—an expanded overall CMBS balance diluting the impact of new distress. Key improvements were driven by transfers of mature loans back to master servicers, signaling that lenders and borrowers are successfully negotiating workouts even in stressed segments.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

May’s special servicing rate fell 51 basis points to 10.86%, marking 2026’s largest monthly decline. Office rates fell 91 basis points to 16.75%. Mixed-use rates dropped 59 basis points to 11.62%. Multifamily fell 57 basis points to 8.51%. Lodging declined 121 basis points to 8.45%. Meanwhile, industrial rose to 1.28%, while retail increased to 13.00%.

New transfers included the 20 Times Square loan. The Manhattan property defaulted at maturity despite a 4.06x DSCR in 2025. Lenders also transferred International Square, a 1.16M SF office property in Washington, D.C., ahead of its August 2026 maturity. Large loan cures supported the improvement. One New York Plaza returned to the master servicer after an extension and paydown. Meanwhile, 700 Broadway in Denver stabilized following a previous modification.

Distress Lingers Despite Metric Improvement

While headline rates are moving lower, Trepp’s report underlines that distress is still widespread and not confined to large trophy assets. May saw a continued influx of mid-tier office, multifamily, industrial, and select lodging loans into special servicing. Portfolio-wide, retail’s slight rate increase and industrial’s reversal of recent improvements highlight the uneven nature of the recovery. Among legacy CMBS 1.0 loans, special servicing remains dire—standing at 61.59% compared to 10.79% for post-crisis CMBS 2.0+—revealing persistent legacy risk as older deals face outsized maturity walls and underwriting issues.

Why It Matters

The May 2026 figures from Trepp show the first meaningful signs of healing in the CMBS special servicing market. The rate fell 51 basis points as loan cures and modifications outpaced new defaults. In May, $1.03B in loans returned to the master servicer or paid off. Notably, office towers in Manhattan and Denver secured extensions and improved performance. Those resolutions helped drive the overall rate lower.

However, distress remains widespread. Borrowers transferred 59 loans totaling $2.9B into special servicing during May. Office properties continue to face refinancing pressure and elevated vacancy. This pressure aligns with a broader rise in office loan extensions, as borrowers seek more time to refinance maturing debt. Moreover, headline improvements mask ongoing challenges. Office loans returning to good standing still average occupancy in the 70% to 80% range. One New York Plaza reached 81% occupancy in April 2026. Meanwhile, assets like International Square still face tenant and refinancing risks.

Legacy CMBS 1.0 deals remain a major concern. Their special servicing rate exceeds 61%, more than five times CMBS 2.0+ vintages. As a result, lenders, servicers, and investors remain cautious about older portfolios.

What’s Next

Market attention will remain fixed on maturity walls, negotiated workouts, and the pace of loan resolutions as 2026 progresses. With office distress still dominating transfers and legacy portfolios weighing on overall metrics, the industry faces a critical test: whether new workouts continue to offset incoming defaults, or if market stress re-emerges as interest rates and refinancing conditions fluctuate. Upcoming maturities, especially in the office and retail segments, are likely to drive further volatility in special servicing rates, keeping lenders, servicers, and investors on high alert as the cycle plays out into early 2027.