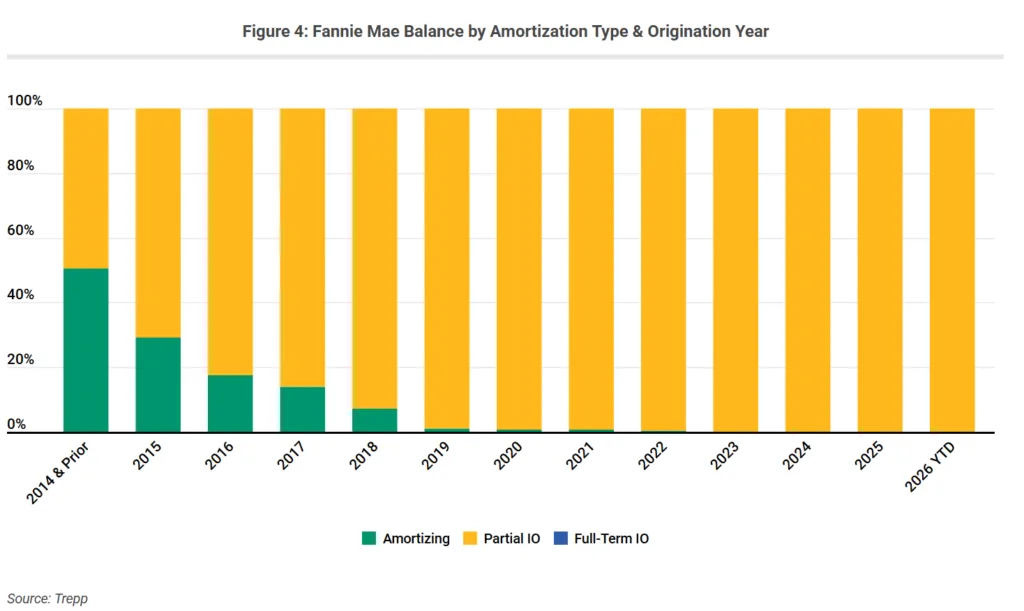

- Trepp data shows full amortization has largely disappeared from recent GSE multifamily loan vintages, with interest-only structures becoming the standard.

- Fannie Mae and Freddie Mac adopted interest-only lending differently, with Freddie Mac showing a larger share of full-term IO loans that preserve leverage through maturity.

- The shift increases refinance execution risk rather than immediate credit losses, making loan outcomes more dependent on interest rates, valuations, and NOI growth.

The GSE multifamily market is entering a new refinancing era as interest-only lending replaces traditional amortizing loan structures. According to a May 2026 Trepp analysis, the disappearance of amortization from Agency multifamily lending has materially changed how leverage evolves over a loan’s life, increasing borrowers’ dependence on favorable market conditions at maturity.

The shift matters because amortization historically acted as a built-in refinance cushion. As borrowers paid down principal over time, loan balances declined and refinancing became easier even if rates moved higher. Under today’s IO-heavy structures, many loans are reaching maturity with balances largely unchanged from origination.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

