- Self storage investment volume reached $5.9B YTD as of November 2025, exceeding 2024’s total and showing investor confidence despite lower transaction counts.

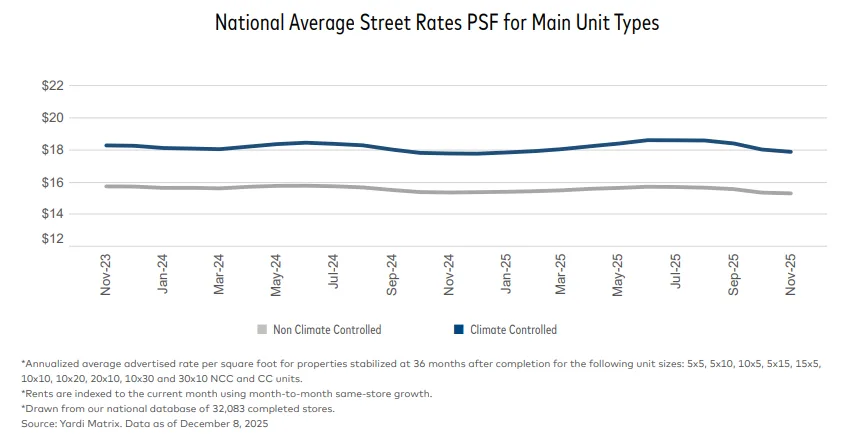

- Rent growth is slowing, with national asking rates rising only 0.6% YoY in November and dropping 0.5% MoM, a steeper seasonal decline than in prior years.

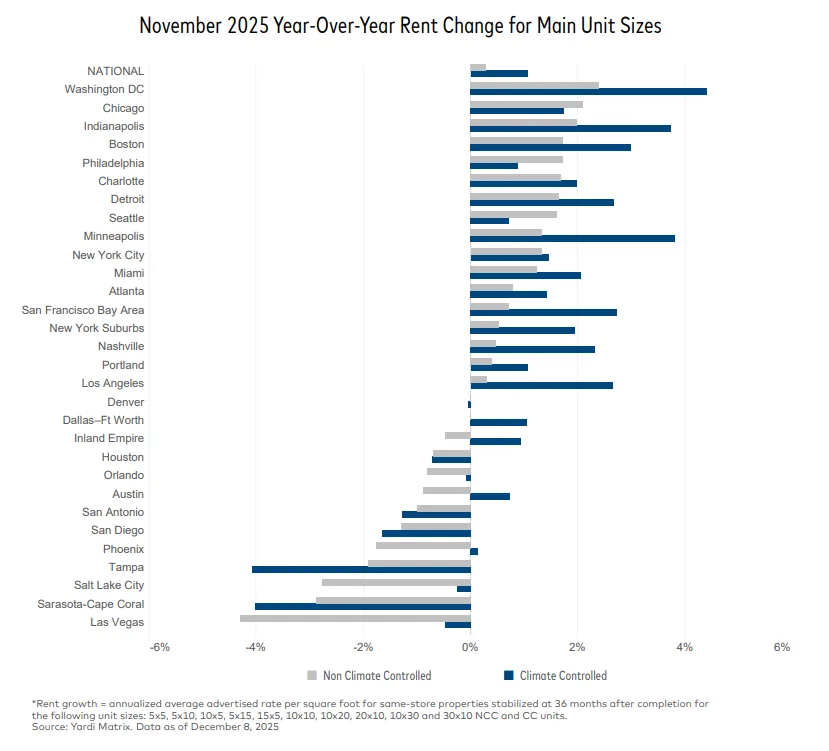

- Markets with manageable new supply like Washington, DC, Indianapolis, and Minneapolis outperformed, while Sun Belt cities including Tampa, Sarasota, and Las Vegas struggled with rent declines due to elevated construction activity.

Investment Confidence Returns

After two sluggish years, the self storage investment market has regained momentum in 2025, reports Yardi Matrix. Transaction volumes have already surpassed 2024 levels. Average sale prices have also increased, reaching $145 PSF, and nearly $200 for Class A properties. Institutional buyers like REITs made up 28% of volume, marking a significant increase in sector participation.

Slowing Rent Growth Nationwide

Rent growth slowed in November, with national average asking rates at $16.38 PSF, up just 0.6% year-over-year. Climate-controlled units outperformed, with 21 of the top 30 metros reporting year-over-year rent growth for CC units.

However, month-over-month performance dipped. In November, 29 out of the top 30 metros posted rate declines. The national average fell 0.5% MoM, a steeper drop than 2024’s -0.3% and the pre-COVID seasonal norm of -0.1%. The only metro to see a gain was Salt Lake City (+0.1%), driven by REIT pricing strategies.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Uneven Market Performance

The rent growth leader was Washington, DC, posting a 3.4% YoY increase. Other top-performing metros include Indianapolis, Minneapolis, Boston, and Detroit, all of which benefit from lower construction pipelines and strong multifamily rent trends.

Sun Belt cities like Sarasota, Tampa, and Las Vegas saw the steepest declines due to aggressive construction and oversupply. These oversupplied markets continue to struggle with rate compression as demand lags behind new deliveries.

Supply Pipeline Holds Steady

Nationwide, 2.6% of self storage inventory is under construction—unchanged from October. While deliveries have slowed in some markets, new supply is not falling as quickly as expected, with 15 of the top 30 metros seeing more lease-up inventory YoY. Sarasota-Cape Coral leads with 20.3% of inventory delivered over the past three years, indicating further pressure ahead.

Why It Matters

Investor interest is rising, but slowing rent growth and oversupply in key metros may limit returns in the near term. Markets with moderate development pipelines and strong demographic trends are better positioned for stable performance in 2026.

What’s Next

The sector appears to be entering a new phase where discipline in development and localized demand drivers will dictate performance. Markets like Washington, DC, and Indianapolis show resilience, while overbuilt regions may need time to absorb excess capacity. With 53.3M net rentable SF still in the pipeline, rent pressure could persist into 2026 unless demand fundamentals improve.