- Lenders are channeling capital to core and core-plus multifamily assets with stable cash flow, as indicated by Berkadia’s mid-year 2026 report.

- Agency lenders like Fannie Mae and Freddie Mac continue disciplined underwriting, while debt funds and life companies tighten pricing and scrutiny on complex deals.

- The flight to quality is narrowing the market, concentrating investment and financing on predictable, execution-ready properties.

Lending Rebounds, With a Focus on Quality

Multifamily lending is picking up in 2026, but the surge isn’t across the board. According to Berkadia’s mid-year market report, the action is focused on higher-quality, core and core-plus properties as capital sources target deals with stable income and predictable execution. Borrowers seeking financing for other asset classes or more complex structures are finding a cooler reception, as lenders become less concerned about capital availability and more selective about where it lands.

Stability Over Aggression Defines This Cycle

Behind this shift is lender wariness about market volatility and uncertain deal outcomes. Agency lenders Fannie Mae and Freddie Mac are increasing originations while maintaining strict underwriting standards for resilient properties.

Non-bank lenders, including debt funds and insurance companies, are taking a cautious approach. They often demand higher premiums for more complex deals. Some are also adjusting pricing late in the process to favor certainty and straightforward execution. In the current climate, execution risk determines both cost and access to capital.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Flight to Quality Reshapes Sales and Pricing

The same themes shaping multifamily lending are influencing investment sales activity. Buyers remain active, but they are concentrating capital on higher-quality assets and underwriting acquisitions with more conservative assumptions.

Rather than relying on aggressive rent growth projections, investors are prioritizing stable income streams and operational durability. That approach reflects a market still navigating economic uncertainty and interest-rate volatility, even as financing conditions improve.

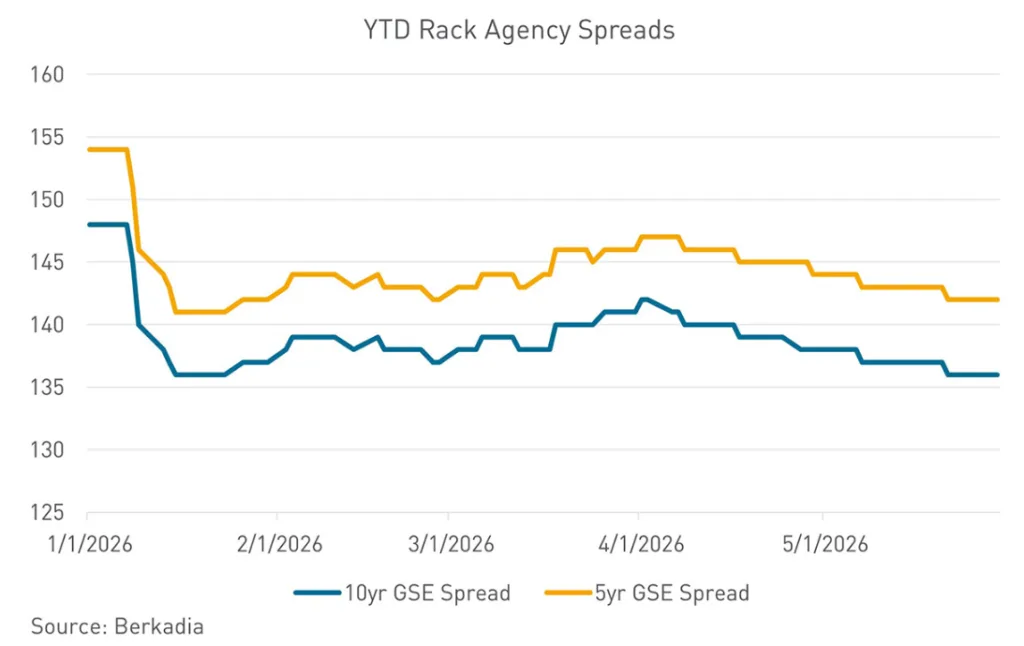

Interest-rate swings earlier in 2026 temporarily widened lending spreads, according to Berkadia. Those spreads have since tightened as investor demand outpaced available deal flow. Standardized transactions continue to attract the most competitive financing, while deals involving complex structures, operational challenges, or execution uncertainty require additional negotiation and often carry higher costs.

The trend suggests that both lenders and buyers are evaluating opportunities through a similar lens, favoring predictability over potential upside.

Why It Matters

The return of liquidity is an important development for multifamily owners and investors, but Berkadia’s report highlights a more nuanced reality. Capital availability has improved, yet access to the most attractive financing remains concentrated among the strongest assets and sponsors.

That distinction matters because multifamily has been one of commercial real estate’s most closely watched sectors during the industry’s broader repricing cycle. As lenders regain confidence, they are not reopening the market equally across all property types and investment strategies. Instead, they are directing capital toward transactions that offer greater visibility into performance and repayment.

The trend is also influencing larger-scale investment activity. Berkadia pointed to continued institutional interest in portfolio transactions, including the widely watched $1.6B Camden, California, apartment portfolio. Public apartment owners such as AvalonBay Communities and Equity Residential are likewise pursuing consolidation strategies aimed at improving operating efficiencies and strengthening scale.

What’s Next

Berkadia expects liquidity to remain healthy through the remainder of 2026, supported by active agency programs, insurance company allocations, and continued debt fund participation. However, the report suggests lenders are unlikely to abandon their disciplined approach anytime soon.

If interest-rate volatility remains contained and investor demand continues to exceed available opportunities, financing conditions could improve further for core multifamily assets. Yet borrowers pursuing value-add, transitional, or highly structured transactions may continue to face pricing pressure and heightened scrutiny.