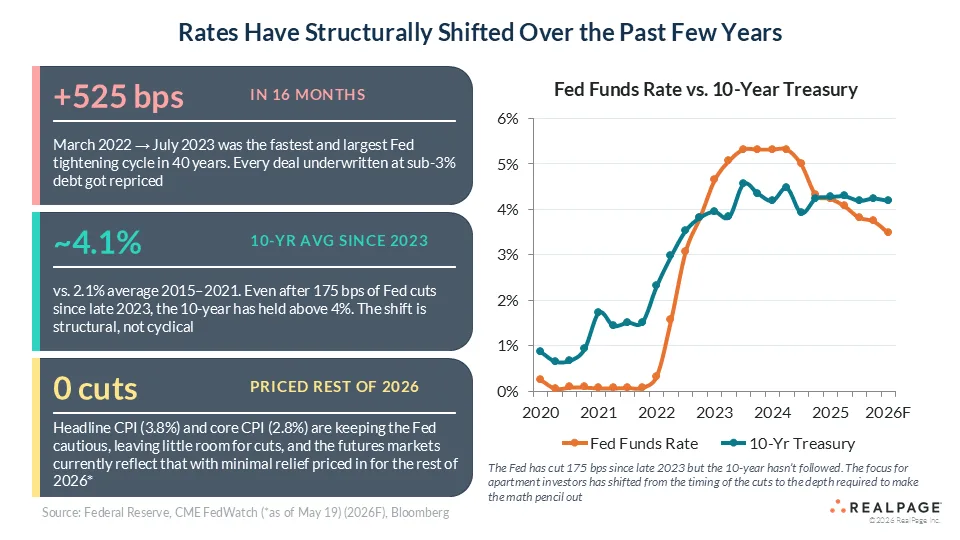

- The Federal Reserve’s 525-basis-point hiking cycle reset multifamily deal economics, making many low-rate-era acquisitions difficult to refinance or trade.

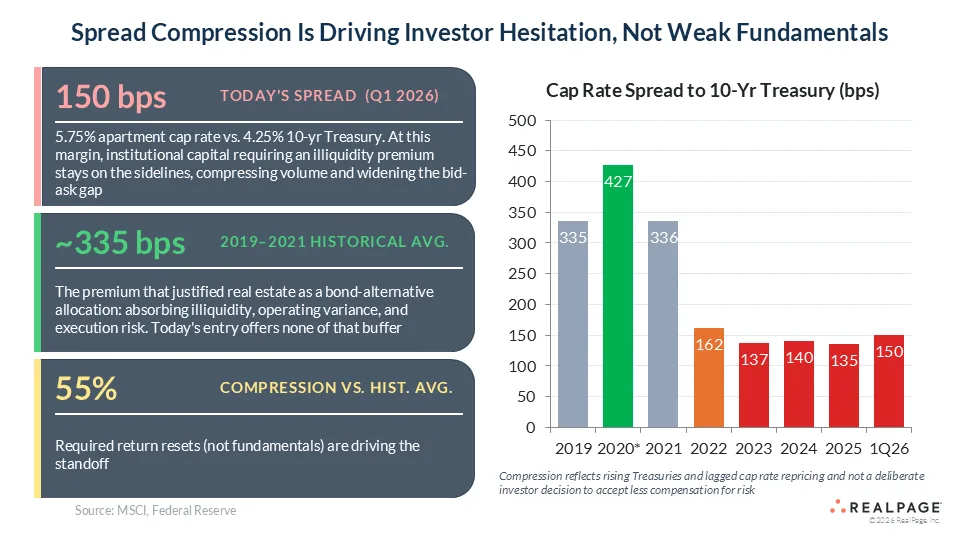

- Apartment cap rate spreads over the 10-year Treasury have narrowed sharply since 2021, reducing the risk premium institutional investors expect from CRE.

