- National self-storage asking rates rose 1.0% month over month in April to $16.22 PSF, with 29 of the top 30 metros posting gains, according to Yardi Matrix.

- The development pipeline fell to 46.2M rentable SF under construction, representing 2.2% of existing inventory and marking a year-over-year decline.

- Slowing supply growth could help stabilize pricing power for operators, even as year-over-year rent performance remains negative across most markets.

Self-storage operators saw another month of pricing momentum in April, even as development activity continued to ease nationwide. According to Yardi Matrix’s May 2026 Self Storage Market Outlook, the national average annualized advertised asking rate climbed 1.0% month over month to $16.22 PSF across all unit types and sizes.

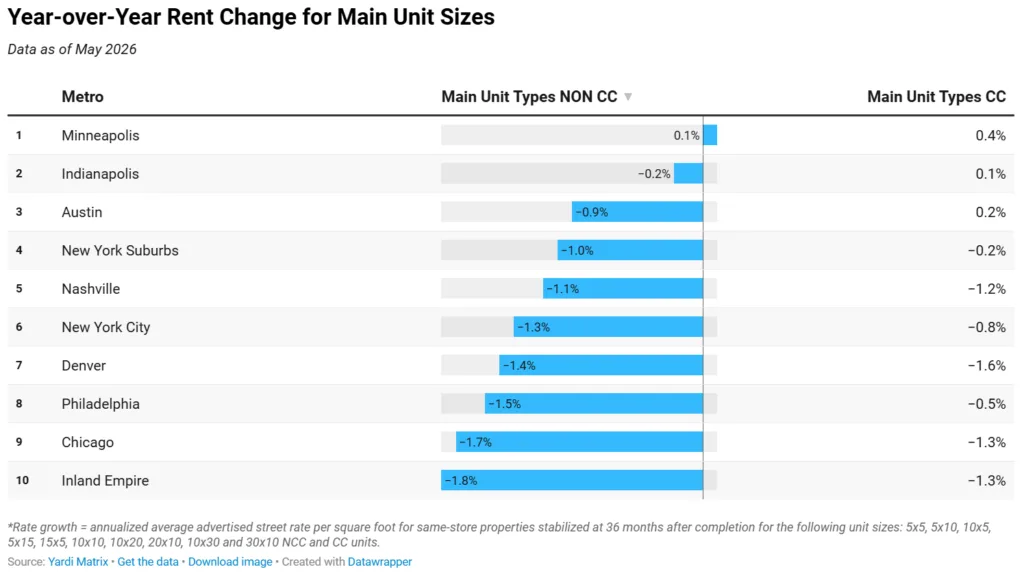

The monthly gains were widespread. Yardi Matrix reported that 29 of the top 30 metros recorded positive advertised rate growth in April, with San Antonio the only market to remain flat. The stronger monthly performance comes despite ongoing annual declines in both climate-controlled and non-climate-controlled storage rents across most major metros.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Monthly Pricing Momentum Persists

April marked another month of broad-based rent increases for the self-storage sector, extending a trend that has emerged in early 2026. Rates for non-climate-controlled units still posted year-over-year declines in 29 of the top 30 metros tracked by Yardi Matrix, while climate-controlled units fell annually in 27 markets.

That divergence highlights the sector’s current dynamic: operators are regaining some short-term pricing power as supply pressures moderate, but many markets are still working through elevated inventory levels delivered during the post-pandemic construction boom.

The Details

Yardi Matrix reported 2,560 self-storage properties in some stage of development nationwide in April. That total included 618 properties under construction, 1,642 planned projects, and 300 prospective developments.

The under-construction pipeline totaled roughly 46.2M rentable SF, down 0.1% from March 2026 and 0.3% year over year. Properties currently under construction represent 2.2% of existing national inventory.

Most metros saw little to no development growth. Of the top 30 markets tracked by Yardi Matrix, only three posted month-over-month increases in under-construction supply: San Diego, Houston, and Boston. San Diego recorded the sharpest increase, rising 110 basis points to 3.1% of existing inventory under construction.

Meanwhile, Phoenix and Sarasota-Cape Coral continued to lead the country in new supply concentration, with each market carrying under-construction inventory equal to 6.5% of existing stock. Both metros, however, experienced pullbacks from March levels. Sarasota-Cape Coral posted the steeper decline, dropping 130 basis points month over month.

Supply Pressures Begin To Ease

The slowdown in new construction reflects a broader recalibration across commercial real estate development pipelines. Higher financing costs, tighter lending conditions, and softer rent growth have made speculative self-storage projects more difficult to pencil.

Some markets are already seeing development activity stall almost entirely. Portland, Oregon, ranked last among Yardi Matrix’s top 30 metros for the third straight month, with under-construction supply holding steady at just 0.5% of inventory since February.

The moderation could offer relief for operators that spent the past two years competing against a wave of new facilities. Self-storage fundamentals remain stronger than many other commercial property types, but the sector has faced slower rent growth after pandemic-era demand normalized. Demand trends also remain uneven nationwide, even during the sector’s traditionally stronger leasing months.

Why It Matters

The self-storage sector appears to be moving into a more balanced phase after several years of aggressive expansion. Slower construction activity could help operators rebuild occupancy and stabilize rents, particularly in oversupplied Sun Belt markets.

The latest data also suggests investors are becoming more selective about development opportunities. Markets with heavy supply pipelines, including Phoenix and parts of Florida, may continue to face near-term pressure on rents and lease-up performance. But nationally, shrinking construction volumes could support healthier fundamentals heading into 2027.

What’s Next

Operators and investors will be watching whether monthly rent gains can continue through the peak summer leasing season. If construction activity continues to slow while demand remains steady, self-storage owners could regain stronger pricing leverage in the second half of 2026.

Attention will also remain focused on high-growth metros where supply levels are still elevated. Markets like Phoenix, Sarasota-Cape Coral, and Houston may serve as early indicators of how quickly the sector can absorb new inventory and return to sustained annual rent growth.