- Americans’ expected probability of moving within three years fell to 21.7% in 2026, signaling a housing market with sharply reduced mobility.

- Renters remain more likely to move than homeowners, but renter mobility expectations dropped more than 20 percentage points over the past decade.

- Affordability constraints, mortgage-rate lock-in, remote work flexibility, and aging-in-place trends are collectively making the US housing market less fluid.

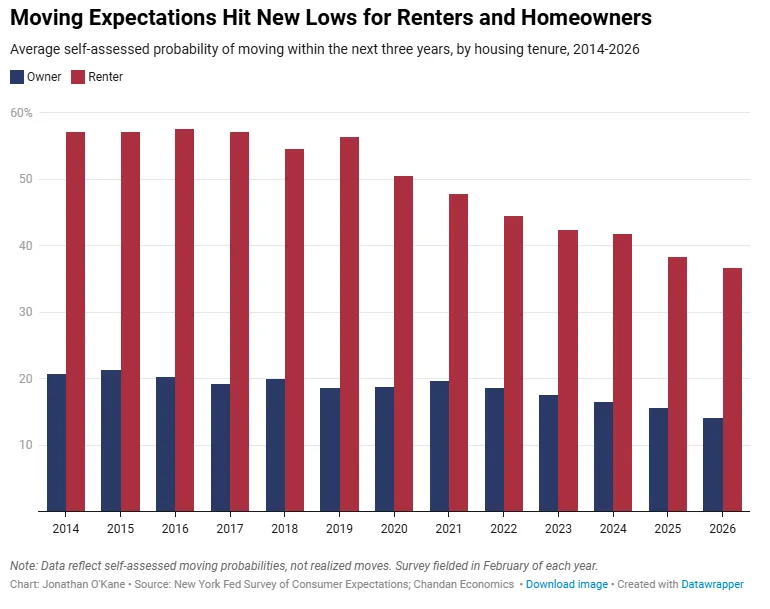

Chandan Economics reports that the US housing market is growing increasingly immobile as fewer households expect to relocate in the years ahead. According to the Federal Reserve Bank of New York’s 2026 Survey of Consumer Expectations Housing Survey, just 21.7% of Americans expect to move within the next three years, the lowest reading since the survey began tracking the metric in 2014.

The decline aligns with broader mobility trends already showing up in the market. Harvard’s Joint Center for Housing Studies reported that just 14.8M US households moved in 2024, representing a record-low mobility rate of 11.2%.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Decade-Long Slowdown

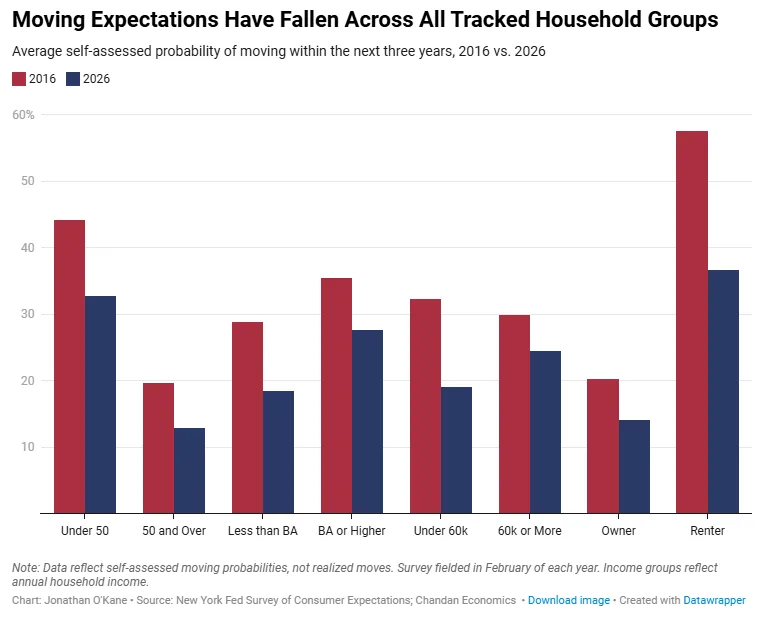

Mobility expectations have steadily deteriorated across nearly every demographic group over the past decade. In the mid-2010s, roughly one-third of Americans expected to move within three years. By 2026, that figure had fallen closer to one in five.

The slowdown is especially pronounced among renters. Renters reported a 36.6% probability of moving within three years in 2026, down from 57.5% in 2016, according to the New York Fed survey. Homeowners also became less mobile, with expected movement falling from 20.2% to 14.1% over the same period.

