- National self storage rents fell 1.8% year-over-year in May 2026, but the rate of decline is slowing, according to Yardi Matrix.

- Oversupply remains a challenge, with roughly 2.2% of existing inventory still under construction nationwide and Sun Belt metros facing the most pressure.

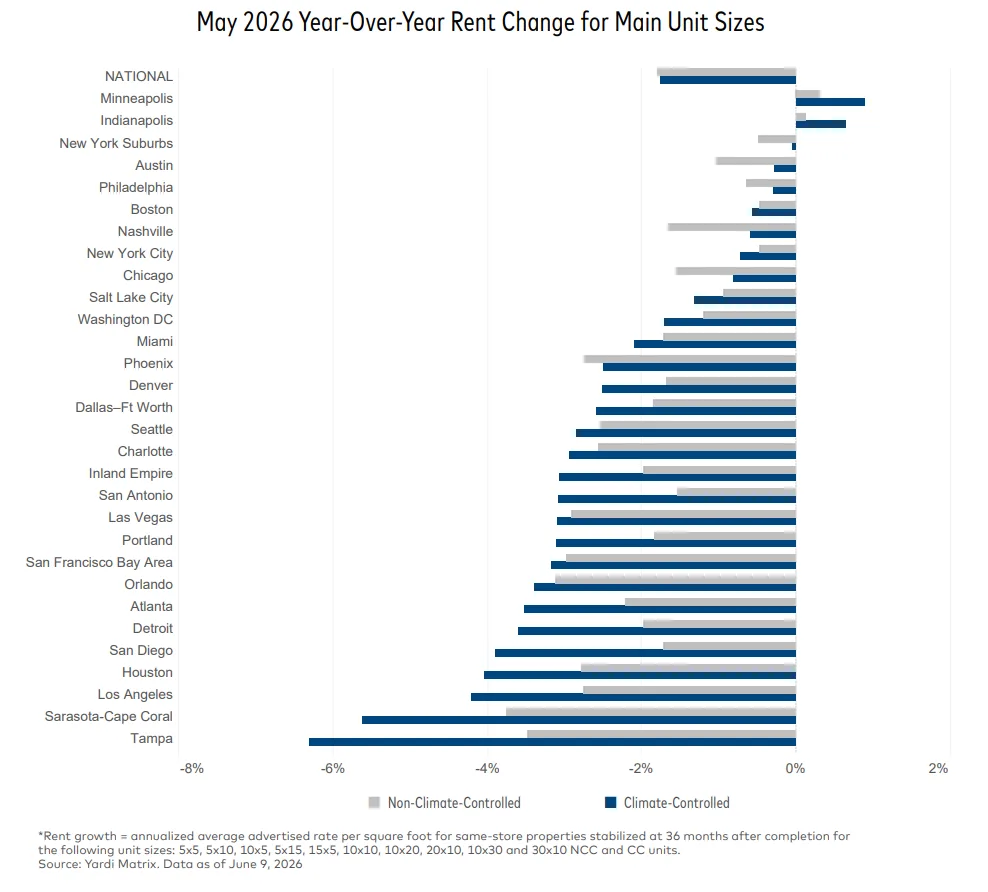

- Recovery is uneven across markets, with only Minneapolis and Indianapolis posting positive annual rent growth among major metros, signaling a prolonged stabilization period ahead.

Texas Serves as a Bellwether for Self Storage Recovery

According to Yardi Matrix’s June 2026 Self Storage National Report, Texas, home to the country’s two largest self storage markets, exemplifies the post-pandemic boom and subsequent reset. In 2021 and 2022, explosive in-migration and record home sales in Austin, Dallas, and San Antonio sent self storage performance to all-time highs. Developers quickly responded, leading to a pipeline surge in growth corridors.

But by 2024, transaction activity and home sales tumbled, and many Texas metros—along with other fast-growing regions—were left competing for a shrinking pool of renters. Advertised rates in Texas dropped 2.5% year-over-year in May 2026 and are now 13.3% below their 2022 peak. Consolidation trends also accelerated, with large operators and REITs acquiring smaller facilities to build scale and operational efficiency during the downturn.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

