- Retail traffic is rebounding as consumers respond to value-driven promotions and fewer tariff-related concerns, showing renewed spending confidence.

- Manufacturing and port activity have declined in May and June after an early-year production surge, suggesting companies are growing cautious about the second half of 2025.

- The split between strong retail trends and slowing industrial output reflects a two-speed economy, creating uncertainty around supply chains and future growth.

Two Economies, One Midyear Story

As the US economy hits the halfway mark of 2025, two contrasting stories are playing out, reports The Anchor. On one hand, consumers are back in stores and responding well to seasonal promotions. On the other, manufacturers and port operators are seeing a decline in activity after ramping up earlier in the year to get ahead of tariff risks. The result is a growing divergence that could shape the trajectory of the broader economy through year-end.

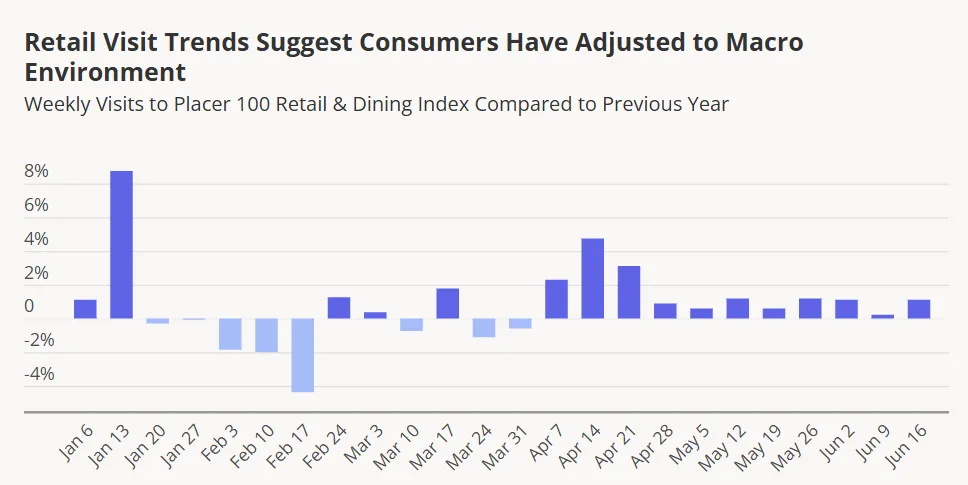

Retail Rebounds, Driven By Value And Promotions

Consumer-facing sectors saw a marked rebound in May and June, bouncing back from sluggish Q1 performance. Year-over-year foot traffic data from the Placer 100 index shows stabilization across major retailers, signaling a return to more predictable consumer behavior.

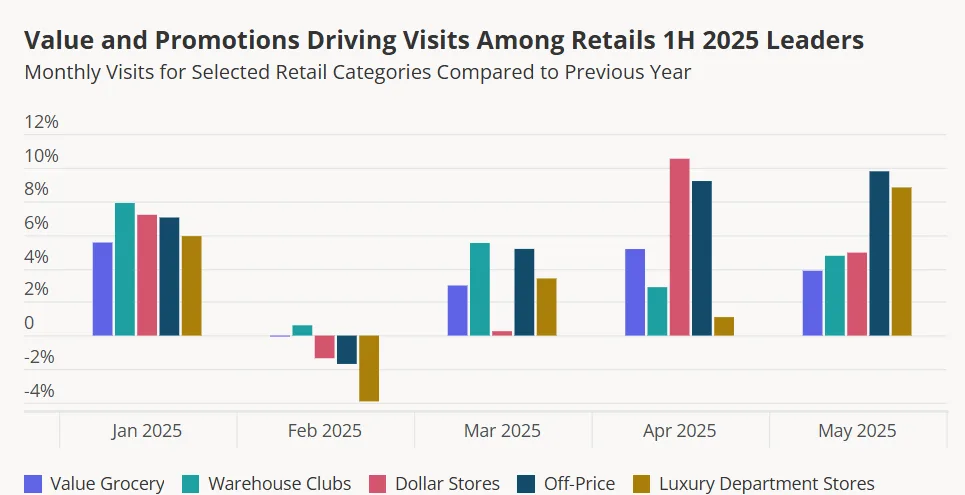

The strongest gains have come from value-driven segments:

- Warehouse clubs and dollar stores are benefitting from renewed interest in discount shopping and less pricing pressure from global fast-fashion competitors like Temu and Shein, due to regulatory shifts.

- Off-price retailers are thriving thanks to inventory windfalls from earlier supply chain disruptions.

- Department stores are seeing renewed foot traffic from successful events like Nordstrom’s Half-Yearly Sale, highlighting the power of promotions in today’s market.

