- The US is heading into a senior housing crunch as the 85-plus population is projected to surge to nearly 16M by 2045, while construction pipelines hit decade lows.

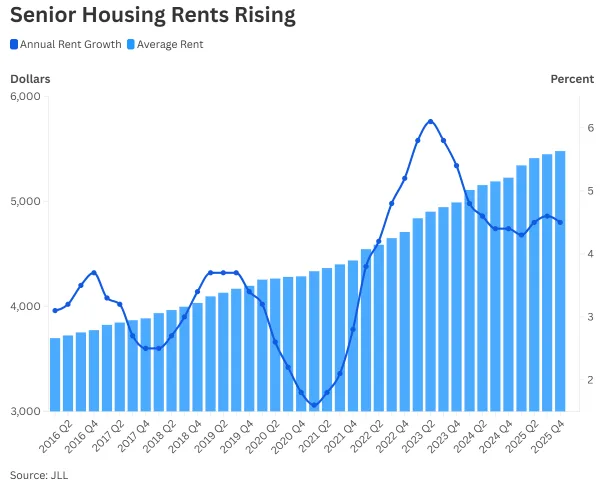

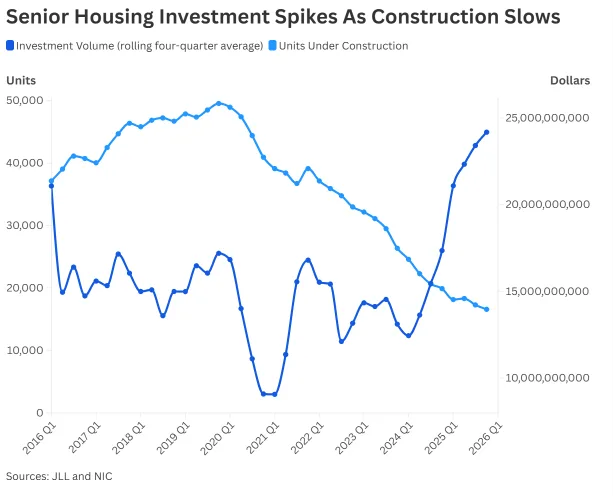

- Average rents for senior housing reached $5,479 per month by Q4 2025, up 28% from 2020, per JLL, even as Wall Street poured $12.1B into the sector in Q1 2026 alone.

- Without expanded supply or alternative models, millions of seniors on limited incomes face the prospect of unaffordable or inaccessible care as developers target higher-end projects for affluent boomers.

Supply Squeeze Pushes Rents Higher

According to Bisnow, the US senior population faces a looming housing shortage as demand for supportive living far outpaces new construction. As the 85-plus age group is expected to grow by 125% to nearly 16 million by 2045, facility pipelines are drying up: only 16,423 units were under construction last quarter, the lowest since 2012 per National Investment Center for Seniors Housing & Care.

High demand and limited supply are already sending prices skyward. JLL reports average monthly rents reached $5,479 by the close of 2025—a 28% jump from late 2020. For many families, even finding a room requires years of waitlisting or paying well above median incomes, underscoring a system leaving millions vulnerable.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Senior housing encompasses a spectrum ranging from independent living for active retirees to memory care and skilled nursing. But even the most basic facilities are becoming unaffordable for much of the population. A 2024 JAMA Internal Medicine study found the average move-in age is 84, often triggered by life-changing events like medical crises.

Construction has stalled as builders face double-digit cost inflation and tightening credit. Per MSCI, investment in the sector hit a quarterly record of $12.1B in early 2026. Demand also continued climbing into 2026, keeping occupancies elevated and reinforcing expectations for further rent gains. Meanwhile, unit deliveries languished at 10,000 for the past year, only a third of the 30,000 units absorbed, according to JLL. Occupancies have bounced back post-pandemic to nearly 89%, but with new supply at a standstill, most developers are focusing on expensive, luxury product targeting high-net-worth seniors.

Barriers to Building and the Forgotten Middle

Surging input costs and challenging capital stacks are driving major developers to chase only the top end of the market. Harrison Street’s focus, for instance, is on supply-constrained, high-income zip codes where rents easily top $10,000 per month. At Calson Management’s upcoming Santa Cruz project, 150 people are on the waitlist for 76 units starting at $10K monthly, plus care fees. While affordable developers leverage tools like the federal LIHTC to deliver subsidized product, waitlists are massive: 1,800 applicants for 110 units at Pinnacle at La Cabaña in Miami shows the scale of unmet need.

The outcome is what the National Investment Center calls the “forgotten middle”: seniors who earn too much for Medicaid but not enough to afford private pay. The average Social Security check ($2,000/month) covers less than half the average rent, and over 17 million seniors are classified as economically insecure per a 2024 National Council on Aging report.

Why It Matters

The shortfall comes as investors flock to senior housing, driving property values and transactions to all-time highs. MSCI data shows nearly $30B in senior properties changed hands in the year to March 2026—almost double the prior 12-month period. Prices have jumped as well: the average per-unit price reached $147,000 in Q1 2026, up 39% in two years and outpacing net operating income.

Yet for the operators and residents, the math is increasingly unsustainable. Rents are projected to rise at 5% annually for the next five years, JLL notes, driven by an unprecedented demand-supply mismatch. The system creates a bifurcated market: wealthy boomers have expanding options, while tens of millions with modest or fixed incomes find themselves priced out, forced to delay moves until health deteriorates or live with family when that’s not an option.

Industry leaders and policy experts warn that without a source of new, cost-effective supply—whether through expanded LIHTC, innovative infill projects, or alt models like accessory dwelling units—the US faces a generational welfare risk with real destabilizing potential for families, hospitals, and local governments alike.

What’s Next

Despite robust investor appetite, meaningful new construction is unlikely to relieve the crunch quickly. Brookdale Senior Living CEO Nick Stengle suggests nationwide rents would need to jump 30%–40% for projects to pencil. Even when developers break ground, entitlement and build timelines can stretch up to seven years—far longer than traditional multifamily cycles.

In response, some investors are seeking ways to retrofit existing residential stock for seniors or back alternative models in urban infill and walkable neighborhoods. Others are betting the continued imbalance will keep driving up asset values. Without policy expansion or industry innovation, however, supply will remain constrained for years—leaving millions of aging Americans scrambling for care and shelter as a once-in-a-century boom gets underway.