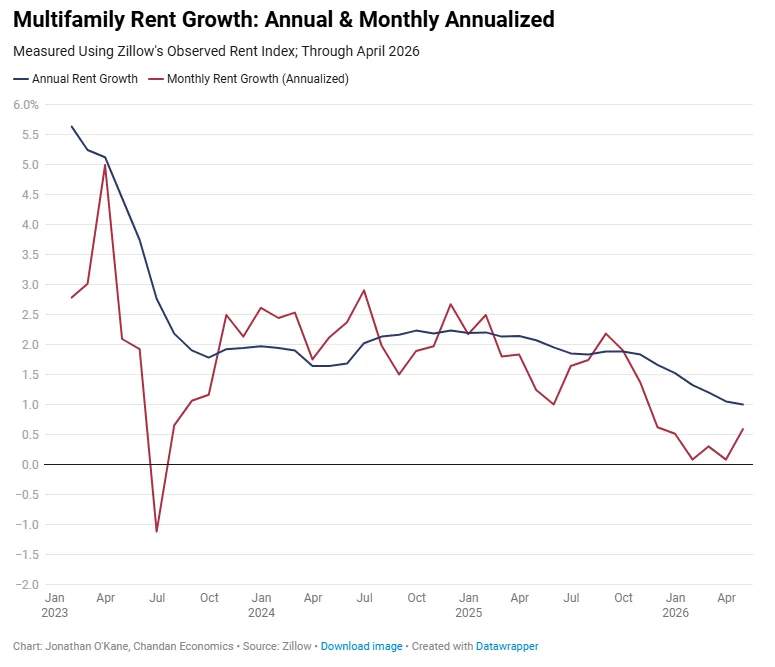

- National multifamily rent growth measured 1.0% year over year in April 2026, signaling that apartment rents may be stabilizing after months of deceleration.

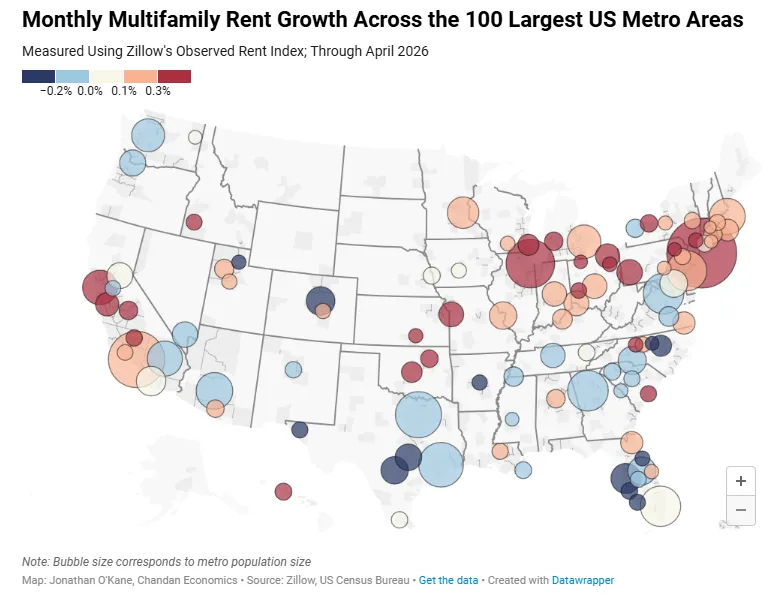

- High-supply Sun Belt markets including Austin, Tampa, and Cape Coral continued to post rent declines, while Honolulu and San Francisco led annual gains.

- Falling multifamily construction activity could ease supply pressures later this cycle, but stronger absorption will be necessary for rent growth to accelerate meaningfully.

US multifamily rent growth remained subdued in April 2026, though the latest Zillow Observed Rent Index (ZORI) data point to a market that is stabilizing rather than continuing to deteriorate. According to Chandan Economics’ May 2026 rent growth update, national apartment rents increased 1.0% year over year in April, nearly unchanged from March’s 1.1% gain but well below the 2.1% pace recorded a year earlier.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Broad Cooling Begins To Stabilize

The slowdown in multifamily rent growth has persisted since the post-pandemic apartment boom faded under the weight of elevated new supply and softer demand conditions. Still, Chandan Economics noted that the pace of deterioration has moderated in recent months, suggesting national rent trends may be bottoming out after an extended cooldown cycle.

