- Self-storage construction starts fell sharply in early 2026, with Q1 starts running 29% below year-ago levels, according to Yardi Matrix.

- The sector’s under-construction, planned, and prospective pipelines all contracted in Q1, while deferred and abandoned projects continued climbing.

- Yardi Matrix forecasts new supply will decline to roughly 1.7% of existing stock by 2028, signaling a much slower development cycle ahead.

Self-storage developers are easing off the gas after years of aggressive expansion. According to Yardi Matrix’s Q2 2026 Self Storage Supply Forecast Update, construction starts, planned projects, and prospective pipelines all declined in Q1 as elevated interest rates and oversupplied Sun Belt markets continued to pressure the sector.

While Yardi Matrix slightly increased its supply forecast to account for 30 newly tracked markets, the broader outlook remains unchanged: self-storage supply growth is expected to slow materially through 2028 before stabilizing at lower levels.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Development Cycle Cools

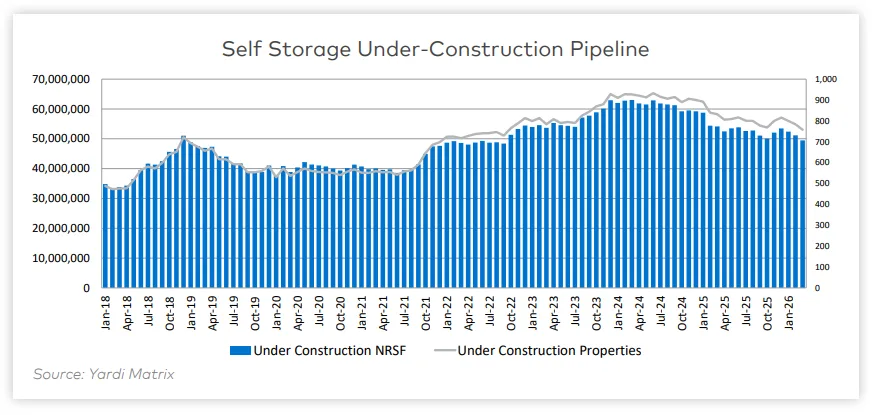

The self-storage boom that peaked in 2022 and 2023 is clearly losing momentum. Yardi Matrix reported the under-construction pipeline fell 14.5% year over year to 50.26M net rentable square feet (NRSF) by the end of Q1 2026. Planned pipeline activity also dropped 14.1% annually, while the prospective pipeline has fallen more than 42% since its October 2023 peak.

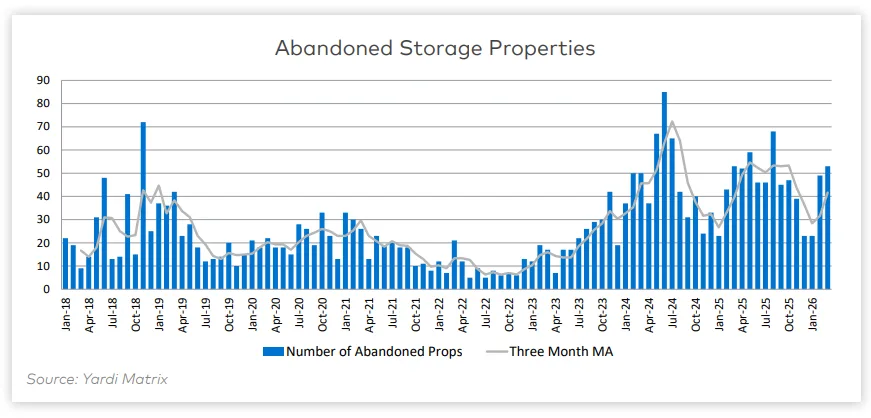

At the same time, more projects are stalling out entirely. Deferred projects climbed 49% year over year to 7.18M NRSF, while abandoned developments remained elevated throughout Q1. In March alone, 53 projects were categorized as abandoned, well above the averages recorded during the prior development cycle.

The Details

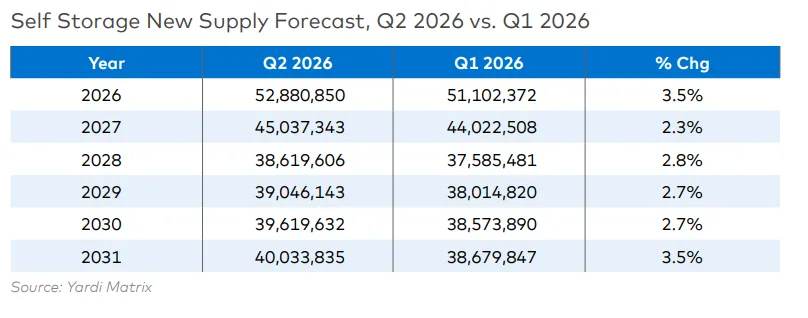

Yardi Matrix now forecasts 52.88M NRSF of new self-storage supply deliveries in 2026, followed by 45.04M NRSF in 2027 and 38.62M NRSF in 2028. The revisions represent a 2.3% to 3.5% increase from the prior quarter’s forecast due primarily to expanded market coverage rather than renewed development activity.

Construction starts are weakening more meaningfully. Yardi Matrix identified 5.12M NRSF of construction starts in Q1 2026, approximately 29% below the same period a year earlier. Developers are also taking longer to move projects through the pipeline, with a growing share of planned projects sitting inactive for more than two years.

Operating fundamentals remain weak. Advertised rental rates face pressure across oversupplied Sun Belt markets. Elevated mortgage rates also continue slowing home sales. Home sales historically drive self-storage demand.

Sun Belt Oversupply Weighs on the Sector

The slowdown is particularly notable in markets that saw heavy pandemic-era development. Sun Belt metros absorbed a wave of new inventory over the last several years. Many operators are still working through excess supply. According to Yardi Matrix, weak NOI growth and elevated cap rates are making projects harder to pencil. That pressure has steadily reshaped development expectations across the self-storage sector, especially as financing costs remain elevated.

The financing environment is also reshaping developer behavior. Higher long-term interest rates continue raising borrowing costs and reducing property valuations, limiting both transaction volume and speculative development activity across the sector.

Why It Matters

The self-storage sector is transitioning from rapid expansion to a more disciplined development phase. While oversupply remains an issue in several markets, the pullback in starts and shrinking pipelines suggest the industry may finally be moving toward a healthier supply-demand balance.

That matters for operators and investors watching occupancy and rent growth trends. Slower supply growth could eventually support pricing power again, particularly in markets that absorb excess inventory faster than expected. But the adjustment period may take several years as projects already under construction continue delivering into 2026 and 2027.

What’s Next

Yardi Matrix expects new self-storage supply to bottom out in 2028 at roughly 1.72% of existing stock before modestly increasing again through 2031. Even then, projected deliveries remain well below the peaks reached during the previous development cycle.

The next key indicator will be whether construction starts continue falling throughout 2026. If interest rates remain elevated and rental rate growth stays muted, developers could retreat even further, accelerating the sector’s shift from expansion to stabilization.