![The Agency delinquency rate fell to 0.49% in April, driven by program-level shifts as multifamily loan performance remained strong. [10:18 AM]strav mi e deka nema da gi stasame do 12](https://cdn.credaily.com/uploads/2026/06/pexels-andy-pluzhnik-545307-1309154-scaled.webp)

- The overall securitized Agency delinquency rate declined to 0.49% in April 2026, falling below its recent trading range.

- Fannie Mae, Freddie Mac, and Ginnie Mae displayed diverging delinquency patterns, primarily reflecting program structural differences rather than true credit degradation.

- With Agency loan performance still robust, future rate movements may hinge on the resolution of matured Freddie Mac loans.

Agency Delinquencies Move Lower in April

In April 2026, the Agency delinquency rate fell to 0.49%, breaking below the narrow band that had defined performance since mid-2025, per Trepp. The decline points to continued stability across the multifamily lending market, where borrowers have largely maintained strong payment performance despite elevated interest rates and ongoing refinancing challenges.

The improvement was modest, but it reinforces a broader trend: distress remains limited across agency-backed multifamily portfolios, even as parts of the CRE market continue to grapple with maturity risk and capital market volatility.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Breaking Below The Range

According to Trepp’s April 2026 Agency loan performance analysis, delinquency levels moved below the range that had prevailed since mid-2025. While the headline figure improved, the shift was driven less by changes in borrower behavior and more by the composition of loans within securitized agency programs.

Agency credit metrics remain exceptionally healthy. As of April 2026, 99.27% of outstanding balances were current, while early-stage payment delinquencies remained stable. Foreclosure activity was effectively nonexistent, underscoring the strength of multifamily fundamentals relative to other CRE property types.

The data suggests that the agency lending market continues to benefit from stable occupancy levels, consistent rent collections, and underwriting standards that have generally held up through the current interest-rate cycle.

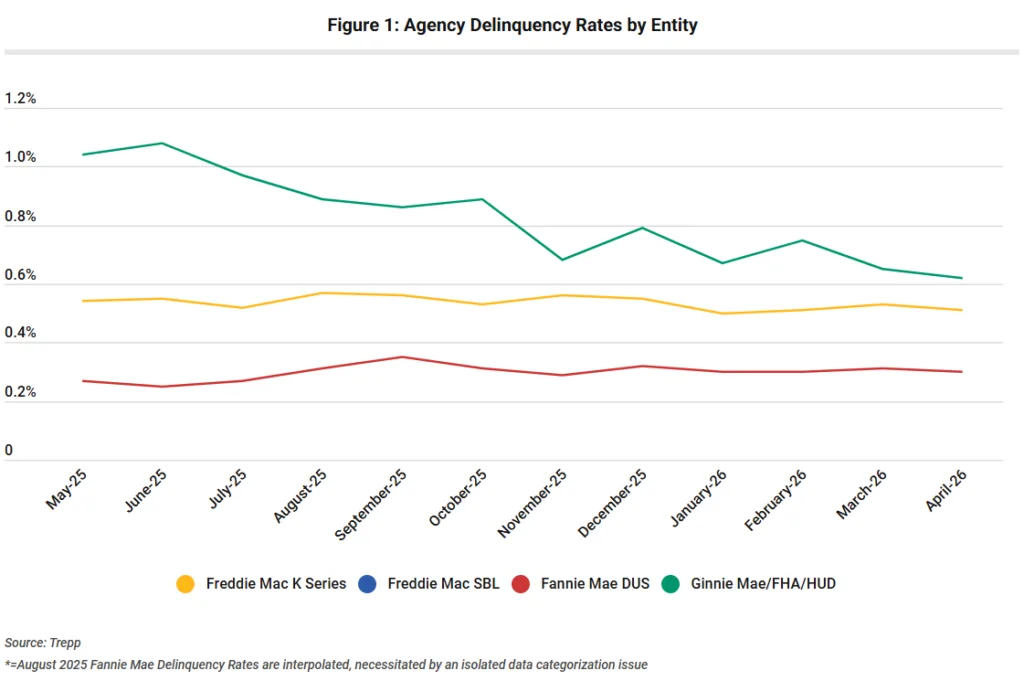

Fannie Mae, along with FHA and HUD programs, saw the most notable drop to 0.62%, continuing a year-long trend of improvement. These discrepancies owe more to securitization mechanics and maturity handling than to actual credit deterioration among underlying loans.

Program Features Outweigh Credit Quality Shifts

Freddie Mac’s delinquency rate declined to 0.81%, remaining the highest among agency issuers. The elevated figure continues to reflect the treatment of matured loans that remain within securitized pools rather than widespread payment stress among borrowers.

Fannie Mae’s delinquency rate fell to 0.30%, staying within the tight range that has characterized its portfolio since mid-2025. Meanwhile, Ginnie Mae, FHA, and HUD-backed loans improved to 0.62%, extending a year-long trend of declining delinquencies.

Notably, serious delinquencies within Ginnie Mae programs continued to shrink while total outstanding balances expanded. That combination helped dilute legacy distressed loans and contributed to overall improvement across the agency universe.

Freddie Mac Maturity Risk

While overall performance remains strong, Freddie Mac continues to stand apart from its peers because of how its securitization programs handle matured loans.

Much of the remaining delinquency pressure stems from loans that have reached maturity but have not yet been resolved, particularly within Freddie Mac’s Small Balance Loan program. These loans can remain classified as delinquent within securitized pools even when underlying property performance remains stable.

As a result, headline delinquency figures can sometimes overstate actual borrower distress. The divergence between Freddie Mac and other agency issuers reflects structural program mechanics rather than a meaningful deterioration in credit quality.

For investors and lenders tracking agency-backed securities, that distinction remains critical. The gap between reported delinquency and actual credit stress continues to shape performance metrics across the sector.

Why It Matters

This continued stability underscores CRE’s relative resilience in the Agency-backed segment. For multifamily lenders, investors, and bondholders, the data offers another indication that Agency-backed credit remains remarkably stable despite ongoing pressure in other CRE sectors.

While office and certain transitional property loans continue to face elevated stress, Agency multifamily portfolios have largely avoided significant deterioration. Trepp’s April 2026 figures suggest current borrower payment performance remains strong and that delinquency fluctuations are being driven more by portfolio mechanics than by worsening fundamentals.

What’s Next

With the Agency delinquency rate now below 0.50%, future performance will likely depend on the pace at which matured Freddie Mac loans are resolved.

If those loans are worked out efficiently and Ginnie Mae portfolios continue adding new originations while reducing seriously delinquent balances, overall delinquency could remain near historic lows through the remainder of 2026. Market participants will be watching whether maturity-related issues continue to outweigh otherwise stable multifamily credit conditions.