The Details

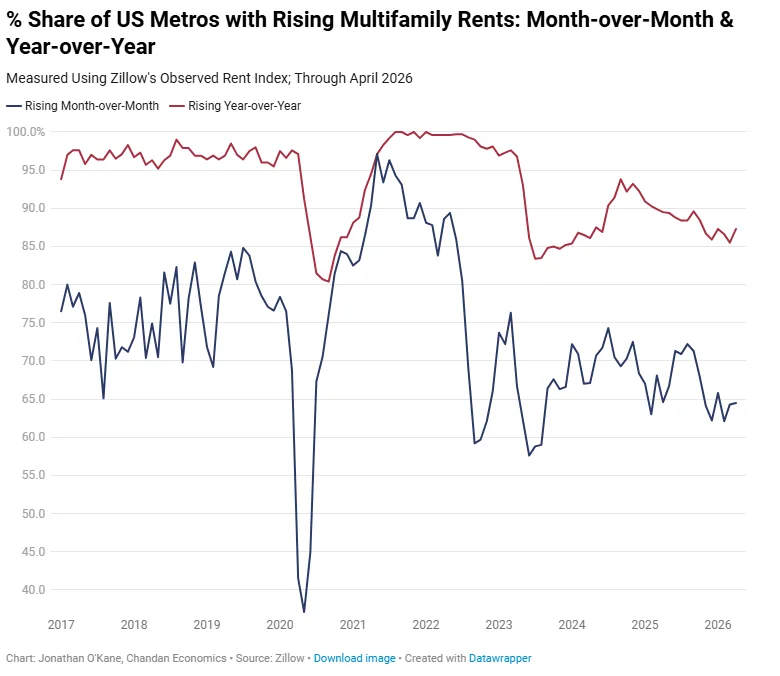

Monthly rent momentum improved modestly in April. National rents posted a 0.6% annualized monthly growth rate, up from just 0.1% in March and the strongest monthly reading in five months. Market breadth also stabilized, with 64.5% of metros recording monthly rent growth and 87.3% posting annual gains, both slightly improved from March levels.

At the metro level, performance remained highly fragmented. Urban Honolulu led annual multifamily rent growth at 6.4%, followed by San Francisco at 6.1%, Wichita at 6.0%, Toledo at 5.8%, and Scranton at 5.7%. Meanwhile, several oversupplied Sun Belt metros continued to struggle. Cape Coral posted the steepest annual decline at negative 5.9%, followed by North Port at negative 5.7%, Austin at negative 3.7%, San Antonio at negative 3.3%, and Tampa at negative 3.1%.

A Tale Of Two Apartment Markets

The latest data reinforce a widening regional divide across the apartment sector. Many West Coast, Midwest, and Northeast metros continue to see steady rent growth, while Sun Belt markets that absorbed massive development pipelines over the past several years remain under pressure. Florida and Texas metros have been particularly vulnerable as elevated deliveries outpaced leasing demand.

Short-term trends showed similar divergence. Honolulu led monthly rent growth at 1.4% in April, followed by Scranton at 1.2% and Akron at 0.9%. On the downside, North Port, Cape Coral, San Antonio, and Durham each recorded monthly rent declines of 0.5%, while Denver fell 0.4%.

Why It Matters

Multifamily owners and investors are closely watching signs that the sector may be approaching equilibrium after one of the largest apartment supply waves in decades. According to Chandan Economics, the number of multifamily units under construction has fallen significantly from its recent peak, indicating the development pipeline is beginning to normalize. That shift could help ease supply-side pressure over the next several quarters, particularly in oversupplied Sun Belt metros.

The uneven rent picture also underscores how localized apartment fundamentals have become. Markets with constrained supply pipelines or stronger employment growth are outperforming. That trend aligns with forecasts showing apartment market softness could persist through 2026 in oversupplied metros. Markets with aggressive multifamily construction continue to face downward pricing pressure.

What’s Next

The trajectory of multifamily rent growth will likely depend on how quickly new supply deliveries moderate relative to leasing demand. Elevated completions are expected to remain a near-term headwind through 2026, but slowing construction starts could gradually improve market balance. For now, the data suggest the apartment market has shifted from broad-based cooling into a more selective environment where local supply dynamics increasingly determine performance.