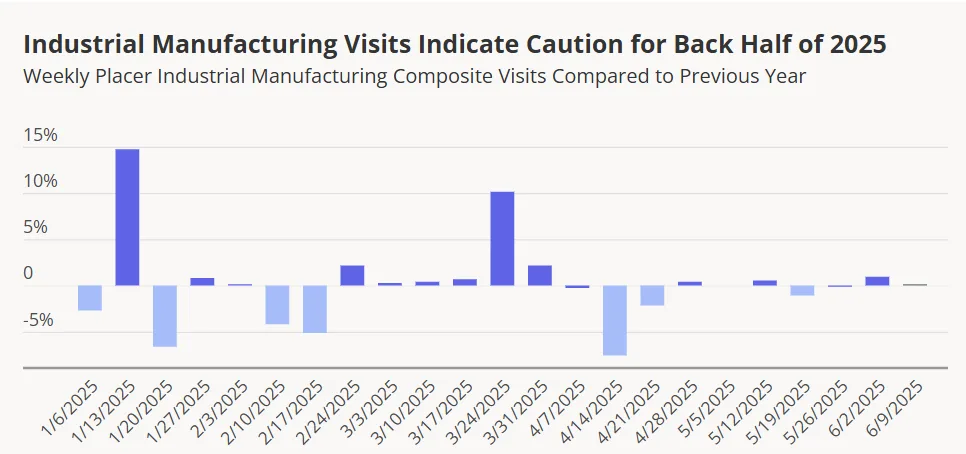

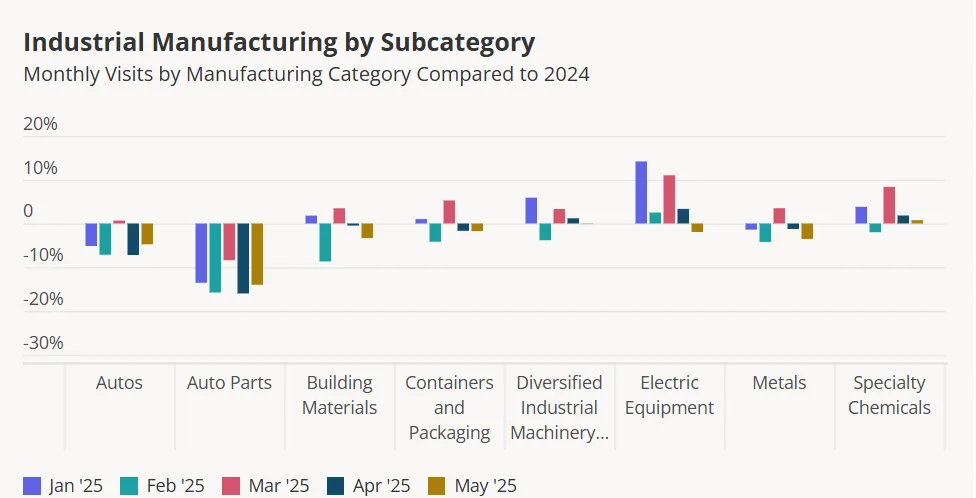

Industrial Sector Slows After Early Surge

While consumers are warming up to shopping again, US manufacturing is cooling down. After aggressively building inventory in March and April ahead of expected tariff actions, factories have eased back.

Placer’s Industrial Manufacturing composite data shows:

- Slower foot traffic across most manufacturing facilities since May.

- Sharp declines in automotive-related manufacturing visits due to international trade pressures.

- Broad pullback across other sectors, indicating a wait-and-see stance amid ongoing economic uncertainty.

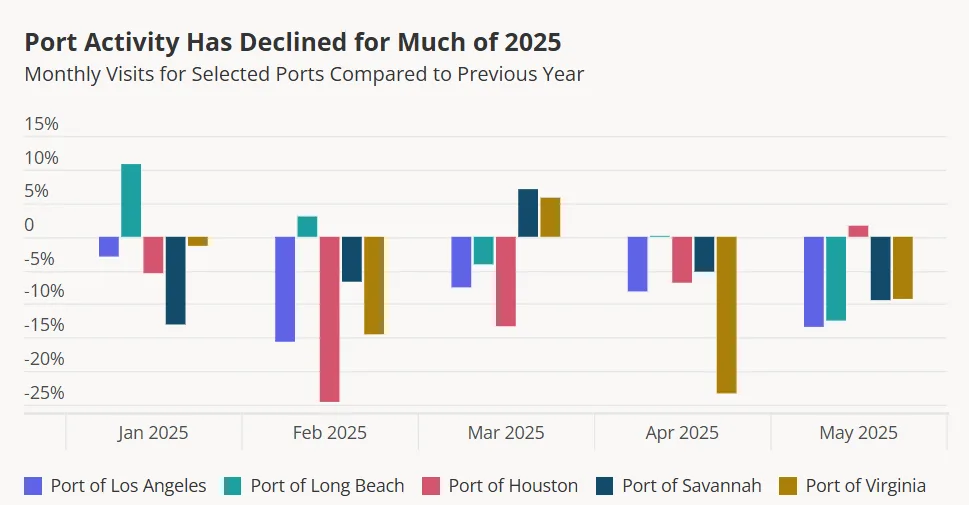

Port Activity Softens—With One Notable Exception

Port operations are also following the industrial cooldown, reinforcing the two-speed economy emerging. After a spike in early spring tied to inventory front-loading, visitation trends at major US ports have steadily declined. The exception is the Port of Houston, which saw increased activity in May and June tied to fuel-related imports.

Slowing container volumes and fewer new orders suggest businesses are hesitant to commit to future shipments, wary of overextending amid policy unpredictability.

Economic Tug-Of-War Ahead

The second half of 2025 begins with a mixed economic outlook:

- Consumer resilience could continue driving retail gains.

- Industrial caution may lead to tighter supply chains and delayed investment.

The key question: Can strong consumer demand pull the manufacturing sector back into growth, or will an extended industrial slowdown limit retail momentum and broader economic expansion?

Bottom Line

The US economy is walking a tightrope at midyear. With retail on the rise and manufacturing taking a step back, the second half of 2025 will hinge on whether consumer strength can offset industrial hesitation—or whether one side of the economy will eventually pull the other down.