- Single-tenant net lease investment sales reached $51.4B in 2025, with fourth-quarter activity jumping 39.1% quarter-over-quarter, according to Northmarq and Real Capital Analytics.

- Industrial properties remained the dominant asset class, but office gained market share as investors adjusted to higher cap rates and shifting pricing expectations.

- Private capital became the market’s largest buyer group in 2025, while REIT participation dropped sharply amid elevated borrowing costs and ongoing sector uncertainty.

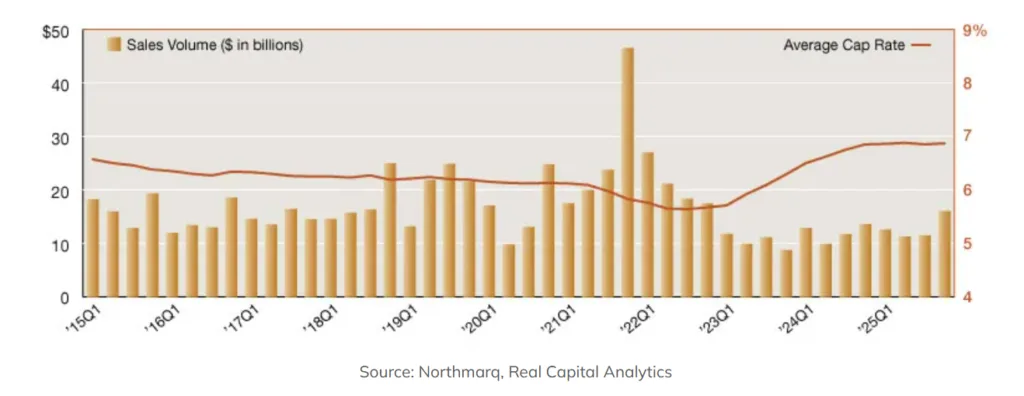

The Commercial Property Executive reports that single-tenant net lease investment sales regained momentum at the end of 2025 after a sluggish start to the year. According to Northmarq and Real Capital Analytics, fourth-quarter transaction volume climbed to $16B, bringing full-year sales to $51.4B. The rebound marked a 12.8% increase from 2024 and suggested investors were becoming more comfortable with stabilized pricing and higher-for-longer interest rates.

While activity improved in the back half of the year, the market spent much of 2025 working through elevated financing costs, valuation resets, and uneven buyer demand across property types. Cap rates continued to rise modestly throughout the year before leveling off in the fourth quarter.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Volatile Year For Net Lease Investment Sales

The market opened 2025 with one of its weakest first quarters in recent memory. First-quarter single-tenant sales volume totaled just $9.4B, down 30% from Q4 2024, according to Northmarq. Investors remained cautious as debt costs stayed elevated and uncertainty around interest rates weighed on underwriting.

Conditions worsened slightly in the second quarter, when transaction volume slipped to $9.6B, the second-lowest quarterly total in more than a decade. Northmarq noted that without a stronger second half, annual sales activity was on pace to trail both 2023 and 2024.

Momentum began to stabilize in the third quarter despite another quarterly decline to $9.9B. By year-end, however, a sharp jump in fourth-quarter activity helped reverse the slowdown and pushed annual totals back into growth territory.

The Details

Industrial assets remained the largest segment of the single-tenant net lease market throughout 2025. The sector accounted for $8.8B in fourth-quarter volume and represented 55.2% of annual activity, though that share declined from 61.2% a year earlier.

Office properties regained some footing during the year despite ongoing sector headwinds. Office transaction volume reached $3.8B in Q4, accounting for 24% of total sales volume, up from 18.3% in 2024. Retail properties totaled $3.3B during the quarter and maintained roughly one-fifth of overall market share.

Cap rates largely stabilized by year-end after several quarters of steady expansion. Northmarq reported the average single-tenant cap rate reached 6.87% in Q4 2025, up just 5 basis points year-over-year. Earlier in the year, cap rates climbed as high as 6.93%, roughly 130 basis points above the market low recorded in Q3 2022.

Private Capital Takes The Lead

One of the clearest shifts in 2025 was the growing dominance of private buyers. Private investors accounted for 53% of single-tenant acquisition volume through year-end, up from 43% in 2024.

Institutional investors also modestly increased their presence, representing 20% of annual acquisition volume versus 17% the prior year. Private buyers also continued favoring retail assets as pricing reset across the sector. REITs moved in the opposite direction. Listed and REIT buyers accounted for just 8% of transaction volume in 2025, down sharply from 17% in 2024.

The retreat was especially pronounced in office. During the first quarter, REITs were entirely absent from the single-tenant office segment, underscoring the continued challenges facing the sector even as transaction activity improved later in the year.

International investors also pulled back. According to Northmarq, foreign buyers represented just 5% of the buyer pool during the first half of 2025, with most targeting retail assets over office or industrial properties.

Cap Rate Recalibration Continues

The single-tenant net lease sector spent much of 2025 repricing assets around higher financing costs. Northmarq described the steady cap rate increases as part of a broader “recalibration of asset valuations” tied to elevated interest rates.

That adjustment appeared most visible in office and retail properties. Office recorded the largest year-over-year cap rate increase by the fourth quarter, while retail posted the biggest increase earlier in the year during Q3.

At the same time, industrial assets continued attracting the deepest buyer demand despite slower volume growth. The sector’s long-term lease structures and tenant-credit profile remained attractive to investors seeking defensive cash flow in a volatile rate environment.

Why It Matters

The 2025 rebound suggests the single-tenant net lease market may be finding a new equilibrium after two years of pricing disruption. Investors appear increasingly willing to transact at higher cap rates as expectations around interest rates stabilize.

The market’s buyer composition also signals a shift in who is driving activity. Private capital has stepped into the gap left by REITs and more cautious institutional investors, particularly in smaller and mid-sized transactions.

That transition could reshape pricing dynamics across the sector, especially if borrowing costs remain elevated through 2026.

What’s Next

Investors will be watching whether fourth-quarter momentum carries into 2026 or proves temporary. Future transaction volume will likely depend on the pace of interest-rate cuts, debt market liquidity, and tenant-credit performance across office and retail assets.

Northmarq expects cap rates to remain under modest upward pressure until financing conditions improve more meaningfully. Still, stabilizing valuations and renewed buyer activity suggest the single-tenant net lease market may be entering a more normalized investment cycle after several years of volatility.