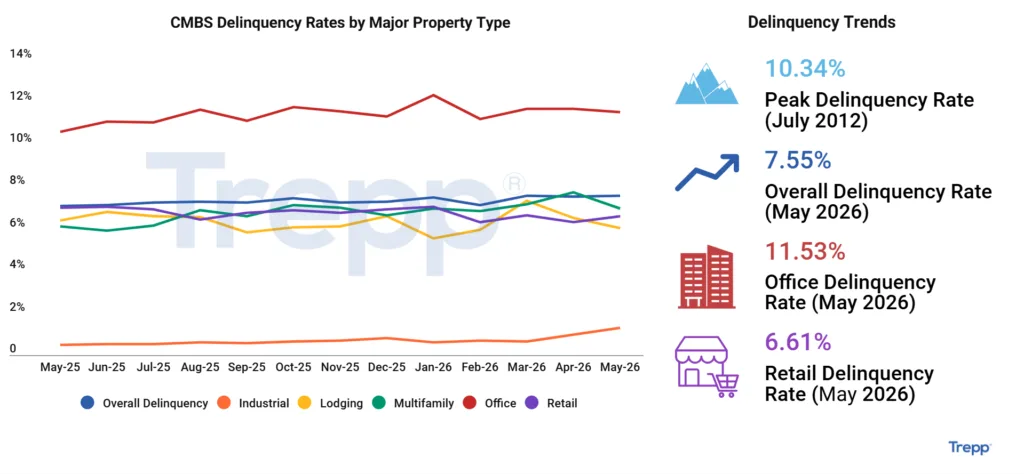

- The US CMBS delinquency rate ticked up to 7.55% in May 2026, rising one basis point from April’s figure.

- Industrial and retail sectors saw increased delinquencies, while multifamily, office, and lodging posted declines or limited gains.

- Non-performing matured balloon loans made up 70% of new delinquencies, highlighting ongoing refinance risk in commercial mortgage-backed securities.

CMBS Delinquencies Edge Up in May

The US CMBS delinquency rate inched up to 7.55% in May 2026, per Trepp’s latest report. This marks a one basis point increase month-over-month and keeps levels near recent highs. The largest newly delinquent loans totaled $1.86B and spanned major metros and asset classes. The list ranged from Orlando hotels to a Times Square ground lease, affecting nearly every CRE sector.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Refinancing Challenges Drive Delinquency Mix

Persistent headwinds, including high rates and tough refinancing conditions, continue to drive the mix of delinquent loans. According to Trepp, 70% of newly delinquent balances were classified as non-performing matured balloon—loans that failed to pay off at maturity but remain in limbo. Another 28% of new delinquencies were in the 30-day bucket, while the remaining 2% are mostly in foreclosure. This highlights just how much maturity issues, rather than operational distress, are pushing loans into delinquency.

Sector Breakdown

Delinquency rates diverged among major property types. Industrial saw the sharpest jump, rising 35 basis points to 1.31% as several logistics and manufacturing loans became delinquent. Retail followed closely behind, increasing 30 basis points to 6.61%, weighed down by regional malls and shopping centers. On the upside, multifamily delinquencies dropped 76 basis points to 6.95%, recovering after an April spike. Office improved by 16 basis points to 11.53%, with cures and payoffs outpacing new trouble spots. Lodging edged down to 6.01%, though this was a technical shift as new issuance outweighed new delinquencies.

Refinancing Stress Remains Paramount

This modest uptick in the overall rate underscores the stickiness of delinquency risk in the current climate. According to Trepp’s data, non-performing matured balloon loans continue to dominate new delinquencies each month, reflecting ongoing challenges for borrowers unable to refinance or sell assets as major maturities come due. Loan performance remains weakest in urban office properties and regional malls. Those sectors have challenged lenders since interest rates began climbing in 2022.

Why It Matters

The May report shows that CMBS performance remains heavily influenced by capital markets conditions rather than purely property-level fundamentals. The one-basis-point increase may appear minor, but the composition of new delinquencies tells a more important story. With non-performing matured balloon loans accounting for the majority of new distress, refinancing risk remains one of the biggest threats facing commercial real estate borrowers.

That dynamic is especially relevant for lenders, servicers, and investors monitoring loan maturity schedules over the next several quarters. Trepp’s data show the headline delinquency rate has climbed 90 basis points from 7.08% a year ago, indicating that distress remains elevated even as some property sectors stabilize.

Office continues to warrant particular attention. Although monthly figures improved slightly, delinquency levels remain far above other sectors. Large CBD assets continue to account for some of the market’s most significant troubled loans, reinforcing concerns about long-term valuation and refinancing prospects across the office landscape.

What’s Next

Market participants will be watching whether the maturity-driven distress cycle begins to ease during the second half of 2026. Much will depend on capital availability, lender appetite, and the trajectory of interest rates. If refinancing conditions improve, some performing and near-performing loans could avoid slipping into delinquency.

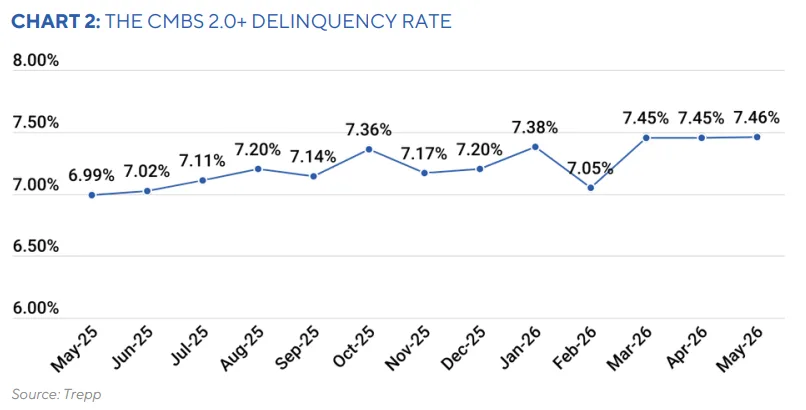

For now, the data suggest distress remains entrenched. Trepp’s CMBS 2.0+ delinquency rate also increased one basis point to 7.46% in May, indicating that challenges extend beyond legacy-vintage transactions. While multifamily and lodging posted encouraging results, continued weakness in office and rising retail and industrial delinquencies suggest the market has yet to achieve a broad-based recovery. Investors will likely remain focused on maturity schedules and refinancing outcomes as the next phase of the cycle unfolds.