- San Francisco office properties averaged $1,088 PSF in February 2026, the highest pricing among major US office markets despite muted transaction activity.

- The metro recorded just $50M in office sales volume through February, while vacancy remained elevated at 24.2%, according to Yardi Matrix.

- Limited new development and steady coworking demand suggest the market is stabilizing, but leasing and investment recovery remain uneven.

San Francisco’s office market is showing signs of stabilization in 2026, but the recovery remains highly uneven, reports the Commercial Property Executive. Pricing for office assets rebounded sharply, topping every major US office market in February, even as transaction activity slowed to one of the weakest levels nationally, according to Yardi Matrix.

The metro is also seeing a sharp slowdown in development after years of life sciences-driven construction activity. Vacancy remains elevated, but leasing fundamentals improved compared to a year ago, while coworking operators continued to hold a meaningful footprint across the region.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Market Split Between Pricing and Activity

San Francisco recorded just $50M in office investment sales through February 2026, ranking 21st among the top 25 US office markets, per Yardi Matrix. Only Portland, Austin, and Nashville posted lower sales totals during the same period.

At the same time, average office pricing surged to $1,088 PSF, outperforming Manhattan’s $740 PSF average. The disconnect highlights how trophy and well-located assets are still attracting capital despite broader investor caution around the office sector.

One of the market’s largest trades so far this year was Moran Capital’s $44M acquisition of 240 Stockton St. in San Francisco’s North Financial District. The 40,442-SF property traded at a 45% discount compared to its 2016 sale price, according to Yardi Matrix data.

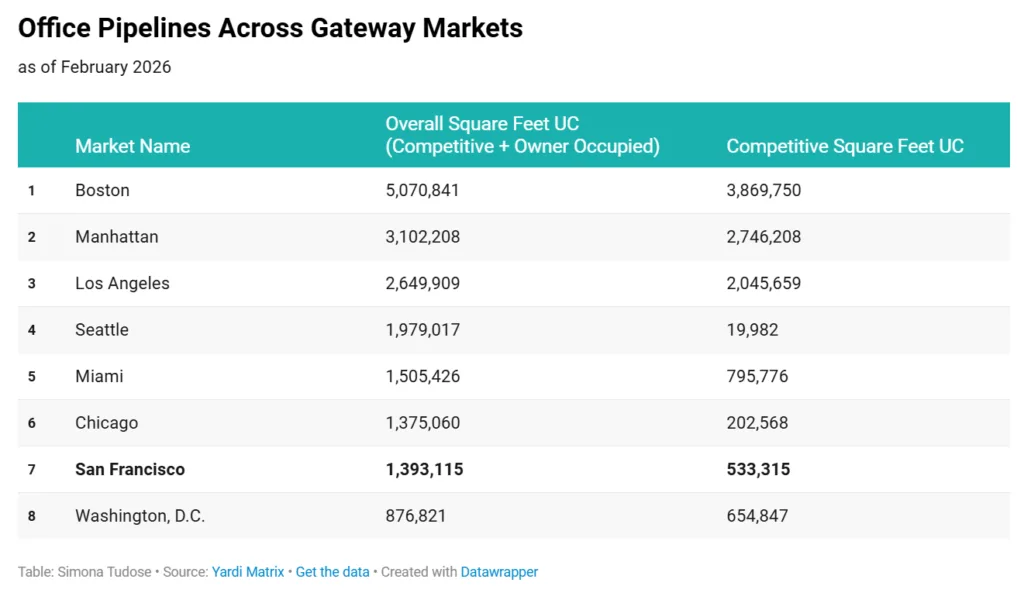

The Details

San Francisco’s office construction pipeline has thinned considerably. As of February, developers had 1.4M SF underway across seven projects, representing just 0.7% of existing inventory.

Competitive office development was even smaller, totaling roughly 533,000 SF, or 0.3% of inventory. Among the top 25 office markets, only Seattle had a smaller active pipeline.

The slowdown follows a major development cycle tied largely to life sciences demand. San Francisco led the nation in office deliveries during 2025 as several large, long-running projects reached completion.

Still, some major developments continue moving forward. Associate Capital broke ground in August 2025 on Block 2 at Potrero Power Station, a 278,230-SF office and lab project anchoring the broader $2B Dogpatch Power Station redevelopment. Plans for the site include 1.6M SF of office and research space, 110,000 SF of retail, and more than 2,600 residential units.

Another major project is YouTube’s planned 248,000-SF office component at 1300 Bayhill Drive in San Bruno. The project is part of the company’s long-term redevelopment plan approved in 2021.

Coworking Stays Resilient

Flexible office space has remained relatively stable despite broader office market volatility. According to CoworkingCafe, San Francisco had 3.9M SF of coworking inventory across 151 locations as of February 2026.

That footprint accounts for 2.2% of the region’s total office inventory, roughly in line with national averages. WeWork remains the market’s largest flex office operator with nearly 737,000 SF, followed by Regus, Studio by Tishman Speyer, Spaces, and MBC BioLabs.

The steadiness of coworking demand contrasts with broader leasing uncertainty. Flexible workspace operators have continued expanding in major US office markets as occupiers prioritize shorter-term commitments. Occupiers are still prioritizing flexibility while long-term office strategies evolve.

Vacancy Pressures Remain Elevated

San Francisco’s office vacancy rate stood at 24.2% in February, well above the 17.6% national average, according to Yardi Matrix. Still, the market improved by 360 basis points year-over-year, signaling gradual absorption gains after several difficult years for the sector.

Only Austin posted a higher vacancy rate among major US office markets at 24.6%. By comparison, Manhattan and Miami continued to outperform with vacancy rates near 13%.

Despite elevated availability, asking rents remain among the highest in the country. San Francisco office rents averaged $62.54 PSF in February, second only to Manhattan’s $73.45 PSF average and far above the national average of $32.79 PSF.

Why It Matters

San Francisco’s office market continues to illustrate the uneven nature of the broader US office recovery. Investors are selectively pursuing premium assets in gateway cities, but overall transaction volume remains constrained by financing costs, tenant downsizing, and uncertainty around long-term office utilization.

The pricing rebound also reflects how little institutional-quality inventory is actually trading. A small number of higher-value transactions can heavily influence market averages when overall deal flow is limited.

Meanwhile, improving vacancy trends and stable coworking demand suggest leasing fundamentals may finally be bottoming out after years of correction.

What’s Next

San Francisco’s office recovery will likely depend on whether leasing momentum continues through 2026 and whether large employers expand office commitments beyond hybrid workplace models.

Development activity is expected to remain subdued as lenders and developers reassess demand levels, particularly for speculative office projects. But with construction pipelines shrinking nationwide and trophy assets still commanding premium pricing, the city could be positioned for a more balanced supply environment over the next several years.

Investors will also be watching whether sales activity accelerates in the second half of 2026 as pricing expectations between buyers and sellers begin to align.