- Sun Belt metros including Austin, Fort Myers, and Phoenix are seeing declining rents and aggressive concessions as new apartment supply outpaces demand.

- Coastal and Northeast markets such as San Francisco, New York, and parts of Virginia are posting some of the nation’s fastest rent increases amid tighter inventory.

- The growing divide between oversupplied and undersupplied apartment markets is reshaping leasing strategies for renters, owners, and multifamily investors nationwide.

The US apartment market is splitting into two distinct stories this spring. In supply-heavy Sun Belt metros, renters are gaining leverage through lower effective rents and generous concessions, while coastal and Northeast markets are seeing renewed rent growth as supply tightens.

According to Apartments.com’s May 2026 RentPulse Index, markets flooded with new multifamily deliveries are struggling to absorb inventory fast enough, especially across Texas, Florida, and the Carolinas. Meanwhile, cities tied to tech growth and constrained housing supply are seeing some of the steepest rent increases in the country.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Tale of Two Rental Markets

San Francisco posted one of the largest annual rent increases nationwide, with average one-bedroom rents climbing 8.2% year over year to $3,351 per month, according to Apartments.com. The report tied the increase to the region’s AI-driven hiring boom led by firms including OpenAI, Anthropic, and Nvidia.

Rhode Island and Virginia’s Hampton Roads region also saw rents outpace inflation. Norfolk rents rose 4.2% annually, while Virginia Beach and Newport News posted gains above 3%, even as broader consumer prices in the region increased 2.4%, per Bureau of Labor Statistics data cited in the report.

At the other end of the spectrum, Sun Belt apartment markets continue dealing with the aftermath of the post-pandemic construction boom. Texas rents fell 2.1% year over year, with Austin and San Antonio posting the sharpest declines as developers compete to fill new units. Florida rents dropped 1.6%, with Gulf Coast markets including Fort Myers, Sarasota, and Tampa seeing particularly heavy pressure from rising vacancy rates.

The Concessions Race Intensifies

Property owners in oversupplied markets are increasingly relying on concessions to maintain occupancy. Nationally, the average concession rate rose to 2% in 2026, up from 1.8% a year earlier, according to Apartments.com.

Fort Myers led the country with a 5.3% concession rate, meaning renters are paying materially below advertised rents once specials are factored in. Asheville followed at 4.4%, while Denver, Austin, and Phoenix all posted concession rates near or above 4%.

The report suggests these discounts are becoming a key competitive tool as multifamily operators navigate elevated deliveries and slowing migration into formerly high-growth Sun Belt metros. Concessions have also become more widespread nationally as landlords compete to fill a growing number of vacant units across major apartment markets.

Migration Patterns Continue to Evolve

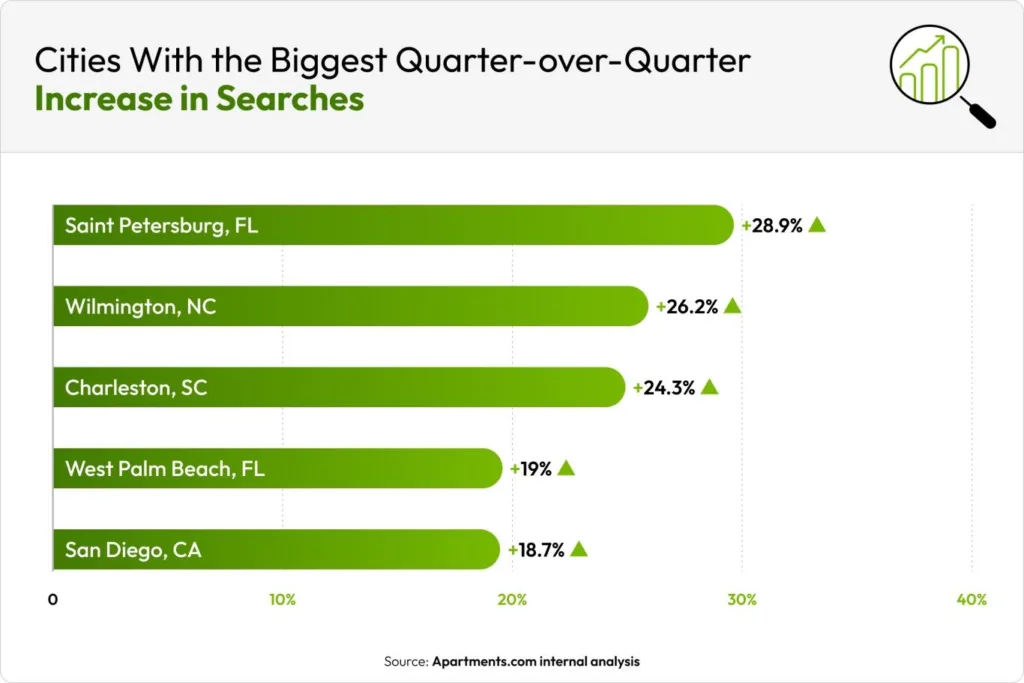

Search activity on Apartments.com shows renters still favoring coastal lifestyle markets despite softer pricing fundamentals. Saint Petersburg, FL, recorded the largest quarter-over-quarter jump in apartment searches at 28.9%, followed by Wilmington, NC, and Charleston, SC.