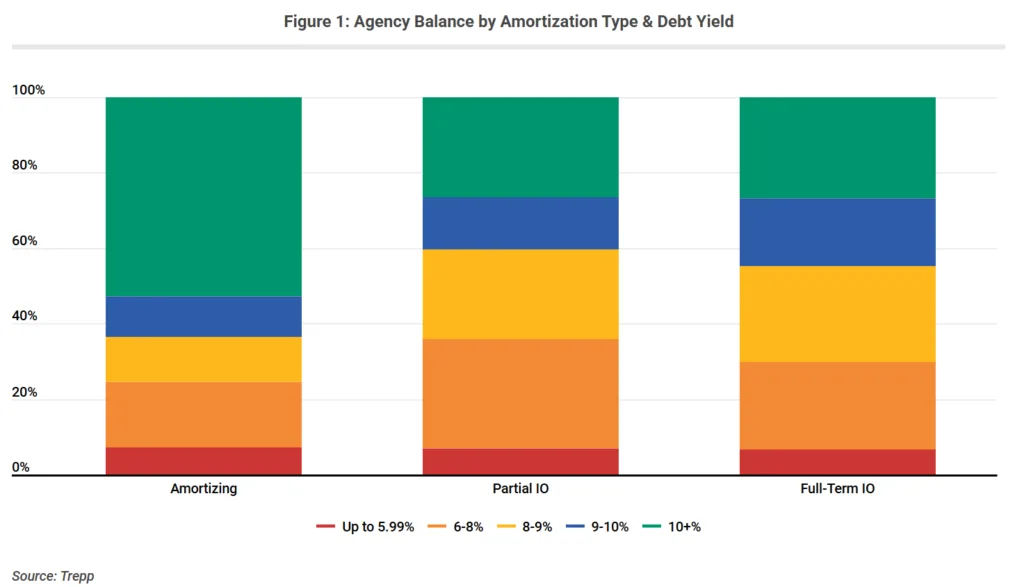

A Shrinking Refinance Cushion

Trepp’s analysis shows the decline in amortization accelerated after 2014 as Agency lenders increasingly adopted partial and full-term interest-only structures. Earlier loan vintages naturally migrated into stronger debt-yield positions over time because borrowers steadily reduced principal balances.

That dynamic has largely disappeared in recent cohorts. Instead of benefiting from automatic deleveraging, borrowers now depend more heavily on NOI growth, higher property values, or sponsor equity contributions to refinance successfully.

Trepp argues debt yield has become the clearest indicator of refinance sensitivity because most GSE multifamily loans were originally underwritten to debt service coverage ratio constraints. Fully amortizing loans continue to dominate the strongest debt-yield buckets above 10%, while IO loans are more concentrated in borderline or riskier refinance categories.

The Details

The report emphasizes that rising refinance risk does not automatically translate into rising credit losses. Trepp notes that refinance friction would likely need to coincide with sustained NOI declines or falling valuations before principal losses emerge across the Agency book.

Instead, stress is more likely to appear first through loan extensions, sponsor paydowns, modified takeout structures, or recapitalizations. The result is a market increasingly defined by maturity management rather than immediate defaults.

The distinction matters as multifamily owners navigate elevated borrowing costs in 2026. Loans originated during lower-rate periods now face refinancing at much higher coupons. At the same time, rising multifamily delinquencies have increased pressure across portions of the GSE lending market.

Fannie Mae vs. Freddie Mac

Trepp’s analysis also highlights a divergence between Fannie Mae and Freddie Mac’s IO adoption strategies. At Fannie Mae, the shift away from amortization has been driven primarily by partial IO structures, meaning some principal reduction still occurs later in the loan term.

Freddie Mac, by contrast, increased its use of full-term IO loans, leaving a larger portion of balances with no contractual deleveraging before maturity. While both agencies may have originated loans with similar initial debt-yield profiles, the long-term refinance trajectories now look materially different.

That distinction could become increasingly important as larger IO-heavy vintages approach maturity over the next several years.

Why It Matters

IO lending reflects a broader shift in multifamily finance over the past decade. Interest-only structures increased borrower flexibility and supported loan origination and transaction activity. They also gained traction during periods of compressed cap rates and intense lender competition.

However, higher interest rates have exposed the tradeoffs. Without amortization, leverage remains elevated throughout the loan term. As a result, refinance outcomes depend more on market conditions, valuation levels, and debt sizing at maturity.

Lenders, servicers, and investors now focus more on extensions, sponsor liquidity, and property performance. They can no longer rely only on delinquency metrics to measure stress. Instead, refinancing pressure may build gradually before triggering defaults.

What’s Next

The next test for the Agency multifamily market will come as larger cohorts of IO-heavy loans mature between 2026 and 2028. Borrowers facing refinancing gaps may increasingly pursue recapitalizations, equity infusions, or loan modifications to bridge proceeds shortfalls.

Much will depend on the path of interest rates and multifamily fundamentals. If NOI growth stabilizes and financing markets loosen, many borrowers may still refinance successfully despite higher leverage persistence. But if elevated rates coincide with weaker property performance or declining valuations, refinance execution risk could intensify across portions of the GSE multifamily market.