- JLL’s new Global Credit Intensity Index reports record competitiveness among CRE lenders and greater borrower leverage worldwide.

- The divergence between aggressive lending and only modestly rising buyer competition creates a rare window for borrowers to lock in favorable financing.

- Sectors with strong rent growth are seeing deals move, but underwriting challenges are holding back transactions for riskier assets.

Tracking a New Liquidity Cycle

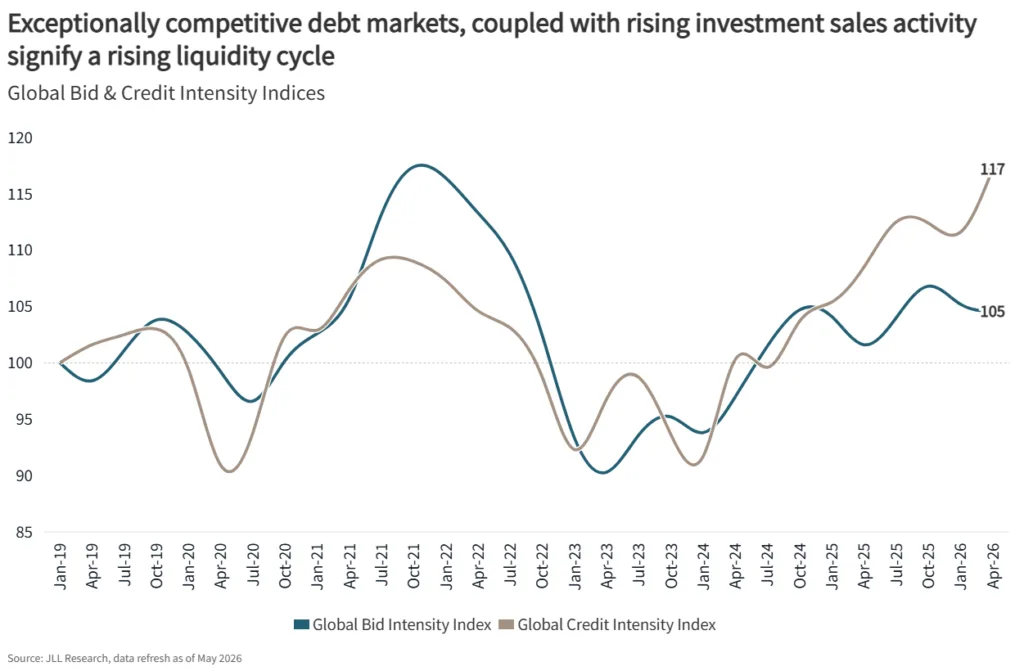

JLL rolled out its Global Credit Intensity Index (CII), aiming to complement the firm’s established Global Bid Intensity Index, according to the latest JLL insights. The CII tracks activity levels among lenders and the terms they offer, providing investors with a timely read on global credit market dynamics. The move comes as debt markets worldwide show signs of a new, highly competitive liquidity cycle, with lender appetite for deals now at, or near, record intensity. Paired with JLL’s Bid Intensity Index—which reflects how many investors are chasing assets and bidding strategies—the new tool gives CRE professionals a two-sided view on capital flows and deal competitiveness globally.

This launch matters as investors wrestle with capital allocation in what JLL calls a dramatically changed liquidity environment. The report finds credit markets entering “borrower’s market” territory, with an elevated number of active lenders offering ever-more aggressive terms. Bidder competition is strengthening too, but the real driver for the moment is deep and growing lender liquidity.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

How the Indices Work

The Global Bid Intensity Index is built by tracking two main data points each month: (1) the count of unique buyers actively bidding on investment sales, and (2) the bid-ask spread between seller expectations and winning offers. JLL notes that while price gaps have narrowed from the 2023 trough, transaction competitiveness remains below the frenzied peaks of 2021—especially in sectors like US multifamily, where underwriting hurdles persist.

The Global Credit Intensity Index, meanwhile, tracks (1) the number of unique lenders competing on loan requests each month, and (2) the average winning loan-to-value (LTV) ratio. This provides a direct signal on both lender appetite and tolerance for risk. April 2026 saw the CII hit an all-time high, with both lender competition and average LTVs rising sharply, per JLL.

Bidding and Lending Dynamics Shift

Bidder competition is on an upward trend but lags the credit side, per JLL’s findings. Sectors with stronger, predictable rent growth are seeing transactions materialize as buyers and sellers get closer on pricing. That trend aligns with recent data showing investment sales activity gaining momentum globally as pricing expectations continue to converge. However, assets requiring more complex underwriting or in less transparent markets still face slowdowns.

On the debt side, lender competition—measured both by headcount and higher accepted LTV ratios—signals deep capital chasing deals. The number of lenders quoting on new loans holds near historic highs, and those same lenders are increasingly willing to stretch leverage, reflecting higher risk tolerance compared to earlier in the cycle.

Divergence in Buyer and Lender Behavior

This split between hyper-aggressive lending conditions and only moderate improvement in bidding means investors equipped to move can, in many segments, secure superior financing before market competition for the assets themselves heats up. JLL advises borrowers to actively evaluate refinancing options on legacy assets and to act swiftly on new acquisitions where fundamentals align.

According to JLL’s analysis, the bid-ask spread has largely stabilized but remains a sticking point for illiquid or hard-to-value properties. Sectors with clearer growth stories are seeing that gap close further, with willing buyers leveraging current lender generosity to secure long-term debt. Still, for much of the market, buyers remain disciplined, and lenders’ aggressive stance is providing rare short-term negotiating leverage.

What’s Next

JLL’s combined indices suggest that the CRE lending environment globally will stay highly competitive in the near term, especially as more borrowers look to refinance or expand portfolios amid stabilizing interest rates. With lender appetite outpacing bidder aggressiveness, dealmakers prepared to transact now may benefit from historically borrower-friendly conditions, but JLL notes that pricing discipline is likely to persist, especially in sectors with underwriting complexity. Investors should watch for further convergence between buyer and lender markets as asset-level fundamentals and broader economic sentiment continue to evolve through the remainder of 2026.