- US multifamily rents increased just 1.0% in H1 2026 as demand cooled, per Yardi Matrix’s June 2026 National Report.

- Gateway and Midwest markets outperformed, while Sun Belt metros remained challenged by negative rent growth and below-average occupancy.

- The investment market is shifting toward debt strategies and agency product innovation as transaction volumes slow but multifamily remains the investor favorite.

Muted Rent Gains Test Market Resilience

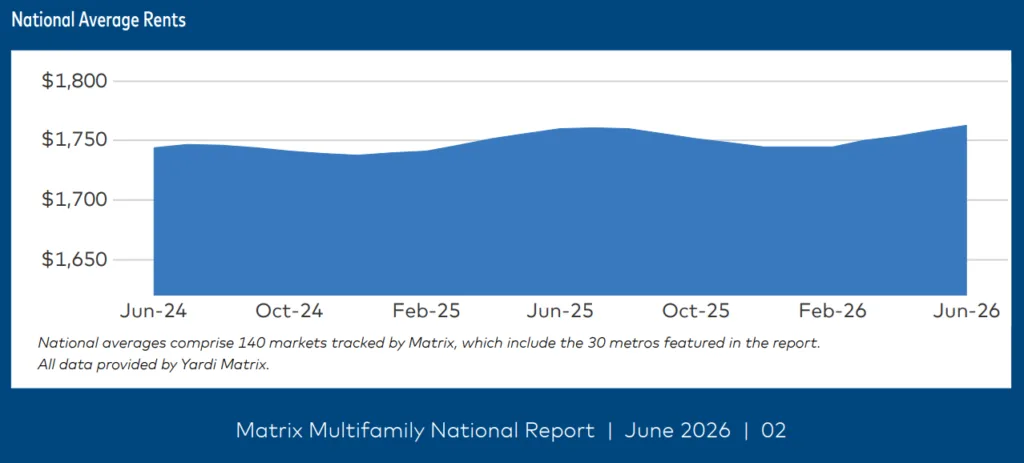

US multifamily owners saw advertised rents inch up just $4 in June, reflecting a 0.7% gain for Q2 and 1.0% in the first half of 2026, according to the Yardi Matrix June 2026 National Report. This pace falls well short of the 2.7% H1 gains typical from 2013 to 2019, and it highlights the current pullback in pricing power as a record pipeline continues to come online.

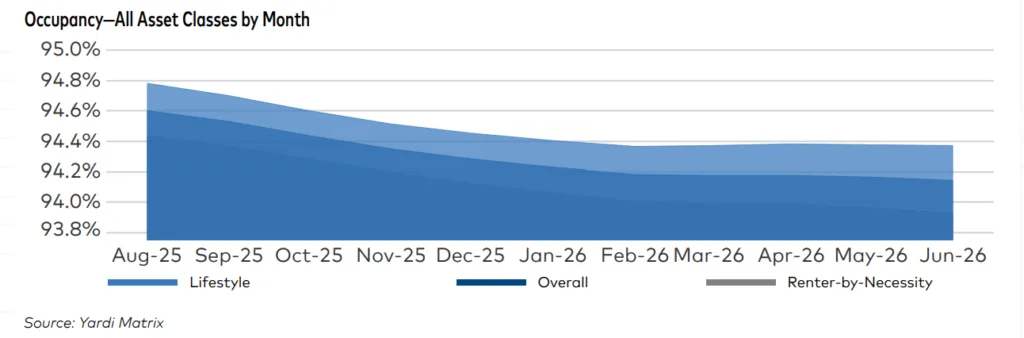

Absorption has retreated sharply. Roughly 108,000 units were absorbed nationally between January and May—61% fewer than in the same five months of 2025. Vacancy has crept higher: national occupancy slipped to 94.1% in June, down 60 basis points year-over-year. A few resilient gateway markets—including San Francisco, New York, and Chicago—posted rent growth above 2%, but most Sun Belt and secondary metros registered year-over-year rent declines.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Supply Waves Redefine Leasing Environment

Historically high apartment completions are reshaping the leasing landscape. Yardi Matrix reports that developers delivered more than 3% of apartment stock last year in key Sun Belt metros. Austin added 5.8%, Phoenix added 4.8%, and Charlotte added 6.1%.

These markets once defined strong rent growth. Today, they face annual rent declines instead. Austin rents fell 4.0% year over year. Denver rents dropped 3.1%, while Phoenix fell 2.7%.

Meanwhile, gateway cities posted stronger results. New York led with 5.6% annual rent growth. San Francisco followed at 4.7%, while Chicago reached 2.6%.

The gap highlights changing demand patterns. Renters are returning to expensive metros with stronger hiring and limited supply. In contrast, southern markets face the effects of aggressive development.

Investor Strategies Pivot Toward Debt

Property sales remain slow, and rent growth remains under pressure. As a result, multifamily debt has become a key focus for CRE investors.

Lenders have introduced a wave of new debt products. Multifamily-only CMBS issuance has also returned. In May, JP Morgan and MF1 priced a $734.2M transaction. Berkshire Residential and Limekiln operate MF1. Barclays, Citigroup, and others launched similar partnerships with private equity buyers.

Several structural changes support this shift. Agency lenders expanded their product offerings. Freddie Mac also redesigned its K-Series platform. Those changes created new risk-sharing opportunities.

Commercial Mortgage Alert reports that CLO issuance exceeded $30B by June. The market now tracks toward a record year. Moody’s Ratings expects private debt providers to capture up to $1T in market share over time. Investors continue shifting preferences, while banks reduce lending activity.

Affordability Pressures, Rental Bifurcation Deepen

Affordability concerns continue shaping apartment demand and performance. Lifestyle assets target higher-income renters who choose to rent. Nationally, those properties posted flat or negative rent growth of 0.2%.

Renter-by-Necessity assets performed better. They recorded annual rent growth of 0.5%. Nashville and the Inland Empire showed even larger differences. In those markets, spreads exceeded 950 basis points.

Yardi Matrix data shows growing pressure on lower-income renters. Many can no longer absorb additional rent increases. Gateway markets with stronger job recoveries continue outperforming across both segments. New York and San Francisco stand out.

Sun Belt markets face different conditions. Many rely heavily on household formation and migration trends. Those markets now report weaker leasing traffic and softer rents.

Strong labor markets continue supporting demand in select cities. However, many overbuilt metros now struggle with excess supply.

Why It Matters

Multifamily has shifted from rapid rent growth to slower gains and falling occupancy. The country’s largest supply pipeline caused much of this change.

Yardi Matrix reports that average national rent reached $1,763. Annual rent growth measured only 0.2%. That figure sits well below the 10-year average of 3.6%.

The decline highlights how quickly conditions can change. External shocks and overbuilding can weaken landlord pricing power.

The reset matters most in the Sun Belt. Markets like Austin and Tampa once appeared unstoppable. Today, both face negative rent growth and weaker occupancy.

Debt markets have benefited from these conditions. Lenders and capital markets firms report strong loan demand. Investors seek higher leverage and stronger yields. Equity transaction activity remains weak, while banks limit lending capacity.

Private debt funds are filling the gap. Expanded agency products are doing the same. Together, they are driving a new era of multifamily finance innovation.

The growing divide between Renter-by-Necessity and Lifestyle assets also deserves attention. Lower-income renters have little room for further rent increases. Future rent growth will likely depend more on wages and job growth.

Gateway cities continue surprising investors. Many wrote them off after the pandemic. Today, they lead the industry in employment and rent growth. San Francisco stands out in particular, as improving office fundamentals are helping support apartment demand and leasing activity across the city.

What’s Next

The outlook for the second half of 2026 remains cautiously optimistic. Inflation remains stubborn, but labor markets continue stabilizing. Stronger hiring could support demand recovery.

Yardi Matrix expects subdued rent growth through year-end. Strong job creation could improve absorption levels. Supply pressures will likely continue until completions decline in 2027.

Construction starts are already slowing. That trend should support a healthier balance over time. For lenders and investors, multifamily debt innovation will likely dominate the next cycle.