Younger households continue to show higher mobility than older Americans, but even those under 50 reported sharply lower expectations. Their expected probability of moving fell from 44.1% in 2016 to 32.7% in 2026. Among households age 50 and older, mobility expectations declined from 19.6% to 12.9%.

The Affordability Squeeze

High housing costs appear to be a major driver behind the stay-put trend. Homeowners who locked in historically low mortgage rates during the pandemic now face significantly higher borrowing costs if they move, reinforcing the so-called “mortgage-rate lock-in” effect.

For renters, relocation costs have also climbed. Moving often requires higher market rents, application fees, broker commissions in some cities, moving expenses, and larger security deposits. Those rising costs can make staying in place financially preferable even for households that might otherwise relocate.

Income disparities further illustrate the pressure. Households earning less than $60,000 annually saw expected mobility decline from 32.3% in 2016 to 19.0% in 2026. Higher-income households also pulled back, though less dramatically, falling from 29.9% to 24.5%.

Remote Work Reshapes Relocation Patterns

Remote and hybrid work may also be reducing the need for geographic mobility. While the pandemic initially fueled migration to lower-cost markets, flexible work arrangements now allow many employees to change jobs or maintain employment without relocating.

That shift could have long-term implications for housing demand patterns and regional labor mobility. Historically, job changes often triggered household moves. As remote work weakens that connection, fewer households may feel compelled to relocate for career opportunities.

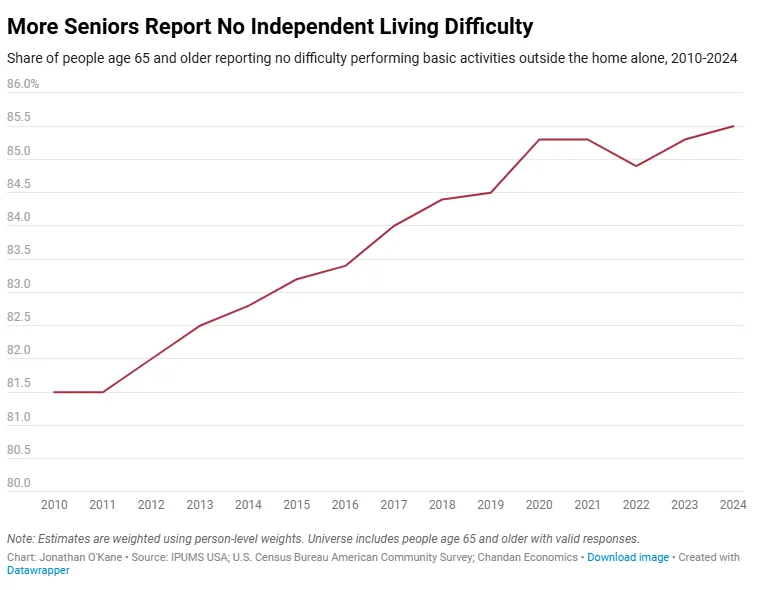

Demographics are adding another layer. Older Americans generally move less frequently, and the aging US population naturally pushes mobility rates lower. According to Chandan Economics’ analysis of 2024 American Community Survey data via IPUMS, 85.5% of Americans age 65 and older reported no difficulty living independently, up from 81.4% in 2010.

Why Lower Housing Mobility Matters

Lower mobility can ripple across the broader commercial and residential real estate landscape. Reduced turnover limits available housing inventory, slows apartment leasing velocity, and can constrain labor-market flexibility if workers remain tied to existing housing situations.

For multifamily owners, lower renter turnover could help stabilize occupancy and reduce leasing costs. But it may also reduce pricing power if fewer households are actively searching for apartments. In the for-sale market, low mobility reinforces inventory shortages that continue to support elevated home prices despite higher mortgage rates. The trend also reinforces broader data showing US household mobility rates fell to historic lows in 2024, tightening housing supply and slowing market turnover across both rental and ownership markets.

Economists also closely monitor mobility because household movement typically supports spending tied to housing transitions, including renovations, furnishings, storage, and moving services.

What’s Next

Housing mobility is unlikely to rebound quickly unless affordability conditions improve materially. Lower mortgage rates could ease lock-in pressures for homeowners, but elevated home prices and limited inventory remain structural constraints in many markets.

At the same time, demographic aging and remote work flexibility are long-term forces that could permanently reduce mobility compared with prior decades. If those trends persist, the US housing market may continue shifting toward longer tenures, lower turnover, and a more structurally “sticky” housing environment.