- Public REIT mergers represented $211B of the $324B in total US REIT M&A activity between 2020 and mid-May 2026, according to Nareit.

- Private buyers completed more deals by volume than non-listed REITs, but they largely targeted smaller and more specialized REIT portfolios.

- The consolidation wave is concentrating capital in larger listed REITs, with average public REIT market caps climbing from $6.5B to $8.7B over the period.

Public REIT consolidation has become the defining theme of US REIT dealmaking. While privatizations have generated headlines since 2020, most of the capital moving through the sector has stayed within the public market ecosystem.

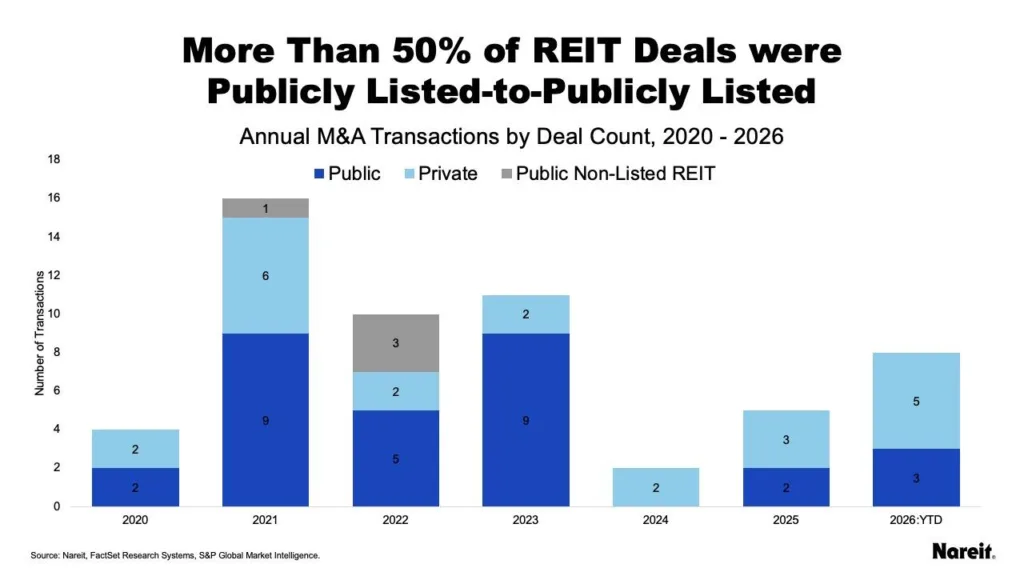

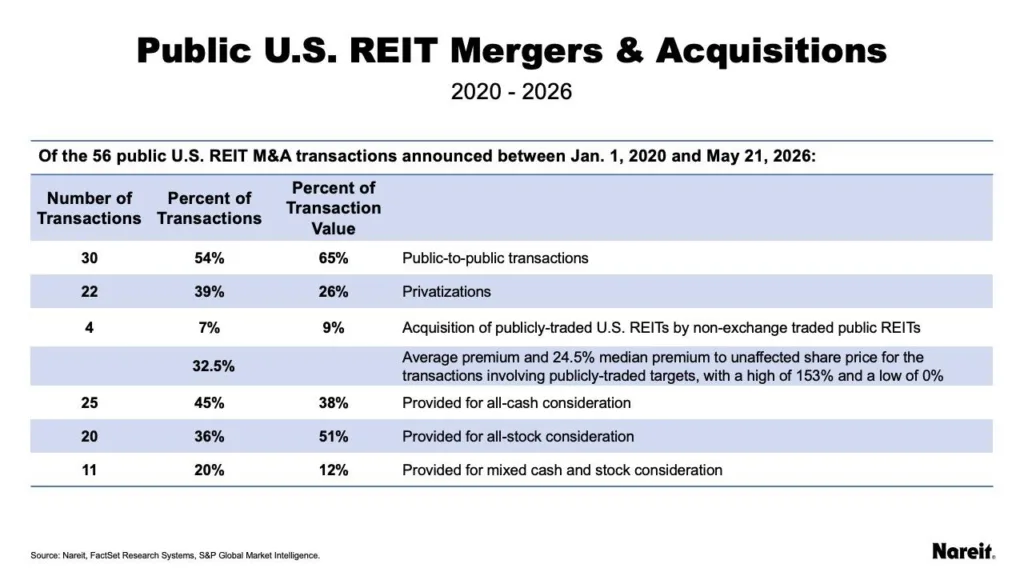

According to a May 2026 Nareit analysis, listed REITs completed 56 mergers and acquisitions transactions totaling $324B between early 2020 and mid-May 2026. Public-to-public mergers accounted for the majority of that activity, representing $211B, or roughly 65%, of total transaction value.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Shrinking Field With Bigger Players

The REIT industry consolidated quickly over the last six years, even as market values increased. Nareit reported listed REIT market capitalization grew from $1.2T in 2020 to $1.6T in 2026. Meanwhile, the number of listed REITs dropped from 223 to 189.

Consolidation created larger public real estate companies with broader portfolios and stronger capital access. Average listed REIT size increased from $6.5B to $8.7B during the same period. Additionally, 14 REIT IPOs raised more than $10B collectively, according to Nareit.

Larger REITs continue using mergers to improve operating efficiencies and expand into complementary property sectors. Many also use consolidation to strengthen balance sheets while capital costs remain elevated.

