- Repeat-sale indices showed US commercial real estate prices fell in April, ending nearly a year of gains.

- Largest price swing was the Woodland Pointe office sale near Washington, D.C., sold for $59.8M less than its prior price.

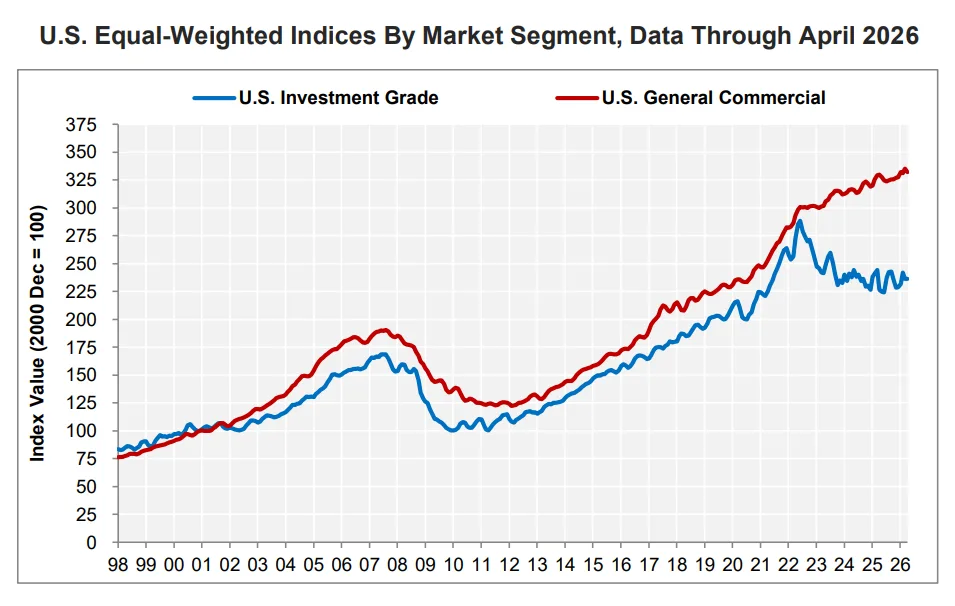

- Price declines were sharpest in the office sector, but industrial and retail assets continued to see gains.

Repeat-Sale Indices Point to Cooling Market

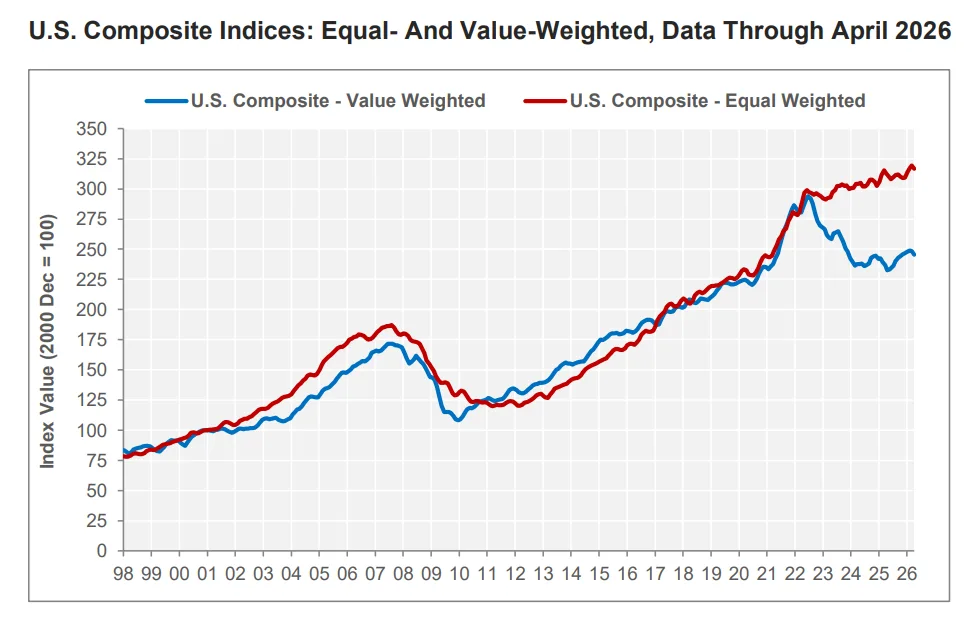

US commercial real estate prices registered their first monthly drop in nearly a year in April, based on new analysis from CoStar’s Commercial Repeat-Sale Indices (CCRSI). Both major indices, tracking high-value core market transactions and broader small market deals, slipped as select large office assets traded at steep discounts. Though both indices remain above last year’s levels, the April pullback marks the first clear cooling of momentum after a steady run-up since mid-2023.

Source: CoStar

Uneven Recovery From 2022 Peaks

After a steep sector-wide downturn in 2022, commercial values had notched incremental monthly gains through early 2026. According to Chad Littell, CoStar’s national director of US capital markets analytics, the current pace—1% to 3% year-over-year gains—is aligned with normalized, post-recovery markets, but far off the rapid growth seen in 2021. Littell cautioned that market recoveries are multi-year processes, rarely proceeding in a straight line. While values generally trend upward, monthly volatility is expected.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

The value-weighted US Composite Index, driven by major properties in large cities, fell 1.3% in April from March. Even so, it’s 3.5% higher year-over-year. The equal-weighted index, which better reflects activity in secondary and tertiary regions, dropped 0.9% on the month and is up just 1.2% over the last 12 months. Office sales drove the largest declines across both indices, with repeat office deals in April transacting $130.8M below their last sale values. The largest single price drop came from the sale of Woodland Pointe, a 185,000 SF office building in Herndon, Virginia, which sold for $40.2M—$59.8M less than its $100M price in 2008.

Source: CoStar

Office Assets Under Pressure, But Multifamily and Industrial Shine

Office was the clear laggard, but pockets of strength persist elsewhere. The month’s largest price gain was the $144.3M sale of Iconic on Alvarado, a 712-bed student housing asset near San Diego State University, which sold for $46.2M above its last recorded price, boosting the institutional multifamily segment by $79.4M. Retail repeat sales in April notched $34.8M in gains—up 26% from previous trades—while industrial assets doubled their prior values, adding $87.5M. This divergence highlights continued demand for necessity-driven retail and logistics, even as the office correction drags on.

Why It Matters

The mixed results signal a fragmented recovery across commercial property types. While average values are up year-over-year, volatility persists and key segments like office remain well below their pre-pandemic highs. According to CoStar, broader asset repricing is still underway, particularly for older or less competitive offices caught in structural demand shifts. Investors are watching for signals that office distress will spill into other asset classes—or if stable multifamily and industrial trends continue to underpin the broader market.

What’s Next

CRE professionals should continue monitoring repeat-sale indices for more signs of asset class bifurcation. If office price weakness deepens, distressed trades could pick up late in 2026, driving further price discovery. Meanwhile, industrial and retail resilience may attract more capital, especially if rent growth holds and new supply remains limited. The overall market is unlikely to return to 2021 pace soon, but further monthly swings—both up and down—should be expected as asset repricing plays out.