- Multifamily construction permitting is accelerating fastest in smaller US markets, with unit growth rates outpacing major cities.

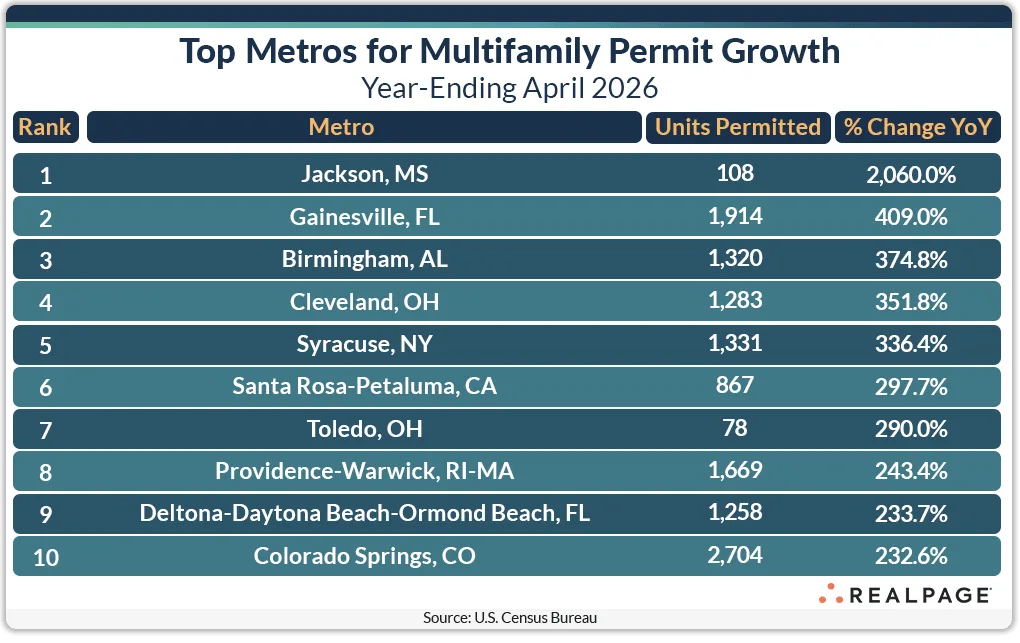

- Jackson, MS, leads in percentage growth, while markets like Gainesville, FL, and Toledo, OH, also post notable spikes in new permits.

- The sharp rise in permitting prompts concerns over potential oversupply relative to smaller inventory bases.

Small Markets Fuel Surge in Multifamily Construction

While top-tier metros like New York, Dallas, and Los Angeles continue to dominate total multifamily permitting volumes, 2026 is seeing smaller US cities driving the highest percentage gains in new units permitted, per RealPage.

Markets including Jackson, MS, Gainesville, FL, and Toledo, OH, have all logged significant year-over-year jumps. The trend signals that developer appetite for multifamily remains strong outside the usual urban powerhouses.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Rising Permits in Smaller Metros Shift the Narrative

Historically, monthly permitting rankings are led by large metros. According to RealPage data through April 2026, the five biggest gainers in annual multifamily permits among smaller markets have posted increases between 233% and 409%. For example, Jackson, MS, saw a 2,000% jump— from just 5 units permitted for the year ending April 2025 to 108 units in 2026. Similar percentage spikes are now appearing in places like Gainesville and Cleveland, though actual unit numbers still trail national leaders.

The Details

The strongest percentage increase occurred in Jackson, Mississippi, where annual multifamily permitting rose roughly 2,000%. However, the jump reflects growth from just five units permitted during the prior year period to 108 units during the latest reporting window.

Other smaller markets posted more substantial increases in absolute unit counts. Several added more than 1,000 units year over year while maintaining permit activity above the 1,200-unit threshold. Gainesville, Florida, recorded the highest inventory growth among the leading permit-growth markets, with new construction equal to approximately 6.1% of existing apartment inventory.

Meanwhile, Cleveland and Toledo, Ohio, along with Jackson, remained below a 1% inventory increase despite their elevated permitting growth rates. Those figures suggest that headline percentage gains do not always translate into significant market-wide supply shocks.

Urban Giants Hold Volume, Small Markets Take Growth

Large cities remain the big movers in absolute numbers, with New York, Dallas, Los Angeles, Houston, and Phoenix accounting for the largest volumes. Yet the real story of 2026 is the relative growth in smaller metros. Miami permitted 4,178 more units year-over-year, Denver 3,321, and Washington, DC, 2,682. The total number of units permitted in the top ten metros reached 148,078 for April, up 23.7% from the prior year, but slightly down 1% month-over-month according to RealPage. Meanwhile, major declines occurred in metros like San Antonio, Orlando, and Austin, each losing thousands of permits year-over-year.

Why It Matters

The latest multifamily permitting data highlights how development activity continues to diversify beyond traditional apartment strongholds. Large metros still account for the bulk of new units, but developers are increasingly identifying opportunities in smaller markets where demographic growth and housing demand may support additional projects.

For investors, the shift creates both opportunity and risk. Markets posting triple-digit permitting growth can offer attractive development economics and less competition than gateway cities. However, smaller inventories make those locations more vulnerable to supply-demand imbalances if leasing activity slows.

The data also underscores the importance of evaluating permitting trends through multiple lenses. Percentage growth alone can exaggerate market momentum when starting volumes are low. Inventory growth rates often provide a clearer picture of how new supply may affect fundamentals.

At the national level, the top 10 permitting metros collectively issued 148,078 units during the year ending in April 2026, up 23.7% from a year earlier. That increase signals continued confidence in long-term apartment demand despite elevated financing costs and ongoing economic uncertainty.

What’s Next

Despite scattered local headwinds, national multifamily permitting totals remain elevated, suggesting that construction pipelines will stay full through 2026. Watch for signs of lease-up stress in small metros with outsized growth, particularly as projects deliver. States like Texas and Florida continue to dominate permitting volume, even as select markets within those states slow. The shifting distribution of new supply across both primary and smaller markets will be a key theme for developers, brokers, and investors tracking multifamily performance over the next several quarters.