The Details Behind the REIT M&A Surge

Of the 56 transactions announced since 2020, 30 involved mergers between publicly traded REITs. Private entities completed 22 acquisitions totaling $83B, while non-listed REITs accounted for four acquisitions worth approximately $30B.

Deal structure varied significantly depending on the buyer type. All-cash transactions represented the largest share by count, accounting for 25 deals, or 45% of all transactions. Those deals represented 38% of total transaction value and were heavily tied to privatization activity led by private equity firms and institutional investors.

Stock-for-stock mergers, meanwhile, dominated the largest transactions. Nareit found that all-stock deals accounted for 51% of total deal value despite representing only 36% of deal count. Public REIT buyers have increasingly favored equity-based transactions to preserve liquidity while giving shareholders continued exposure to future upside in larger combined entities.

Mixed cash-and-stock structures remained relatively limited, representing 20% of transaction count and just 12% of total value.

Privatizations Still Shaped the Market

Although public consolidation dominated by dollar volume, privatizations remained a major force across the sector. Private buyers completed 22 transactions, or 39% of total deal count, over the six-year stretch.

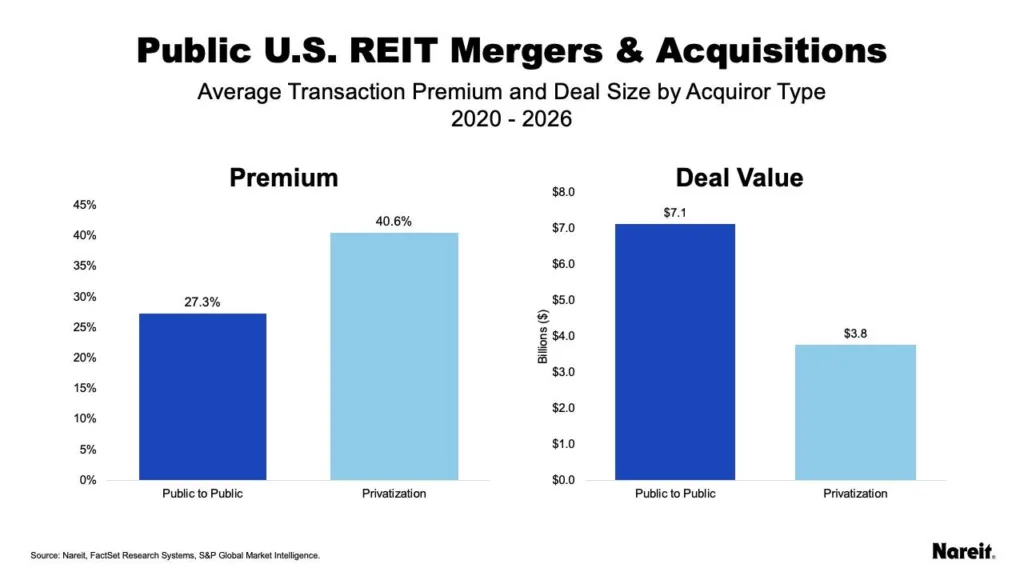

Those deals generally targeted smaller REITs and carried significantly higher acquisition premiums. According to Nareit, privatization transactions offered premiums more than 13 percentage points higher on average than public-to-public mergers.

The dynamic reflects a widening valuation gap within the sector. Private capital has focused on discounted public REITs with niche portfolios or sector-specific exposure, particularly where buyers see opportunities to reposition assets outside the scrutiny of quarterly public reporting.

Non-traded REITs also emerged as opportunistic acquirers during the cycle, pursuing public REIT portfolios across industrial, residential, retail, data center, and self-storage sectors.

Even so, privatizations accounted for just 26% of total transaction value, highlighting how the largest capital shifts continued to happen between listed REIT peers rather than through take-private deals.

Why Larger Public REITs Are Gaining Ground

The consolidation trend comes as institutional investors increasingly favor scale, liquidity, and portfolio diversification. Larger REITs typically enjoy lower borrowing costs, greater index inclusion, and stronger access to equity capital than smaller competitors.

That matters in an environment where higher interest rates and tighter lending conditions have pressured property valuations and refinancing activity across multiple asset classes.

Public REIT mergers also help companies lower operating costs across larger portfolios. They also improve tenant diversification and geographic reach. In sectors like industrial, apartments, and data centers, scale now drives technology and leasing advantages. That trend aligns with growing expectations for another CRE brokerage and advisory consolidation cycle.

According to Nareit’s 2026 analysis, nearly half of all deals effectively removed assets from public markets through privatizations or non-traded REIT acquisitions. But the majority of transaction value remaining inside the listed REIT universe suggests public markets still provide meaningful advantages for large-scale real estate ownership.

What’s Next for REIT Consolidation

REIT M&A activity could remain elevated through the rest of 2026 as valuation dislocations persist and companies continue searching for scale advantages. Public REITs trading below net asset value may remain attractive acquisition targets for both strategic buyers and private capital.

At the same time, stock-based mergers could become increasingly common if REIT share prices stabilize and financing markets remain expensive. Larger consolidators with stronger balance sheets are likely to keep pursuing sector-specific expansion opportunities, particularly in industrial, housing, infrastructure, and digital real estate.

For the broader CRE market, the last six years have made one thing clear: consolidation is no longer cyclical in the REIT sector—it’s becoming structural.