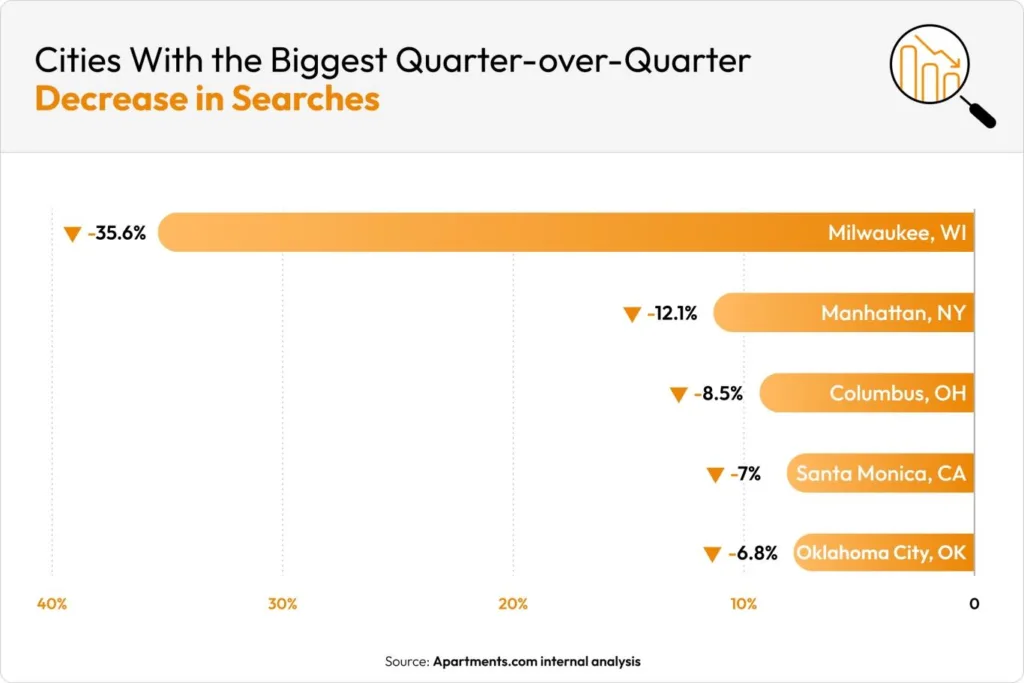

Chicago also emerged as a standout, with searches rising 16% from late 2025 levels. Meanwhile, search activity declined sharply in Milwaukee, Manhattan, and Santa Monica.

CoStar Group analysts linked Milwaukee’s slowdown partly to rising inventory levels after the city absorbed one of its largest apartment supply waves on record in 2025. In Southern California, analysts noted that renters may increasingly view Orange County as a more affordable alternative to Los Angeles as affordability pressures persist.

Affordability Gaps Widen

The national apartment market may appear balanced on paper, but affordability varies dramatically by metro. Apartments.com reported the national average one-bedroom rent consumes roughly 23.3% of median household income, below the standard 30% affordability threshold.

That balance breaks down in major gateway markets. In New York City, the average one-bedroom rent reached $4,104 per month, equal to roughly 69% of the city’s median household income. Miami, Boston, Brooklyn, and Queens also posted rent-to-income ratios above 50%.

By comparison, several Texas and Midwest metros remained relatively affordable despite recent population growth. Austin’s rent-to-income ratio stood at 20.3%, while Kansas City and Columbus each came in near 23%.

Why It Matters

The apartment market’s growing geographic divide is reshaping multifamily investment strategy. Operators in oversupplied Sun Belt metros face mounting pressure on rents, occupancy, and revenue growth, while landlords in supply-constrained coastal markets are regaining pricing power.

The divergence also complicates underwriting assumptions across the sector. Markets that attracted aggressive multifamily development during the pandemic-era migration surge are now seeing softer fundamentals, even as long-term demographic growth remains intact.

For renters, timing and location increasingly matter more than seasonality. In markets with heavy deliveries, negotiating leverage has improved materially. In tighter coastal metros, however, affordability pressures continue intensifying.

What’s Next

Apartment supply pipelines across the Sun Belt remain elevated despite a slowdown from the 2024 construction peak. Apartments.com expects many Southern markets to remain renter-friendly through at least the near term as additional units deliver into already competitive leasing environments.

Investors are also watching several macro risks that could influence apartment demand and operating costs, including rising oil prices, New York City’s proposed rent freeze for stabilized apartments, and the federal ROAD to Housing Act, which would restrict large investors from purchasing single-family homes if enacted.