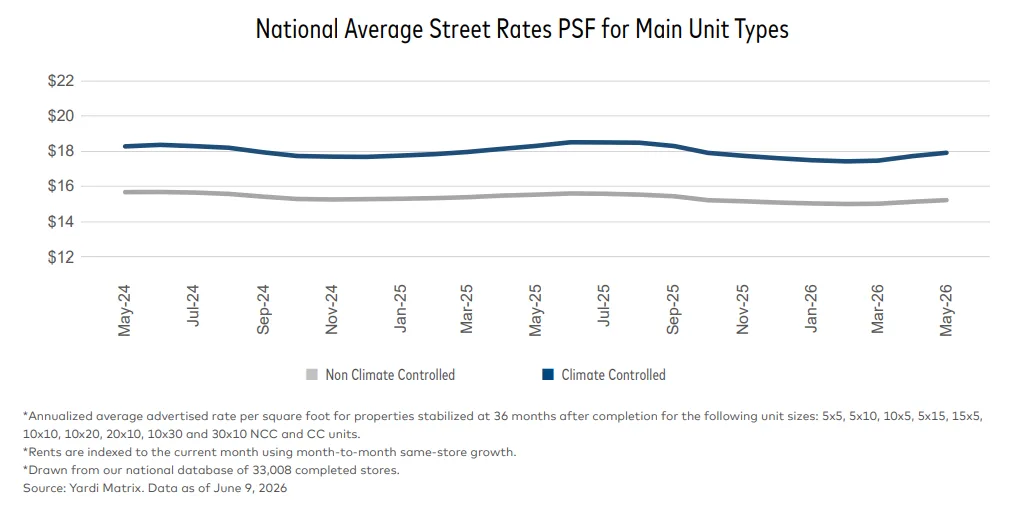

Nationally, Yardi Matrix reported average self-storage advertised rates of $16.34 PSF in May. Rates fell 1.8% year over year. However, conditions improved slightly from April’s 1.9% decline and March’s 2.0% drop. Climate-controlled and non-climate-controlled units each declined 1.8%. Meanwhile, monthly rent growth showed early momentum. Rates increased 0.8% in May, exceeding gains recorded during the same month in 2025 and 2024.

REITs led the monthly rebound through seasonal pricing strategies. However, their national rents remained 3.1% below May 2025 levels. This gap shows seasonality, not stronger demand, drove recent gains. Meanwhile, 2.2% of national inventory remained under construction, or about 45.6M SF. That figure stayed unchanged from April. Yardi tracks 2,513 properties under development and 33,008 completed US facilities.

Sun Belt and Florida Supply Keeps Recovery Uneven

New supply continues to limit rent growth across many metros. Yardi’s June 2026 data shows Sarasota–Cape Coral, Orlando, Tampa, and Las Vegas added the most inventory. Those markets expanded supply by 17% to 23% over three years. They also posted the sharpest rent declines. Tampa rents dropped 5.1% year over year, while Sarasota–Cape Coral fell 4.8%.

By contrast, markets with limited development performed better. Minneapolis added 3.9% net new supply, while Indianapolis added 4.5%. They were the only top 30 metros with positive annual rent growth. Minneapolis gained 0.6%, and Indianapolis rose 0.4%.

Nationally, deliveries reached 9.0% of starting inventory over the past three years. However, construction has slowed recently. New supply delivered during the past year measured 2.4%, down from 3.1% a year earlier. Even so, localized building surges continue to pressure rents across many Sun Belt submarkets.

Why It Matters

These trends are reshaping underwriting, acquisitions, and asset management. Annual rent declines are slowing, but demand has not fully recovered. That shift shows how quickly fundamentals changed after pandemic-driven demand faded. Heavy construction, especially across the Sun Belt and Florida, created lasting oversupply. As a result, rent growth and property values remain under pressure.

Yardi Matrix reports the largest development pipelines in Phoenix, Sarasota–Cape Coral, and Orlando. Active projects equal 6.7%, 5.2%, and 4.9% of existing inventory, respectively. Markets that built aggressively now face longer absorption periods before fundamentals improve. That trend extends the broader slowdown that has defined the self-storage sector since early 2026, even as construction activity begins to cool. Meanwhile, REITs and large operators continue acquiring smaller portfolios. However, weaker rents make it harder for new investors to support recent valuations and projections.

Developers face another challenge. Projects now average more than 550 days from planning to completion. Many began during peak rental conditions but entered weaker markets. That mismatch extends lease-up periods and delays recovery. Only two major metros posted annual rent growth, while 28 recorded declines. Therefore, self-storage conditions remain challenging across most US markets.

What’s Next

Supply moderation should gradually stabilize the sector. However, recovery will vary by market. Yardi Matrix expects shrinking development pipelines to support some metros first. Meanwhile, Sun Belt and Florida markets will likely face longer periods of competition and rent pressure as new space absorbs.

National rent trends should follow the same pattern through 2026. Seasonal pricing may support modest monthly gains. However, stronger annual growth will depend on housing turnover, migration, and consumer confidence. Investors and operators should expect uneven performance through at least 2027. Consolidation and operational efficiency will remain priorities. Markets with limited new supply could return to modest rent growth sooner.