- Freddie Mac SBL supports a crucial segment of the multifamily lending market with small, geographically diverse loans.

- Over 68% of SBL loans exhibit strong DSCRs at or above 1.4x, appealing to conservative lenders.

- If SBL liquidity wanes, banks, credit unions, debt funds, and private credit would likely step in.

Freddie Mac SBL’s Critical Role

The Freddie Mac Small Balance Loan (SBL) program has long bridged a gap in the multifamily market, targeting smaller loans often overlooked by traditional lenders. Its consistent liquidity and broad national reach have made it central to multifamily financing, especially for smaller properties.

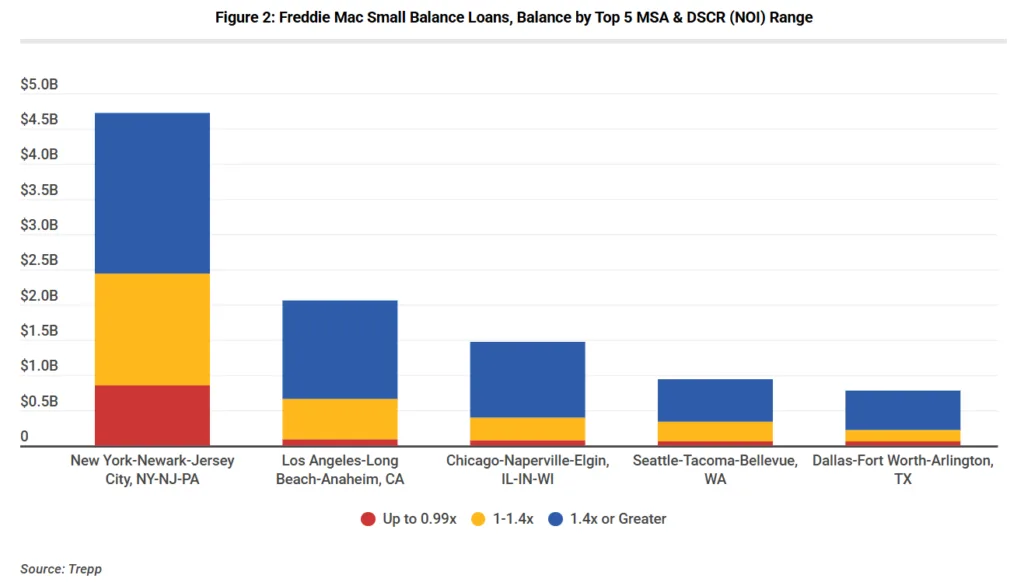

According to Trepp, nearly half of the SBL book matures in ten or more years, providing stability for borrowers and investors. The average loan size is $2.59M, and more than 68% of loans by balance have DSCRs of 1.4x or higher, reinforcing the overall credit strength of the pool.

Potential Successors

Should the SBL program scale back or cease, the underlying loan pool features—solid DSCRs, moderate LTVs, modest average balances, and geographic diversity—make these assets attractive to a broad spectrum of capital providers. Recent data shows that banks and other CRE lenders continue to originate loans with similarly conservative credit metrics, such as a Q4 2025 average multifamily DSCR of 1.57x and LTV of 56.8%, even as some segments of the multifamily market have recently shown rising signs of loan stress and delinquency.

Active participants already include banks, credit unions, debt funds, and private credit platforms, all familiar with the typical loan sizes and profile of the SBL program. The infrastructure is in place for these groups to absorb securitized SBL assets and maintain origination in the segment if GSE support changes.

What’s Next

While Freddie Mac SBL remains a pillar in small loan multifamily finance, its existing loan book performance and buyer interest suggest market resilience. The sector’s attributes—modest, well-distributed balances with strong risk profiles—position it well for continued capital flow, even if the SBL channel narrows. Replacement liquidity is available, supporting ongoing small loan multifamily activity nationwide.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes