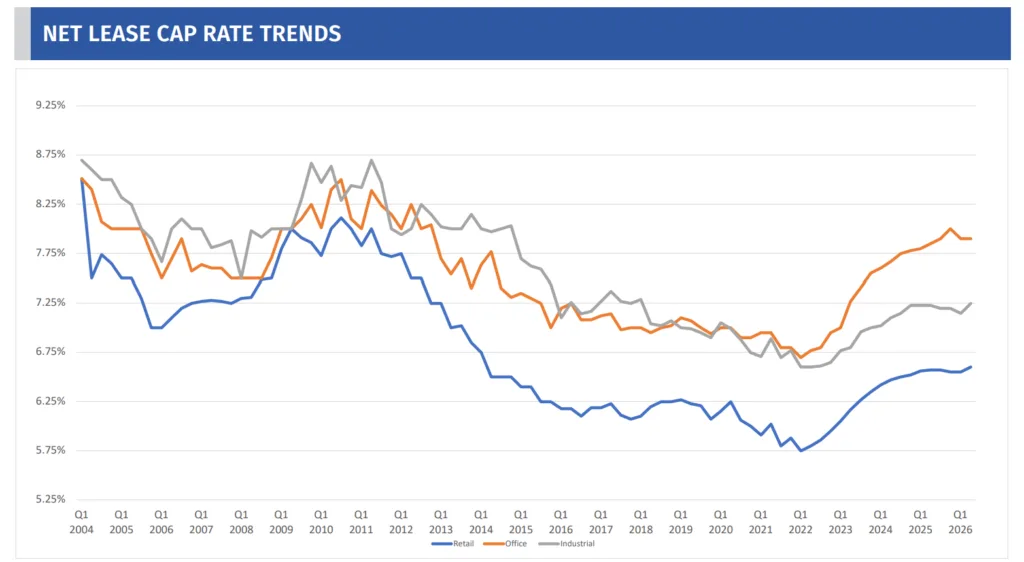

- US net lease cap rates edged up in Q2 2026, with retail up 5 bps to 6.60% and industrial up 10 bps to 7.25%, per The Boulder Group.

- Total single tenant properties on the market increased 12.5% quarter-over-quarter, driven by a 16.2% surge in retail availability.

- The gap between asking and closed cap rates continued to tighten, reflecting intense competition for premium, long-term assets.

Fed Hold, Retail Glut Set the Stage

Cap rates in the single tenant net lease space moved marginally higher in Q2 2026, signaling a market still adjusting to persistent rate uncertainty. According to The Boulder Group, overall cap rates climbed two basis points quarter-over-quarter (QoQ) to 6.82%, with the retail sector seeing a 5 bps increase to 6.60% and industrial climbing 10 bps to 7.25%.

Office cap rates held steady at 7.90%. The most notable macro development: The Federal Reserve kept the federal funds rate unchanged between 3.50% and 3.75% at both its April and June meetings, scrapping the rate cut previously forecast for 2026. The 10-Year Treasury hovered between 4.20% and 4.70% before settling near 4.40%. Investors read this as a signal that higher-for-longer rates may stick, keeping both cap rates and pricing stuck in neutral.

In Q2, investor focus shifted sharply as property supply in the single tenant segment jumped 12.5% QoQ to nearly 5,800 properties. Retail drove the bulk of the action—available listings in that sector surged 16.2%. The new inventory skewed toward non-credit tenants, while high-quality, investment-grade assets with long leases remained scarce at less than 10% of retail supply. That bifurcation underpins both pricing dynamics and competitive pressures in today’s market.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

High-Quality Asset Scarcity Drives Flight to Safety

Underlying the modest cap rate movement is a market increasingly split by asset quality. Investor demand for prime, long-term net lease assets—especially those anchored by investment grade tenants—remains fierce, as evidenced by a shrinking gap between asking and closing cap rates. In Q2, median spreads tightened by one basis point in retail and three in industrial, falling to 22 basis points for both.

Best-in-class deals include ground lease assets for Chick-fil-A and McDonald’s, which commanded the lowest asking cap rates in the sector at 4.45%. The appetite for high-credit tenants, especially those with proven store-level performance and long lease terms, continues to draw dollars from both institutional buyers and private capital, including 1031 exchange investors focused on assets under $10M.

A similar quality divide has emerged in office markets, where tenants continue to concentrate demand in premium buildings while older inventory struggles to compete.

The Details

Looking at sector specifics, retail cap rates climbed 5 bps to 6.60%, while industrial rose 10 bps to 7.25% and office held flat at 7.90%.

Source: The Boulder Group

The retail supply surge swelled to 4,452 listings in Q2 from 3,832 in Q1. Notably, the gap between asking and closed cap rates for both retail and industrial compressed to 22 basis points, reflecting competitive bidding for high-quality listings. Properties with long remaining lease terms (16–20 years) still drew sub-6% cap rates, but short-term leases (under 5 years) were priced at 7.6% or higher. Among auto and QSR tenants, asking cap rates ranged from 4.45% (Chick-fil-A ground lease) to about 7% depending on remaining term and credit. Selected closing comps in Q2 include McDonald’s and Chick-fil-A ground leases at 4.45%–4.75% and Del Frisco’s in Orlando at 6.23% on a nine-year term.

Investor Bifurcation Deepens

The trend lines in Q2 2026 reflect a bifurcated market that has persisted through two years of interest rate and macroeconomic volatility. Investors continue to prioritize credit quality, flocking to ground lease and long-term offerings from nationally recognized tenants—as seen in the competitive cap rate environment for McDonald’s, Chick-fil-A, and CVS.

The Boulder Group notes that less than 10% of retail supply now meets the high-bar of investment grade, long-term net leases. Meanwhile, non-credit and short-term listings are piling up and moving more selectively, often at wider effective spreads. Private capital, especially 1031 exchange buyers, is keeping money flowing beneath the $10M threshold, competing directly with institutional players.

With the Federal Reserve’s new leadership and projections now tilting toward a potential rate hike rather than the long-awaited cut, uncertainty is once again back in focus for CRE investors. According to The Boulder Group, investors are scrutinizing tenant financials and location fundamentals more rigorously, unwilling to sacrifice on covenant quality or lease length despite greater volume on the market. The Q2 tightening in bid-ask spreads signals some return of pricing discipline, yet actual deal activity shows a clear winner-take-most dynamic as the hunt for yield intensifies in the highest-quality segments.

What’s Next

Heading into the back half of 2026, investors will be closely watching the Fed for further signals on the rate trajectory after June’s meeting under new leadership. Market expectations are shifting from a rate cut to a potential rate increase, which could trigger more corporate sale-leaseback transactions as tenants look to optimize capital structures ahead of higher borrowing costs.

Despite increased property supply, transaction volume is expected to stay steady thanks to ongoing demand for quality single tenant net lease product. Both private and institutional investors remain active—but only the best-located, premium, long-term assets are commanding competitive pricing. All eyes are now on whether increased retail supply, especially from non-credit tenants, puts further upward pressure on cap rates in the quarters ahead.