- The pricing gap between buyers and sellers continues to slow transaction volume, with loan maturities and capital pressures likely to drive the next market reset.

According to RealPage, the multifamily capital markets landscape continues to adjust to a dramatically different interest rate environment than the one investors enjoyed for most of the past decade. After years of ultra-cheap debt fueled apartment acquisitions and record valuations, higher borrowing costs are forcing buyers, lenders, and sellers to rethink pricing assumptions and return expectations.

Between March 2022 and July 2023, the Federal Reserve raised the federal funds rate by 525 basis points, marking the fastest tightening cycle in more than 40 years. Although the Fed has since reduced rates by 175 basis points, long-term borrowing costs remain elevated and continue to pressure multifamily valuations.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Historic Reset for Multifamily Financing

The sharp increase in rates effectively rewrote the underwriting math for apartment investors. Deals structured when agency debt carried sub-3% interest rates suddenly faced refinancing costs well above original projections, putting pressure on debt-service coverage ratios and leveraged returns.

The 10-year Treasury yield has stayed above 4% throughout 2026, according to the source material. That remains well above the 2.1% average recorded between 2015 and 2021. Meanwhile, forward markets expect little additional rate relief through the rest of 2026. April 2026 CPI reached 3.8%, which strengthened expectations for higher long-term rates.

The Details

The most immediate impact has shown up in cap rate spreads. Between 2019 and 2021, apartment cap rates traded roughly 335 basis points above the 10-year Treasury, providing investors with a meaningful premium over risk-free government bonds. By early 2026, that spread had narrowed to approximately 150 basis points.

That compression has materially changed institutional investment strategies. While apartment fundamentals remain relatively stable, supported by healthy occupancy levels, moderating rent growth, and slowing new supply, many investors no longer view current pricing as adequately compensating for operational risk and illiquidity.

The result is a growing disconnect between buyers and sellers. Owners continue to anchor pricing expectations to 2021 peak valuations, while buyers underwrite to today’s financing costs and lower leveraged returns. That gap has slowed transaction activity across the multifamily sector.

A Slower Multifamily Investment Market

The apartment sector is not alone in facing higher-rate pressure, but multifamily has remained more resilient than office assets. According to CBRE and JLL commentary from 2025 and 2026, institutional capital still favors housing assets despite slower deal volume. Industrial assets have also shown stronger lender confidence as yield spreads stabilized in 2025.

Aggressive cap rate compression has largely disappeared. Investors now focus on durable cash flow and operational efficiency. They also prefer fixed-rate debt over speculative rent growth assumptions. Those assumptions fueled pricing during the low-rate cycle.

Meanwhile, lenders have tightened underwriting standards. Debt providers now examine leverage, reserves, and sponsor experience more closely. Rising refinancing risk across maturing multifamily loans continues to drive that caution.

Why It Matters

Higher interest rates have fundamentally altered multifamily capital markets by reducing the spread between apartment yields and safer fixed-income investments. That narrower premium makes it harder for institutional investors to justify acquiring stabilized multifamily assets at historically high valuations.

The impact extends beyond transaction volume. Refinancing pressure could increase distress among owners who acquired properties with floating-rate debt or aggressive underwriting assumptions during the 2020–2022 cycle. At the same time, long-term investors with available capital may find opportunities as pricing gradually resets.

For multifamily operators, elevated rates also influence development pipelines. Higher construction financing costs and stricter lending standards continue to slow new project starts, which could eventually support rent growth by limiting future supply.

What’s Next

Market participants are watching for catalysts that could break the current pricing standoff. Loan maturities, recapitalization needs, and investor redemption pressures may push more sellers to accept lower valuations over the next 12 to 18 months.

Absent a significant decline in Treasury yields, multifamily pricing will likely continue adjusting to a structurally higher-rate environment. Investors appear increasingly focused on operational performance and long-term income stability rather than short-term appreciation, signaling a more disciplined phase for apartment capital markets heading into 2027.